What kind of person actually wants a stock market crash just two months before retirement?

This guy, that’s who!

That might sound like a weird sentiment especially considering I’ve been worried about this exact thing over the past couple of years. After all, a down market would kill my net worth at the same time I plan to start withdrawing my money.

This discussion is specific to the mindset of getting closer to retirement. If you’re in the accumulation phase of your life, you shouldn’t be questioning whether or not a down market is good.

If that’s the case, a stock market crash is exactly what you want. You should already be saving and investing so a crash would just help you to buy a lot more shares at their “on sale” prices.

But when you’re coming up on retirement, it can become a little more critical depending on what your plans are to fund your lifestyle.

The problem with a stock market crash when retiring

When you’re dealing with retirement (particularly early retirement), you need to be concerned with something called sequence of return risk. The general idea is that you’re most vulnerable to hurting your long-term retirement if you’re counting on your investments to fund your expenses and the market takes a dive during the first handful of years after you quit your job.

Here’s an example – let’s keep it simple and say you have $1 million in investments. According to the 4% rule, that would mean you’d be able to withdraw $40,000 annually (adjusted every year thereafter for inflation) for at least 30 years.

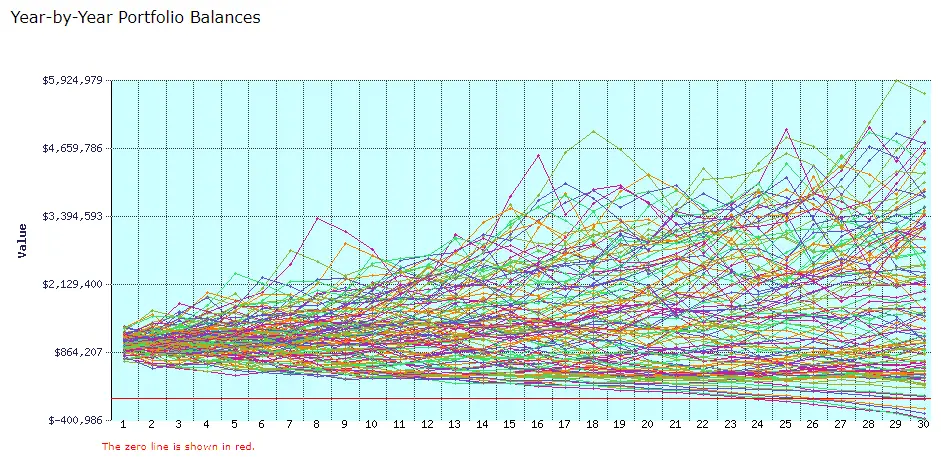

If you run this through one of the FIRE calculators out there, you’ll find that the simulations show that your plan will likely succeed over the long haul. Here’s the scoop from FIRECalc:

In fact, FIRECalc tells us that it looked at the 118 possible 30-year periods in the available data with the example $1,000,000 portfolio and $40,000 in annual expenses. It found that only 6 cycles failed giving us a success rate of 94.9%.

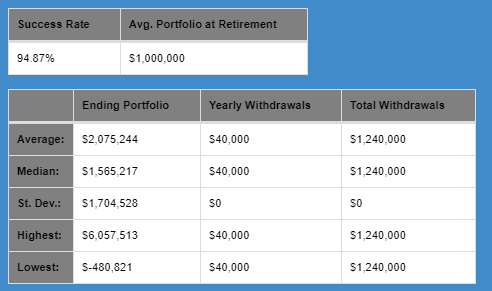

Another calculator, cFIREsim, gives us results along the same lines showing a 94.87% success rate:

In other words, even with a stock market crash or two, you’re probably going to be just fine even with all things considered.

But…

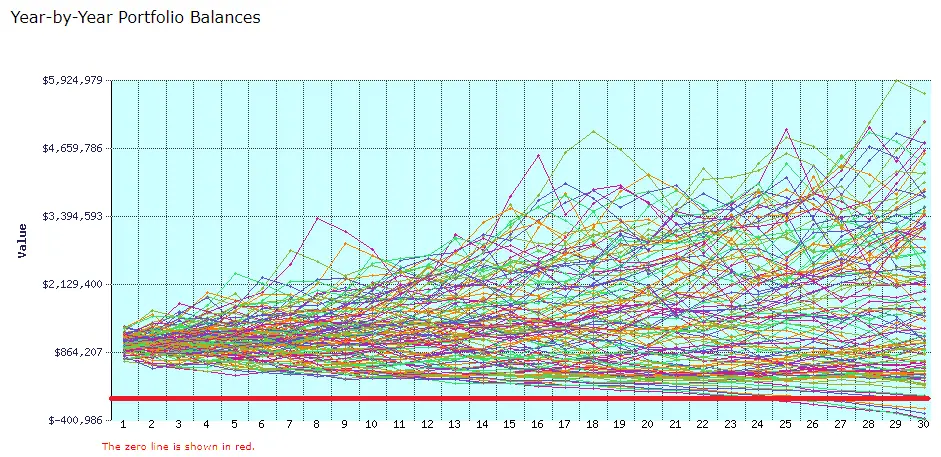

Yup, there’s always a big old “but” out there somewhere. Look again at the chart from FIRECalc (I highlighted the zero line to make it stand out a little more). It might be a little hard to tell, but the lines that tend to not quite make it and cause you to run out of money seem to stem from your portfolio going down in the first few years…

