Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

I’ve never done a portfolio rebalancing on my resting investments. As I’ve made money moves over the last few years to get prepared for early retirement, that’s helped me to rebalance accordingly at those times.

However, this was my first shot at actively doing a portfolio rebalancing just because it was time.

All the smart financial folks out there will tell you that rebalancing is an important part of maintaining your investments. The problem is that those folks don’t usually detail the steps on how to actually implement it.

Good news! I’m going to take you through what portfolio rebalancing is and how to do it more easily. I’ve also created a spreadsheet that I’ll share with you to help you out with the process.

So let’s get started!

The usual disclaimer: As always, remember that I’m just sharing my thoughts on what I’m doing. Don’t take this as investment advice. Talk to a professional before making any money moves you don’t fully understand.

Asset allocation

Here’s the deal – if you’re newer to getting your finances in order, you’re probably focused on just adding more and more $$$$ to the pot. Good! That’s the most important thing. The more you add, the bigger the growth swings can be over the long run.

However, at some point, you want to look more at your asset allocation. In essence, your asset allocation is what percentage each asset holds in your total investment portfolio. For example, you might have an asset allocation of 60% stocks and 40% bonds.

This could also be taken deeper to be something like:

- 50% U.S. stocks

- 10% international stocks

- 25% U.S. bonds

- 3% international bonds

- 5% alternatives

- 7% cash

For me, I’m trying to keep it simple and just know what I have in the volatility of the stock market versus something a little more stable like bonds. The idea is that the stock market should give growth over the long term, but it could be a rocky ride along the way. Stability of assets such as bonds can help smooth the path but you likely won’t get as much growth out of them.

You’ll want to figure out what an ideal asset allocation for you would be. Personally, I have a lot of years ahead of me where I need the long-term growth of the stock market. I’m also comfortable with a little risk. Right now, my desired asset allocation is 70% equities (stocks) and 30% bonds and other assets that are a little more stable.

As a side note, this is strictly for my investment accounts through my brokerages. I do have a year’s worth of living expenses in cash in Ally bank that isn’t included – nor is the rental income from the duplex we own.

Depending on where you are in life and your risk tolerance, you’ll want to figure out what your ideal asset allocation is. If you’re more risk-averse or further on down the plan than I am, you might choose to be less heavy in the stock market.

Or maybe you’re exactly the opposite and just want to let it all ride in the market… all in, baby!!

That’s up to you – it’s all about finding what risk level lets you sleep at night.

What is portfolio rebalancing and why is it important?

Let’s assume you set up your asset allocation to be 70% stocks and 30% bonds. Whew, glad that’s done, right?

Well, it’s not. Over time, those percentages are going to get out of whack. As the stock market goes up, so does the value of your investments. That adds more weight to that percentage which drops your percentage of bonds.

Now, maybe you’re 75% stocks and 25% bonds. Dang, it! What the heck?!

Or it could be the opposite. If the market heads down, but your bond values grow, you might be 65% stocks and 35% bonds. Son of a biscuit!

Time to rebalance. Portfolio rebalancing is simply the idea of buying/selling different assets in your portfolio to get their percentages back in line. You sell the stuff that became a little heavy and then buy more of the asset class that became lighter. You make the moves to get back to your desired asset allocation percentages.

In this case, if we’re 75% stocks and 25% bonds and want to get back to 70/30, we need to sell some stocks. Then we’ll probably want to put the money back into bonds or something along those lines to get everything back in check.

Why is this important?

Well, the reason you want to periodically do a rebalance of your portfolio is to help manage risk. If the percentage of equities in your portfolio starts becoming a lot higher than your desired asset allocation, you’re now exposed to more risk than you want.

The inverse is also the same. If your equities position drops too much, you could be miss out on growth potential because too much of your money is now tied up in slower movers like bonds.

Important note: target retirement funds will handle portfolio rebalancing for you… leave ’em alone. They’re designed to follow a risk level that may start out heavier in equities but over time will become more bond-centric as it gets closer to the chosen fund year (which generally matches your retirement date).

If you don’t care about trying to figure out what to invest in and when to rebalance, low-cost target retirement funds can be the simplest way to invest in your portfolio. You just keep putting everything into the fund and the magic will happen automatically for you.

