Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

I’m just going to say it – I have three very small businesses that I’ve been running for years and I’ve never paid estimated self-employment tax payments.

I’m just going to say it – I have three very small businesses that I’ve been running for years and I’ve never paid estimated self-employment tax payments.

Ouch, for shame, for shame!

That’s right, I’m a complete failure in that avenue. And that could have cost me, too.

If you owe $1,000 or more come tax day in April, you might be hit with a penalty by the IRS. In essence, it’s an interest penalty on the difference of what you should have paid and what you actually paid.

And guess who gets to decide what that interest rate is? That’s right, the IRS does. For the second quarter of 2019, they’ve decided that the rate for underpayments will be 6%.

Here’s the scary part – I didn’t know that until recently. Yeah, I’m not ashamed to admit it.

In fact, I didn’t even know that I should have been making estimated self-employment tax payments at all until a year or so ago.

Not only that, but I’m still learning all the details.

Regardless, my financial advisor/accountant, David, did my taxes for the first time this year and told me it was time to step up and start making the quarterly payments.

That’s fair – I suppose I should get over my fear and make some sense of all this. So let’s discuss this a little more…

What is self-employment tax?

In a nutshell, if you have a W2 job, your employer takes out taxes for you including income tax, Social Security, and Medicare. So that’s pretty easy. The government gets their money and then every year you settle up to figure out who owes who.

But if you’re self-employed, you just get all your money earned with no taxes taken out and a big old smile on your face. Then you could just pay everything owed come tax day, right? Not so much.

Uncle Sam’s not a big fan of waiting until after the year’s up to get his take. So, you need to pay estimated taxes four times a year to ensure that you’re staying current with what you owe.

Then you settle up on tax day just like everyone else.

When you need to pay estimated taxes

You’d think that the quarterly due date for your estimated self-employment tax would be every 3 months, but that seems too logical. Instead, the due dates fall as follows:

- For income you’ve made from January 1 through March 31, the estimated tax payment is due on April 15.

- For income you’ve made from April 1 through May 31, the estimated tax payment is due on June 15.

- For income you’ve made from June 1 through August 31, the estimated tax payment is due on September 15.

- For income you’ve made from September 1 through December 31, the estimated tax payment is due on January 15.

That said, if the 15th falls on a weekend or a federal holiday, the due date will be the following business day.

Um, do I really need to pay estimated taxes?

Hey, that was my question, too! And the answer is a firm… maybe.

The key is what I mentioned earlier. If you’re going to owe $1,000 or more when tax day rolls around, you need to be paying estimated taxes regardless of whether you’re self-employed or not.

If all your income is from a regular W2 job, then you’re probably in good shape since your employer’s already taking money out for taxes every payday. If not, you can file a Form W-4 with your employer to withhold an additional amount throughout the year to avoid that problem.

However, if you’re self-employed, you don’t have that “benefit” of an employer pulling out and getting taxes to the IRS. So the question is: will you owe more than $1,000 come tax day?

If the answer is yes, it’s time to start filing estimated taxes.

I currently have three small businesses plus some other “income” coming in later this year. Let’s take a look at where I’m at with each…

Business #1 – Publishing

You can look at this as a good thing or bad, but my one business hasn’t made enough money for this to matter. This is the publishing company I created in 2007. I’ve written and published two books under this LLC.

The first was published in 2007 and the second in 2015. With such a large gap of time between books and no real marketing, I didn’t have a year where I made enough money to skew my tax return enough to owe the IRS money at the end of the year (so no penalty).

And that’s Ok – with those books, the goal wasn’t to get rich. Instead, it was for the feeling of accomplishment of actually writing a book and having it in the hands of other people. I sold a little less than a couple of thousand books and that exceeded my expectations at the time.

However, the next books I decide to write will likely (or at least hopefully) sell more copies. I not only understand the whole process much more, but I also have an outlet to market it. A larger audience is always good for these things!

Business #2 – Real Estate

The second business we have is the LLC that holds our rental property. At one point, this was both a rental house and a duplex. However, we sold the rental house in 2018, so it currently just contains the duplex we bought in 2015.

