Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

When I started to get a little more serious about reaching financial independence a few years ago, I started dipping my toes into different ideas as I learned more about them. One of those ideas was to start investing in dividend stocks.

When I started to get a little more serious about reaching financial independence a few years ago, I started dipping my toes into different ideas as I learned more about them. One of those ideas was to start investing in dividend stocks.

Dividend stocks are great because you don’t usually focus as much on appreciation as you do on the regular payoffs you get from the stock. That means passive income, which is something we all know and I love. I look at some of the successful investors such as Jason at Dividend Mantra and see that dividend stocks can be an excellent addition to your portfolio.

DRIPs

In addition to the cash flow you get from dividend stocks, many companies allow you to enroll in DRIPs when you buy their stock directly from them. DRIPs are Dividend Reinvestment Plans that take the money you would be receiving as a dividend and put it right back in to buy you additional shares of the investment.

What’s cool about this is that these additional reinvestments don’t require buying full shares. So if you get a $2 dividend for a stock that’s currently trading at $100, being enrolled in their DRIP would buy you a fractional share of the stock – 0.02 shares in this case. Over time, these fractional shares can accumulate and help build up your investment in the security.

Pretty cool, right?

Enrolling in DRIPs directly with the company bypasses the broker and their commissions. I’m guessing that brokers don’t like this – obviously they want all your cash to be with them instead. Both my Roth IRA and my wife’s which are with TD Ameritrade and they allow you to enroll in a dividend reinvestment program directly through them. This benefit through TD Ameritrade covers most securities and they don’t charge commissions on the reinvestment. So of course I turned this on for all my investments with them once I found out about it.

Down the line, if you accumulate enough dividend income from these stocks, you could turn off the DRIPs and either supplement your regular income or in some cases, actually live solely off of the dividends.

Sounds good to me!

I came across a list of S&P 500 Dividend Aristocrats which made this seem pretty simple. The Dividend Aristocrats are companies that have increased their dividend payouts for 25 consecutive years.

Easy enough – hard to go wrong here, right?

I started buying stocks in my Roth IRA based off the picks I “felt” were companies who I know and trust… because who needs research when you have instinct?!! Ok, probably not the best idea, but that was then.

Starting with a Change in the 401(k) Plans

Over time, I learned that picking stocks isn’t necessarily a great idea, especially when you’re just guessing like I was! 🙂 Obviously, the biggest problem with picking stocks is that you’re putting a lot of your eggs in one basket. If one of the companies in your portfolio fails, that can put a pretty big hurt on things.

I also learned to simplify. I was getting caught up in all the noise and not seeing the forest for the trees. Then I listened to a podcast from the Mad Fientist where Jim Collins from jlcollinsnh was the guest. This turned out to be an eye opener for me. If you’re not familiar with Jim, he encourages his readers to tune out the hype and focus on index funds. He’s known for his multitude of articles grouped together and called the Stock Series. If you’re unfamiliar, be sure to check it out.

After hearing him on the podcast though, I got it. It made sense and since then, I realized that I was just missing the message out there – a lot of personal finance bloggers have been preaching this same point for years. Either way though, I finally understood.

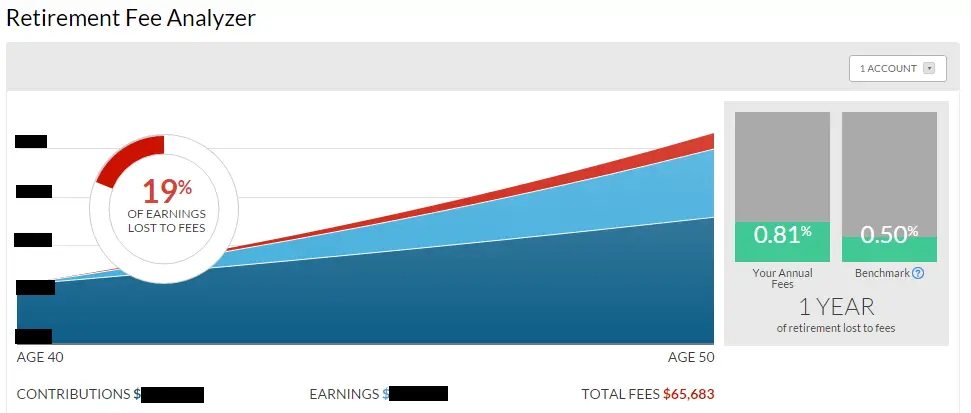

After that, I went in and changed the investments in my 401(k) plan to all be in one extremely low-cost index fund. I did the same with my wife’s account. Empower (formerly Personal Capital) has a wonderful 401(k) fee analyzer that can show you what your 401(k) is going to cost you in fees by the time you retire. My 401(k) alone was going to have cost me over $65k in fees – and that’s with me retiring early!!! Here’s a snapshot of the before:

What makes this even worse is that a couple of years prior, I had already gone in and changed my investments to lower my fees from about 1.5% – ouch! If I had run this analyzer back then, I probably would have had a heart attack.