When to do portfolio rebalancing

Rebalancing used to be something that you didn’t want to do too often mainly because of the selling/buying commissions with each transaction. However, if you’re with a low-cost provider, chances are that a lot of their funds can now be bought or sold with no fees involved. Competition in the economy = major consumer wins!

Regardless, your investment portfolio should be pretty hands-off for the most part. Some folks recommend doing a portfolio rebalance once a year on a random date like your birthday or anniversary. You rebalance on that day regardless of what the market’s doing.

Others recommend rebalancing twice a year or even quarterly. How often you decide to do that is up to you.

Another smart recommendation is to just keep an eye on your portfolio and when the asset allocation gets out of whack by a predetermined amount, you rebalance. For example, if one asset class drifts by maybe 4% then you know it’s time to rebalance.

Now that we have everything in place and our drawdown on investments is rolling, I plan to do my rebalancing twice a year. One of the dates will be on my birthday every summer.

The second time will be in January when I make my money moves for the upcoming year. That’s the time when a year’s worth of expenses in my bond fund ladder will have matured and I buy another year’s worth. It’s also when we move a year’s worth of expenses to our online savings. It’s a perfect opportunity every year for me to evaluate where things stand and update as needed.

Additionally, as I’m writing this, the market’s been doing incredibly well. So with that, I’ll be keeping an eye on my portfolio a little more and possibly adjust a little more if the percentages get too out of line.

As an aside, if you’re adding new money into investment accounts, you can also just use that to do some rebalancing. For instance, let’s say your allocation of stocks is high and you have, say $10k you’re ready to invest. Instead of putting that toward stocks, you can just invest that in bonds (or other potentially less risky side assets) to help get your percentages back in order.

Leveraging Empower (formerly Personal Capital) for simplicity

You might be thinking, “Jim, the idea of rebalancing sounds great but how in the @#$% do I figure out what my asset allocation currently looks like?“

Well, you can try to manage this yourself via spreadsheets and other fun, but that can get complicated. If you have multiple investment accounts (which most of us do), you can expect a lot of work compiling the data each time.

Personally, I hate doing extra work, so now comes the fun part.

The best resource I’ve found to make this as simple as possible is Empower (formerly Personal Capital). It’s a fantastic website and they have an awesome app as well.

If you’re not familiar, Empower (formerly Personal Capital) is a free service that aggregates all your financial accounts into one nice dashboard. It’s superb for easily seeing exactly where you stand financially. You can view your net worth at a glance, see the value of each account, and view/filter all your transactions.

They also have a nice Retirement Planner tool built-in, which is very easy to use and works extremely well. I’ve found this to be very useful in my own planning.