But another awesome feature of rental property is that the income you receive is not counted as wages unless you’re a real estate professional. To be considered a real estate professional, IRS Publication 925 states that you must meet both of these requirements:

- More than half of the personal services you performed in all trades or businesses during the tax year were performed in real property trades or businesses in which you materially participated.

- You performed more than 750 hours of services during the tax year in real property trades or businesses in which you materially participated.

That stuff’s pretty boring, but basically, since it isn’t our main business (especially because we use a property manager), we’re not real estate professionals. And as such, no sucky self-employment tax for us. On top of that, our rental income gets put on Schedule E and gets treated as passive income during tax time… yay!

Business #3 – Personal Finance

Business #3 is the one I’m enjoying the most right now… this one! The Route to Retire empire in all its glory. Ok, it might not be an empire yet, but it’s still the most fun. I love writing for it as well as the interaction I get from you guys. This community has been fantastic and supportive from the onset of this blog in 2015. And, of course, I love seeing the growth over time.

This is also the business where I’m starting to pay self-employment tax. That’s not a bad thing for sure, but it’s a kick in the pants to learn how to do this stuff.

This has obviously been a gradual shift and, believe me, my first payment wasn’t very big. As this site and brand continue to grow though, I expect the income to also expand as well.

The Roth IRA conversions

Now that I’m retired, earlier this year, I rolled over my 401(k) into a traditional/rollover IRA. This is the same process we did with Mrs. R2R’s old 401(k) a year or so ago.

The goal now is to start converting the money in these IRAs to Roth IRAs at the end of each year. Roth IRA conversions are taxable and I’m fully prepared for that.

What I didn’t consider though is that each of these conversions counts as income. And we learned earlier that if you receive income from a source other than an employer, you’re generally on your own in getting the IRS their money along the way.

So even though this isn’t income in the traditional sense, we’ll still need to make estimated tax payments each year that we do this.

How I’m handling my estimated self-employment tax fun

First things first. A vital component of running your business is to keep your business income and expenses separate from your personal. When we start out as entrepreneurs, things usually come together pretty slowly and we tend to let those things blur together.

That can lead to trouble – you need to keep everything separate.

I made it a point to open a business checking account for each of my businesses at U.S. Bank when I first started them. Why U.S. Bank? Because they were the only no-fee bank available in our area and my credit union wouldn’t do business accounts. A no-fee account is important for any business just starting out, so find one in your area.

Then I have the Chase Ink Business Cash credit card for each business. I like that card because it offers some good cash-back opportunities, gives me a chance to take advantage of the sign-up bonus, and most importantly has no annual fee.

Use your business credit card to pay for all business expenses and use your business checking to pay the bill. Pull that off and you’ll set yourself up and make life soooo much easier for yourself.

Now onto the fun of self-employment tax.

There are all sorts of different accounting programs you can use to manage your expenses. Some are free and some cost money. They all have their pros and cons as well.

For me though, I found that the easiest way to do this is to use QuickBooks Self-Employed. This isn’t the full-blown version of QuickBooks you may be familiar with. Instead, it’s a simpler version that’s all online (or through their app) and designed specifically for independent contractors and freelancers.

My financial advisor recommended using this program for a few reasons:

- QuickBooks is considered to be the de facto standard when it comes to accounting for small businesses.

- He’s able to access it to be able to review things, provide advice, and do my taxes.

- It does all the math of calculating your quarterly estimated taxes automatically.

That last one is the big one for me. It just shows up at the top and tells me exactly how much to pay and when. I love the simplicity. I want to focus on growing my businesses and I like having someone (or rather something) handling this pain-in-the-@#$ math for me.

So here’s the deal – I just connected to my business checking and credit card I use for Route to Retire. Um, yeah – that’s really it.

Because I’m not commingling my business finances with my personal, this becomes extremely easy to manage. I just log in every few weeks and review the transactions to categorize them and make sure nothing personal got mixed in.