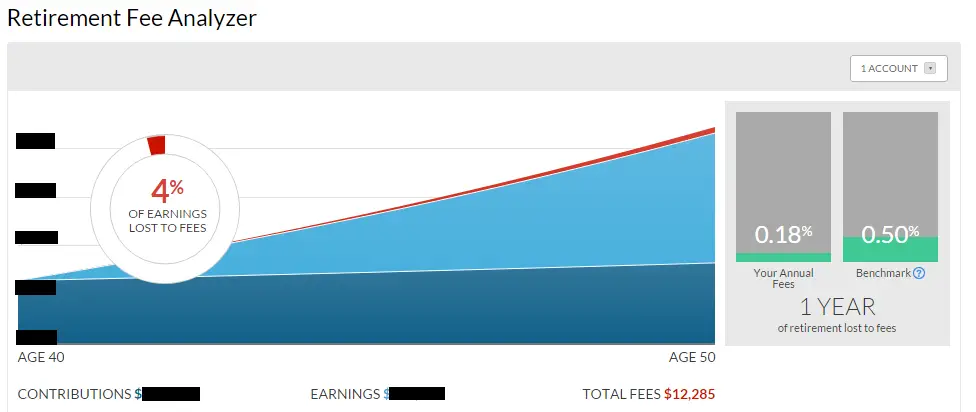

But after making the changes to one low-cost index fund, I’m now looking at around $12k in fees:

It still makes me want to throw up, but a $53,000 savings in fees does make me feel quite a bit better.

Take a few minutes and sign-up at Empower (formerly Personal Capital) and do this. The analyzer is completely free, easy, and takes only a few minutes to run through:

Wringing Out the DRIPs

So with that first mission out of the way, I moved on to other things. Recently, I went to a financial advisor for a second opinion on my retirement game plan. Things went well and he agreed with a lot of what I was doing, but then…

He tried to be a little bit tactful when he brought up my Roth IRA, but I could tell he had an opinion on it and was just trying to come up with the right words. I made it a little easier on him and interrupted…

“You’re wondering what the hell I’m doing with the investments in my Roth account, aren’t you?”

“Exactly” was his response.

So I explained to him that most of the stocks were purchased before I knew what I was doing (though some could argue that I still don’t know what I’m doing!).

Long story short, his recommendation was that I sell everything in there and buy index funds. Like I said, having a lot of your portfolio in individual stocks can be more dangerous than spreading the wealth with one investment containing thousands of securities instead.

So I had to make a decision – listen to the advice of a trained professional or go with my own thought process. Some of these stocks I didn’t want to let go but I do know that index fund investing is the smarter move.

So I decided to split the difference. I sold off a few of the stocks that I no longer wanted right off the bat. This actually made me feel a little better with that move alone – some of the stocks I had in there weren’t even dividend stocks that I had thoughtlessly bought a decade or so ago.

My next move was to shut off all DRIPs with TD Ameritrade for my Roth IRA as well as Mrs. R2R’s account. By doing that, the dividends will just stack up as cash in my account.

I decided that all my future investments in our Roth accounts will be to buy shares of Vanguard Total Stock Market ETF (VTI). I bought a number of shares in VTI and all future contributions and dividends will be invested in it as well. I also enrolled just the VTI ETF in the DRIP program through Ameritrade as well.

I like the VTI ETF because Ameritrade doesn’t charge a commission on it and the expense ratio is only 0.05% (that’s extremely low!!). The fund has over 3,000 stocks in it and aims to track the performance of the US Total Market Index.

The kicker to all this… it pays off dividends as well. What was I thinking?! I should have done this long ago.

I enjoy making strategic moves like these. Beating the market is something that’s generally not attainable (or not for long periods of time), but optimizing my accounts is something that I’ll continue to strive to do to put myself and my wife in what I think is the best position I can.

Are you a dividend stock investor? Do you buy individual dividend stocks or mutual funds/ETFs that pay dividends?

Thanks for reading!!

— Jim

Disclaimer: I’m long Vanguard Total Stock Market ETF (VTI).

We’re still selling off some individual stocks from my early years of investing, but all new holdings for the last 5 years are index funds or index etfs of some sort. I do hold one dividend fund, but thats been out there for 6-7 years and I no longer invest in it because the expense ratio is to high. I’m happy to collect the S&P500 dividend and appreciation.