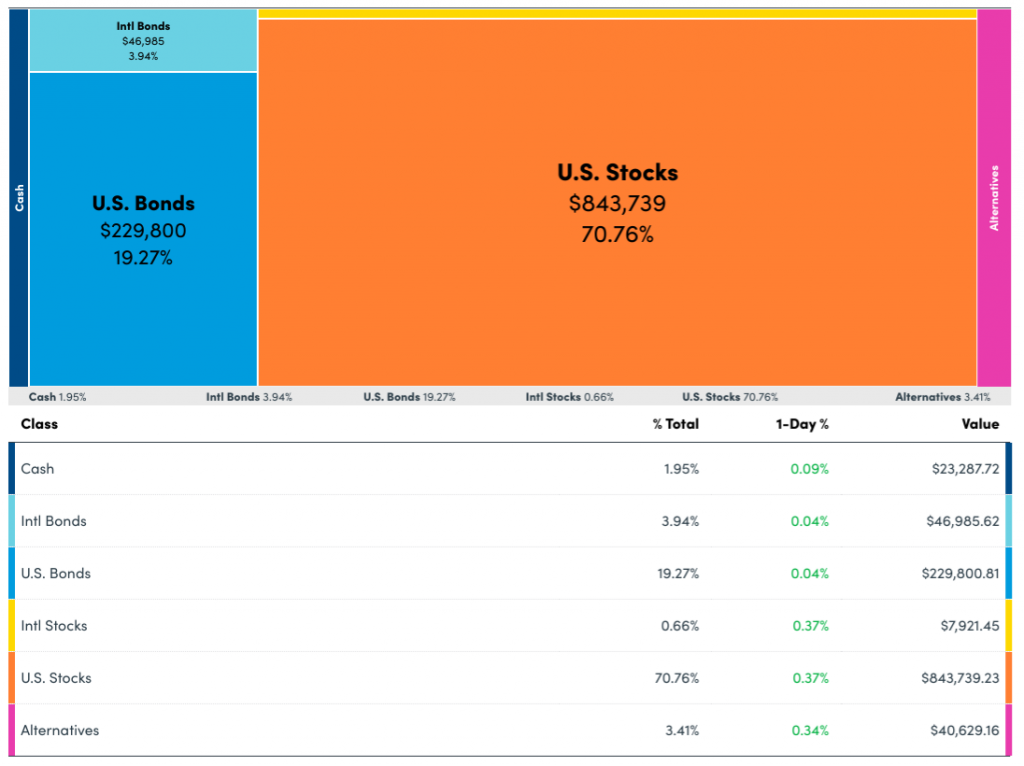

In addition to all this great stuff is that with a simple click off the menu, you can view exactly what your asset allocation is…

BOOM! I do love Empower (formerly Personal Capital) and I’m probably in it every week or so to manage my investments.

The best part is that it’s free. Be aware that they might call you to offer a free portfolio review but you don’t need to take ’em up on it. I told them I wasn’t interested, but you’re welcome to if you feel that could provide you some value.

Here’s an asset allocation spreadsheet to use

So, the easy part’s out of the way. You can see your asset allocation at a glance and know when and why you should do a portfolio rebalancing act.

But just because you see that your stocks are now consuming too much of your asset allocation, how do you know how much to sell or buy?

I’m with you. That was something I needed to figure out as well. I could see my asset allocations and wanted to adjust but needed to do some math to figure out how much to do.

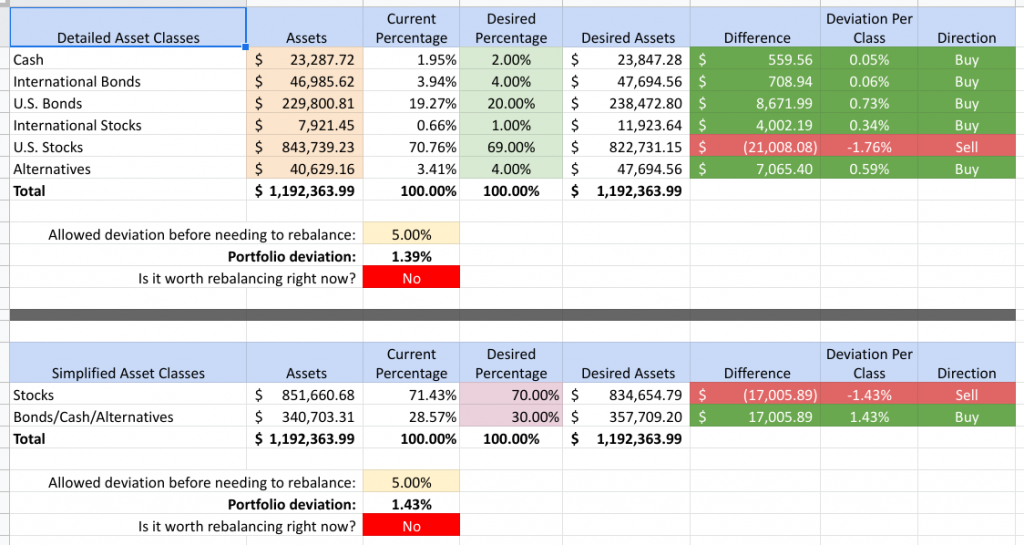

This is where spreadsheets shine! So I decided to create one that would help me calculate how much to buy or sell within each class.

While I was looking for some formulas I needed, I stumbled across a post from a very valued member of the FIRE community, The White Coat Investor. He had a basic portfolio rebalancing spreadsheet in his post How to Make a Portfolio Rebalancing Spreadsheet.