And that is really the crux of the problem. That’s what sequence of risk return is all about. If you get unlucky and a stock market crash or other downturn happens during your first few years of retiring, you have a potential problem.

With a smaller balance than you initially started with, you’re now pulling out more principal than gains. And when that happens, you get stuck with less money in your portfolio to accumulate gains over the coming years.

So the likelihood of you running out of money in your portfolio increases. That’s why it’s usually better to catch the market on a bull run over a few years when you first leave your job.

With that said, why the heck would I be rooting for a stock market crash when I’m just a couple months out from leaving my job?

1) Protection and resiliency

A lot has changed over the past couple of years that’s helped me become a little less worried about a stock market crash.

When I first started down this path, I was just saving and investing. I didn’t really have a solid plan in place. But as I started getting closer to setting a solid FIRE date, I was debating between utilizing a Roth IRA Conversion Ladder or Rule 72(t) to be able to get to my retirement investments.

I didn’t really like Rule 72(t) because it’s very precise and inflexible. And once you start withdrawing money with this process, you’re basically stuck continuing every year whether you want to or not… that’s a little scary.

The conversion ladder is a much more flexible option and easier to implement. You can choose whatever amount you want to convert each year (as long as you are aware of the tax implications) and you can stop the rollovers any time you want.

Because you get taxed on these conversions, you want your income to be as low as possible to ensure you’re in a bracket that gets taxed at the lowest rate possible. So, obviously, your best bet is to wait until you no longer have a regular 9-5 job. And, in my situation, I want to access my 401(k) with my current employer, which I can’t do while I’m working there anyway.

Sounds great, right? The catch is that there’s a five-year waiting period before you can access each conversion of funds penalty-free. Five years! Ouch.

In other words, you’re no longer working and start this process. But, you need to have socked away five years of money already set aside to live off of while your conversion is cooking.

At the time, this was a really tough hurdle for me to get past. We had maybe a year of expenses put aside, but I didn’t know how we’d be able to save the rest of the cash to make this happen. I make a decent buck, but I’m far from a doctor or attorney for sure!

In a weird twist of fate, though, we unexpectedly ended up selling my first rental house. The house was paid off, but it was also run down and in a bad neighborhood. When all was said and done, we pocketed about $40k on it – not a ton of money, but still another year of expenses we had now acquired.

Then, after talking to my new financial advisor, David Jacoby from Remote Financial Planner (who I highly recommend!), we figured out a game plan. It included selling our current house and utilizing those proceeds as well as some of our other investments. This would help cover the remaining years and then some during the conversion.

And sold it we did – I’m actually typing this in my half-empty house right now (fingers crossed the closing goes smoothly this week!).

But here’s the deal – we’re not actually going to be selling off our investments for a while. Yeah, we’ll be doing rollovers from my 401(k) to a traditional IRA at the end of the year, but the stock market prices are pretty much irrelevant.

We’re just going to be selling everything off and then buying similar investments right after. So whether the market’s high or low, the prices are likely to be in the same ballpark during the sell and buy. If we’re still in a bull market, well, we’re selling high and buying high. If we’re in a bear, we’re selling and buying low. It’s really a wash.

Then we’ll be doing the Roth IRA conversions in large chunks on both of our traditional IRAs. When we do our conversions, we plan to do them as in-kind transfers. That means that the investments themselves should transfer from one account to the other – no selling and buying necessary.

More importantly, when we’re ready to start withdrawing our money from our Roth IRAs, we’ll be able to be more cautious about it. Cash is king and with an average bear market of 1.4 years, we can afford to wait it out and not sell-off our investments during a downturn.

In the meantime, we’re going to be spending our cash on hand. So, we shouldn’t have to worry too much about those first few critical years that could be swayed by sequence of returns risk from selling off and withdrawing our investments at low prices.

Additionally, I’m sure there will be some income coming in from this blog as well as some other projects I’m hoping to do in the near future.

And with that, we’ve basically built ourselves some protection in the event of a stock market crash once I leave my job.

2) Roth IRA Conversion Ladder

Recently I was reading a post from Fritz, regarding resilience in the face of market volatility. I was happy to think that we should be in good shape because we’ve basically set ourselves up with our own bucket strategy.