Sounds like are paths are pretty similar. Just out of curiosity, is there a reason why you’re hanging onto the dividend fund instead of selling it and buying a lower expense ratio fund?

— Jim

Great post. Dividend reinvestment is a great way to snowball your returns. I’m also a strong advocate for the index fund path, there’s no easier way to diversify and simplify your retirement account. My biggest obstacle in retirement accounts have been expensive funds in 401K accounts that I have little control over.

Thanks, Jake – I got lucky that we offer a Vanguard fund in my 401(k) with a low expense ratio. My wife’s 401(k) plan sounds as great as yours 🙂 – she didn’t have a good fund to choose from, but I was able to trim it down to a 0.88 ratio… not great, but at least it was somewhat of an improvement.

— Jim

.88 is not bad considering some of the alternatives. In my last job there was an optional management fee of 2% to essentially have a rep pick the most expensive funds for you.

I opted to focus on my tax-sheltered IRA accounts and only contributed the max matched amount to that 401k, without the service fee :D.

2%… ouch! I like your choice much better. 🙂

— Jim

I’ve got to say it Jim — There’s more than one way to skin a cat.

Yes, I know most of the personal finance blogs out there trumpet this exact same advice “buy index funds”…and it’s certainly decent advice.

But index funds aren’t the only way to invest. I’m living proof of that. I hate that the blogosphere treats it like the only answer. Some people invest only in real estate. Other just in bonds. Some in private companies. There’s a million ways to invest!

BTW: I’ve never used DRIPs. I always found them good in concept, but in execution it meant reinvesting money at the wrong time and occasionally in the wrong assets.

I definitely agree that there are a lot of different ways to invest. Maybe I made it seem a little too narrow on this post, but I invest in other opportunities as well (such real estate).

As far as the stock market goes for me personally though, index funds seem to be a better answer. I don’t find myself getting caught up in the “is Home Depot up or down today” and it simplifies things in my portfolio. I also like that I don’t have to worry about one stock going bad and crushing a portion of my Roth.

As a side note, what kind of investments have worked best for you?

— Jim

Mr. Tako,

I think the so called blogosphere holds index funds in such high esteem is because they’re so simple to implement. They’re not the only answer but they are the only easy answer that fits most people’s retirement goals.

Investing in real estate or private companies requires a lot of capital, bonds are a bust and individual stocks can be risky. An index fund is sort of the catch-all to call these obstacles and they’re easy to “sell.”

I do both. My 401k is running a total market fund with extremely low fees and great dividends. I have a traditional IRA also doing index funds, but I use my Roth to do some DRIP investing with some of the dividend aristocrats as I save up a little bit extra to do so.

I was talking to a friend of mine at work today and he’s doing the DRIP investing with dividend aristocrats in his Roth as well… kind of funny how we all are seem to think along the same lines! 🙂

— Jim

90% of my investments are in passive index funds that pay dividends. The remaining 10% are stocks that I play around with. For the most part they are dividend paying but a couple of them are not.

But I am like you in that I love dividends especially since I can turn on a DRIP and forget all about it and watch it grown and give me more shares 🙂

That was pretty much the same pattern as I was following with the “playground” on the dividend stocks until my financial advisor beat me with a stick! 😉 I didn’t fully listen to him though – I do have a handful of individual stocks that I did decide to hang onto so he can yell at me more sometime down the line.

— Jim

I invest in individual stocks and index funds on a regular basis. I chose DRIPS whenever offered by companies I am invested in. If there is not such a scheme, I collect the cash dividends to buy additional stocks of that company or to diversify in new holdings. After some years I could recognize the “support” of the compound effect. It works even more in favour of a long term investor when markets are flat or retreat for some time.

Cheers

Sounds like you have a great system in place to help build up your investments – nice work! 🙂

— Jim

I do still stock pick specific companies for my portfolio. It’s a hobby. I’m putting about 10% of our investments into this stock portfolio, the rest goes into index trackers. Feels pretty secure. The stock portfolio tends to be between 10 and 15 companies, that seems to be the most I can keep an eye on in my spare time.

I do sometimes feel like I should stop doing it though, just transition to full index funds. Saves a ton of time. And I have plenty of hobbies already 😉

Nothing wrong with that, Mr. Thinkbig – and like you said, it’s just a small part of your portfolio. I actually know a couple of folks who are FIRE and dividend stocks are the far majority of their portfolio – they live completely off the dividends. Definitely not my hobby though… I’ll stick with the simplicity of index funds any day! 😉

— Jim