I used this as my starting point and then built it up into something more useful for my needs. Here’s a look at what I ended up with:

You fill in a handful of cells and it does all the rest for you. You have your choice between looking at a detailed table or a simplified table. Simple but valuable, right?

Since I know we all like that, I’m offering this up to you to use for your finances as well.

If you’re already on my email list, you already received a link to this spreadsheet in an email talking about this post. If not, sign up here and I’ll send a link to this spreadsheet right over to you (along with some other useful tools)…

Um, did you just continue on reading without signing up? C’mon, stop being silly… sign up real quick. You’ll be glad you did!

For real… do it.

I’ll wait.

Ok, I’ll trust that you’re now on the list. So let’s talk about what this spreadsheet does. It’s a cinch…

- Enter your balances for each asset class that Empower (formerly Personal Capital) ever so conveniently lays out in front of you.

- Enter your desired percentages for each class ensuring that they add up to 100%.

And…. done. Easy peasy, right?

You’ll now see how much you need to buy or sell within each asset class to get you back in line with your goal.

You’re now ready to do the actual portfolio rebalancing!

Making the money moves

I can’t give you specific instructions on how to buy or sell your stocks or bonds since there are way too many brokerage firms out there. Plus, the type of asset you’re buying or selling will likely be completely different than the next guy or gal.

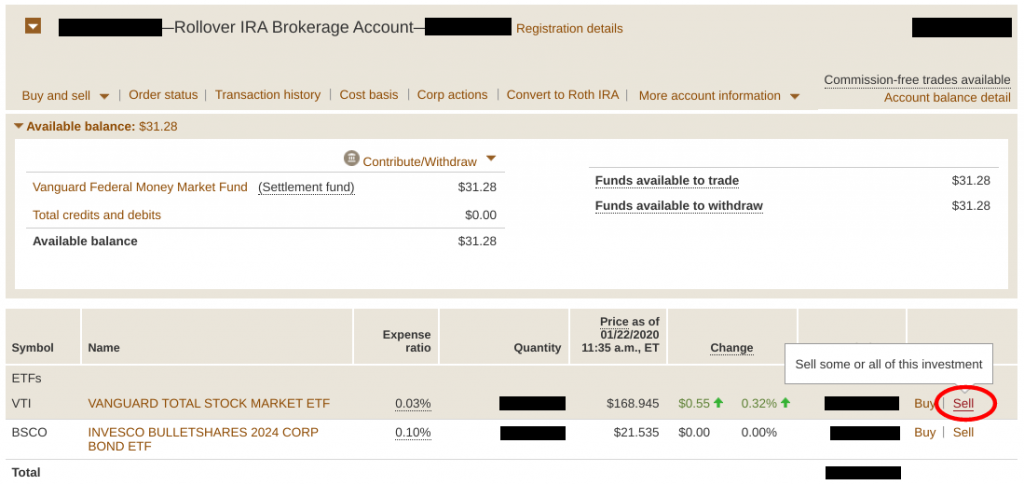

However, I just went through and sold about $17k worth of stock to get my asset classes aligned again and I’ll show you how that worked. My account is through Vanguard, but the gist of what we’re all aiming to do is the same.

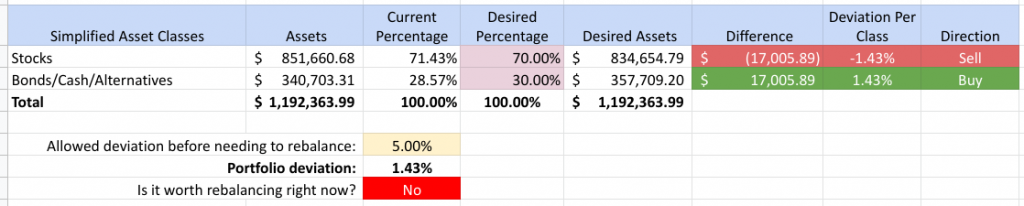

The spreadsheet was nice enough to show that I was $17,005.89 too high in stocks…

Technically, my portfolio’s not off by too much (1.43%), but I like you guys so much that I thought I’d rebalance anyway. I decided that I would sell roughly that amount in my Rollover IRA account to get the house back in order.

So I logged into my Vanguard account, went to that account, and chose “Sell” next to VTI which is my total stock market index fund.