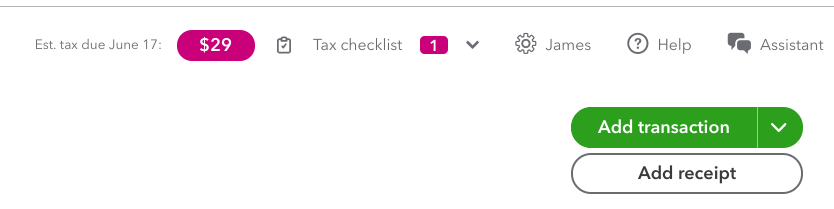

QuickBooks always tells you at the top what your estimated tax payment is and when it’s due:

Simple, right? That’s really it. You can upgrade the software to pay the IRS directly through QuickBooks, but that’s definitely not the Route to Retire way!

I went to the Direct Pay page on the IRS website and easily made my payment from my business checking… for free! I’m also told you could pay through their EFTPS: The Electronic Federal Tax Payment System, but the Direct Pay seemed simple enough for me.

I also set a recurring calendar event for myself for the 15th of each month when quarterly payments are due. I’ll get notified a week or so in advance, log into QuickBooks to see what I owe and make a payment. Easy peasy!

When we do our first Roth IRA conversion at the end of this year, we’ll calculate the appropriate amount of tax for that and add that to the 4th quarter payment that Quickbooks tells me to make.

If you’d like to follow suit and make your life easier, here’s my link to sign up for QuickBooks Self-Employed. You’ll help support this blog, but more importantly, you’ll save some money as well.

Making estimated self-employment tax payments isn’t as scary as I thought it would be. It was just a matter of learning a little more of how this worked and finding a system that worked for me. The key was keeping it simple and I think this should work out well over the long run.

Have you started paying self-employment tax for a business? Anything you want to add?

Thanks for reading!!

— Jim

I did a similar post recently Jim and my strategy is to have my W2 job take out extra to cover for my side hustle income so I don’t have to file quarterly. Of course you need to still have a W2 job to do that 🙂

I saw that post, Dave, and really liked that idea! Of course, the chances of me going back to a W2 job are pretty much slim to none! 😉

— Jim

Quickbook sounds like a good piece of software. I’ll check it out.

I started sending in estimated tax in 2018 because we owed over $10,000 from the previous year. It worked out okay and this year I owe much less, around $1,500. I just took a guess and it worked, somewhat. This year, I’ll probably send in a bit extra to avoid underpayment.

That actually makes me feel better, Joe. I figured that guys like you would know the estimated taxes inside and out. The next-to-nothing cost of QuickBooks Self-Employed could really be worth it and simplify things for you.

— Jim

Hmm, I’ve had to pay these estimates in the past but had always done it manually and with a physical check through snail mail. I like your more semi-automated approach

What’s a check? 🙂 Just kidding, but I do try to avoid writing checks any more when I can. To each his/her own though – what works for me might not be a great solution for someone else and vice versa.

— Jim

I just started having some self-employment income so your article is timely for me. I was under the impression that you could include your self-employment tax with your income tax in figuring out the minimum amount of estimated tax you had to pay – 90% of this year’s tax or 100 of last year’ tax. Is that not right? Do I need to pay the self-employment tax quarterly separate from the rest of my income tax.

Hi Susie! You’re correct in that you can pay 90% of this year’s tax or 100% of last year’s (sometimes referred to as safe harbor). As far as paying the self-employment tax separately, I don’t believe that’s necessary. In our situation, we’ll have “other income” coming in from the Roth IRA conversions at the end of the year. According to my accountant, we’ll be calculating the appropriate amount of tax and adding that to the fourth quarter payment that Quickbooks tells us to make. So I would guess that your situation would likely be similar in the aspect of other income tax.

Keep in mind that I’m not an expert on this and you should probably talk to an accountant for advice. I’m still learning a lot of this, but I’m definitely liking that the self-employed version of QuickBooks makes it seem a little simpler.

Good luck!

— Jim