But as I read that, I had an “a-ha” moment. I realized that a stock market crash or good downturn could actually be a good thing in another way for us – our Roth IRA Conversion Ladder.

Initially, our goal was to do our conversion ladder by moving over one year’s worth of living expenses. Then in year 6, we would withdraw year one’s conversion and continue this process every year:

| Year | Amount to Convert | Amount to Withdraw |

|---|---|---|

| 2020 | $40,000.00 | $0.00 |

| 2021 | $41,200.00 | $0.00 |

| 2022 | $42,436.00 | $0.00 |

| 2023 | $43,709.08 | $0.00 |

| 2024 | $45,020.35 | $0.00 |

| 2025 | $46,370.96 | $40,000.00 |

| 2026 | $47,762.09 | $41,200.00 |

| 2027 | $49,194.95 | $42,436.00 |

| 2028 | $50,670.80 | $43,709.08 |

| 2029 | $52,190.93 | $45,020.35 |

| 2030 | $53,756.66 | $46,370.96 |

However, David had another idea, which I liked even more. His thought was to convert as much as we can every year without hitting the next tax bracket (conversions are taxed as regular income).

His thought was to move the money over now while tax rates are favorable instead of taking our chances later on down the line. And the sooner we move it over, the less time the money has to compound and grow in that account, which means we’ll likely be converting a smaller total amount than if we drag this out. Less money converted = less money being taxed.

I knew I liked this guy.

My a-ha moment though was that if a stock market crash happens around the time of our Roth conversions, we can get this done much faster. I’ll be able to start my Roth conversions at lower prices. And with that, I’ll be able to move more over before hitting the next tax bracket.

Let’s use the 2018 income tax brackets in our example since we don’t know what the 2019 numbers look like yet:

| Rate | Individuals | Married Filing Jointly |

|---|---|---|

| 10% | Up to $9,525 | Up to $19,050 |

| 12% | $9,526 to $38,700 | $19,051 to $77,400 |

| 22% | 38,701 to $82,500 | $77,401 to $165,000 |

| 24% | $82,501 to $157,500 | $165,001 to $315,000 |

| 32% | $157,501 to $200,000 | $315,001 to $400,000 |

| 35% | $200,001 to $500,000 | $400,001 to $600,000 |

| 37% | Over $500,000 | Over $600,000 |

According to the table, that means we can have up to $77,400 in reported income before moving into the 22% bracket. Now, I plan to leave the taxes to smarter folks like my accountant (which will also be David for the time being) so don’t jump all over me on the specific tax laws. Nevertheless, if we keep things simple just for this example, let’s assume we don’t have any regular income (though we will have some from some pass-through LLCs) and leave out credits like the Child Tax Credit.

This gist of this would mean that if we converted over $77,400 from our traditional IRAs to our Roth IRAs, the marginal tax rates mean we would pay just over $8,900 in taxes on it:

10% on the first $19,050 = $1,905

12% on the remainder of $58,349 ($77,400 – $19,051) = $7,001.88

Total = $8,906.88

Let me remind you again that I’m far from a tax expert, but this sounds like a pretty good deal to me. And if everything remained constant (which it won’t), it would probably take us over 10 years to complete our conversions.

Regardless, things change (including tax laws) and it would be great to get all the conversions sooner than later while the tax rates are low. Now imagine that a stock market crash occurs and our investments lose half of their value.

With those same brackets, we’d be able to convert twice the amount over from the traditional IRAs to the Roth IRAs for that year (or years). Depending on how long the downturn was we’d be able to push a lot more through than we would otherwise and we’d pay a ton less in taxes over the long haul.

Think about it – if we get done early, that means we have a few years we won’t have to do conversions any longer and that’s a few years where we wouldn’t have to pay those taxes. That could easily save us tens of thousands of dollars!

So that’s it – as weird as it may sound, I’m now rooting for a market crash!

Are you prepared for a stock market crash or solid downturn? Are you looking forward to it or dreading it?

Thanks for reading!!

— Jim

Jim, buy low, sell high! Market drops are an opportunity to invest at a lower cost.

Make sure you take into account other income when looking at the conversions. You do highlight that the $774,00 is “reported income.” Tax brackets above are based on adjusted gross income (AGI). AGI includes salaries, taxable income/dividends, capital gains/losses, etc…plus any IRA conversion amounts.

Time the conversions in the last part of a calendar year. Doing it later allows you to better estimate other income streams and the impact on your AGI to ensure you do not convert too much that results in you hitting another higher tax bracket.

Thanks, Mr. r2e – that’s exactly what we had planned. At the end of next year, we’ll do a mock-up of our taxes to see where we stand and determine how much we can convert.