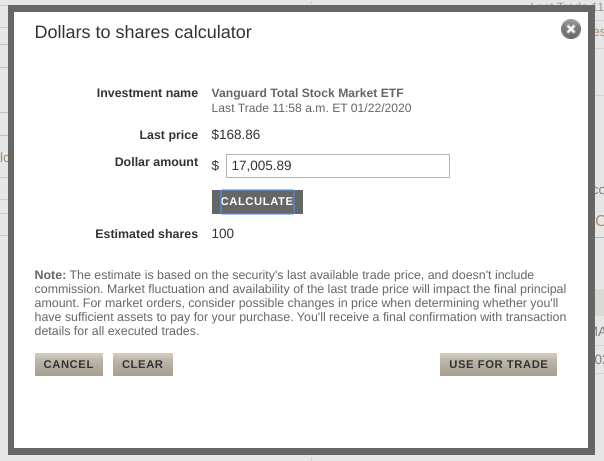

I used their “dollars to shares calculator” to determine that at the current share price, I should sell roughly 100 shares. Perfect!

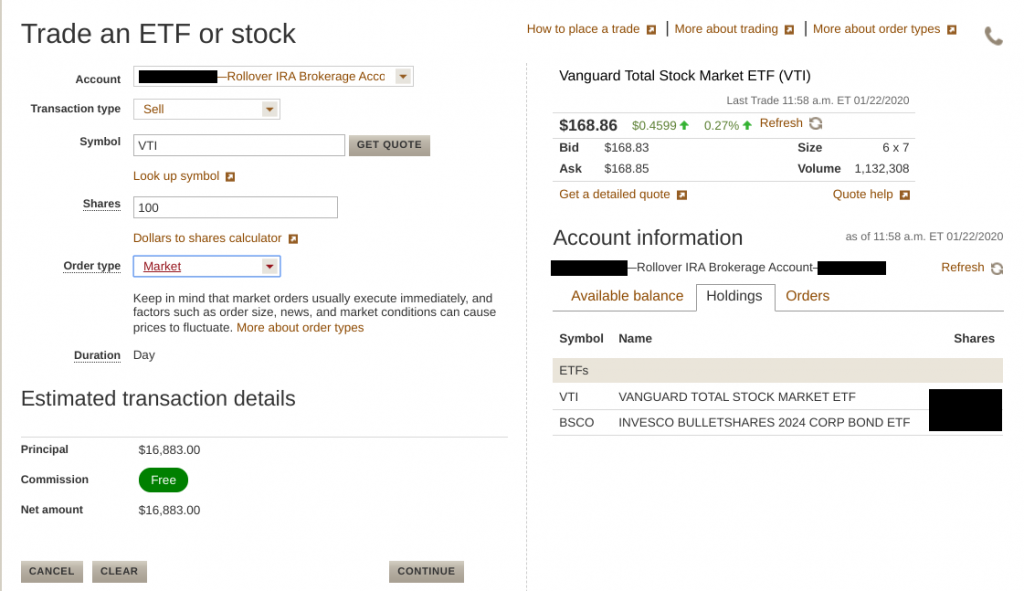

I entered all the detailed needed…

And then I submitted it as a market order to be processed. Notice the part about this being “Free” and no commission taking place. That’s the reason I was more than willing to do this run-through. Normally, my portfolio deviation being off by such a small amount wouldn’t have justified the move, but you’re worth it!

The order executed immediately and I’m now done with my portfolio rebalancing for about six more months!

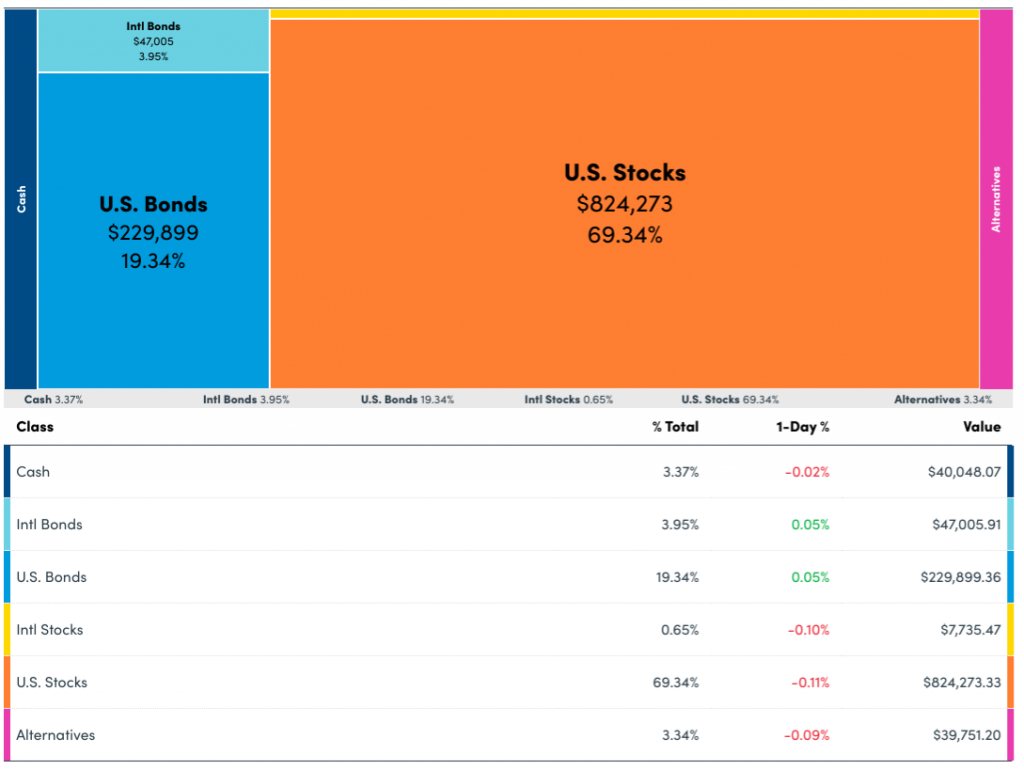

Once the trade settled the next day, I logged back into Empower (formerly Personal Capital) to see how everything looked.

No surprises here… even with the market changes for the day. Between my U.S. and international stocks, I’m almost exactly at the 70% mark in equities again. This is right where I want to be.

I plugged the numbers back into my spreadsheet so I could show you where we’re at:

Beautiful!

I haven’t decided yet if I’m going to leave this money in my money market account at Vanguard or buy some more bonds with it. I may just leave it alone until my next portfolio rebalancing is done in the summer. Or, if the market drops down significantly, now I’ve got some money on the sidelines waiting for the opportunity.

Only time will tell!

That’s it, folks! I’m glad I now have a plan in place to help me easily rebalance as needed and I hope this helps you with your portfolio as well.

Do you already practice portfolio rebalancing? If so, how do you do it and how often? If you don’t, what’s been holding you back from doing so?

Thanks for reading!!

— Jim

Do you worry about the tax implications when you rebalance?

Fantastic question, Joan! If you’re making money moves in a regular taxable brokerage account then yes, that would be important – capital gains and losses would come into play. However, with retirement accounts like 401(k)/403(b)s, traditional IRAs, or Roth IRAs, capital gains don’t come into play so you don’t have to worry about that hammer being dropped there. 🙂

We pay a minimal .30 fee for Vanguard to automatically review & rebalance for us quarterly. The fee is worth it for us to take this off our plate. Since my husband retired this week, we rebalanced to 50/50 recently & Vanguard took care of it over the phone! We are actually considering suspending this service now as we probably don’t need this review anymore. Thanx for sharing all this info. It does give food for thought.

Vanguard Personal Advisor Services is fantastic for those who don’t want to be too hands on with their portfolio. I haven’t used them before but I’ve read quite a bit about it. In the latest iteration of the “in case I die” letter to Lisa, I instruct her to use this service to manage our portfolio (or “her” in this case).

Congrats to your husband on retiring! I know he’s been chomping at the bit to get done from what you had said before so that’s exciting news. 🙂

Good post. Going to link to it in my posting on rebalancing. I think you did a good job covering the method.

Thank you – very much appreciated!

Great post! Will revisit next rebalance. Thank you.

Thanks, Brad – much appreciated! Have a great weekend!