Your point about the other income is well-stated and important. I was hoping to keep the idea simple for others, but maybe I should have gone a little more in discussion about understanding that you have to take into consideration other income on this.

— Jim

Interesting thought on the market crash! I hadn’t thought of it as an ideal time to do a conversion.

I’m in a similar situation (although I didn’t realize it until reading this post) where if the market did drop I would be able to tax-gain harvest a larger portion of my taxable account each year and then rebuy those same funds immediately. If there was a market drop, I would be able to zero out my cost basis while paying less tax now. Neat idea I hadn’t thought of!

Great idea, Adam!

— Jim

Hey, that’s good. I never thought of it that way. Converting to Roth is a buy-in point. It’ll be good timing if the market crashes next year, I guess. You can move more money to Roth if the market is low.

I’m somewhat dreading a market crash. It’s not going to feel good, but let’s get it over with. The earlier the better because Mrs. RB40 plans to retire in 2020. Even with your reasoning, I don’t want a crash as she retires. The Roth conversion is just a small piece of our finance. A market crash impacts the whole thing.

Yeah, I’m with you on getting the downturn done and over with, but I’m trying to look at the glass as half full and take advantage of the opportunities that come to light! 😉

— Jim

Well, you’re getting your wish! 🙂

Good times are over, but that’s why I ain’t gonna stop working online. Gotta pay for some new shoes!

Love it! I need some new shoes, too… except I get mine at Kohl’s so I probably don’t need to save as much as you! 😉

— Jim

Jim :

A good strategy, but I am a bit confused. When the market crashes, you can’t convert more money to a Roth at the same tax rate. The tax thresholds haven’t change. I think you meant to say you can convert a higher percentage of your 401/Traditional IRA to a Roth within the same tax bracket, since the $1,000,000 may now be worth only $900k.

I think one advantage of a market dip before retirement is that the initial 3.5 or 4% withdrawal becomes less. The dip creates a built in safety net of conservatism. And it only represents maybe $4k a year on a 100k dip. That doesn’t seem like a deal breaker for escaping the cubicle.

Yup, that’s exactly what I was referring to, Kev – the dollar amount would still be the same, but we be able to move a higher percentage over because of the value.

— Jim

Jim, thanks for the shoutout on my “volatility” post. Once again, we’re in agreement that a downturn would be an opportunity to increase Roth conversions during the downturn. I also wrote a post a while back about the opportunity presented by the new tax law to increase conversions (see

http://www.theretirementmanifesto.com/the-new-tax-law-a-loophole-for-retirees/

I like the way your new advisor thinks. Amazing minds, indeed.

I like when I get confirmation on these kinds of things from you, Fritz. More importantly, though, you’re like a walking marketing machine – I love it! 🙂

— Jim

Great charts! I get nervous when I start thinking about those first few years when I’ll be doing conversions. Turns out there are pros and cons to retiring during either a bull or bear market!

So true, Nickel – if you’re prepared for the inevitable, it can be a win either way. 🙂

— Jim

Thanks for this post! I sometimes get panicky about maxing out pre-tax accounts and have to go reread one of the Mad Fientist articles to reassure myself. So it’s good to see someone else is doing too.

I like the optimistic position and you bring up a great point…you could get everything converted faster if you do it during a downturn. I wonder if that would also be a good time for those of us still stuck in the race, and paying higher taxes, to do a small conversion just due to the values being lower. Hmmm.

Haha, we’d definitely need the Mad Fientist to do the numbers on if that makes sense to do! 😉 I think everyone’s situation would be a little different for that. First off, you’d probably have to already have the money in a separate traditional IRA (or old 401(k) floating around) since you generally can’t roll over a current 401(k) or similar plan unless your plan allows it. But then, yeah, that would mean every penny you convert would be at a much higher tax rate and that could negate a lot of the benefits… but you never know!

— Jim

I’m thinking of retiring in the next few years and wouldn’t mind a downturn now to “get it out of the way.” I have been building up our cash to get us to a point of 3 years of living expenses, so I should be OK over the next few years. I hadn’t thought about how a market downturn would mean depressed IRA value and being able to covert a greater percentage to Roth; it’s brilliant. I would love to do Roth conversions in early retirement, but I am also looking at trying to keep our income low so we can get some good subsidies for health insurance. I guess it will eventually have to be a balancing act.

Yeah, that health insurance dilemma can definitely throw a wrench in the works. Obviously, our situation is a little unique since we’re leaving the country, but I think you’re nailing it on the balancing act. You’ll probably need to run the numbers a few ways to determine the optimal strategy for yourselves. Congrats on being able to retire soon – if you’re still a little “iffy” on it, you might want to check out the post I wrote for the ESI Money site recently – https://esimoney.com/how-to-get-up-the-nerve-to-retire/.

— Jim