Retirement money is definitely something you shouldn’t be gambling with. But hey, it’s only your future on the line… what could go wrong?

Retirement money is definitely something you shouldn’t be gambling with. But hey, it’s only your future on the line… what could go wrong?

I admit it – I love gambling. That’s not something you’d expect to hear from a blogger in the personal finance community, but it’s true.

I’m not an avid gambler – I just enjoy some table games or video poker at a casino every now and again. Sometimes I’ll even throw a little bit at a periodic game of Keno at the bar (worst odds ever!).

Of course, I like it more when I’m winning, but I only play with money I’m prepared to lose.

And please don’t take this as me being a casino regular with a major gambling problem. We’ve lived a mere one mile from a Hard Rock casino for the past 5 years and I think I’ve been there four times – mostly because people in town wanted to go check it out.

So why would I gamble with just shy of $700,000 in my IRA?

Here’s the scoop…

401(k) to rollover IRA

As you guys know, I was able to retire from my career at the end of 2018, which has been wonderful so far.

You might also be aware that part of our drawdown plan is to utilize the retirement money in our former 401(k) plans to fund our lifestyle. We’ll be doing Roth conversions to get access to our money before the “official” retirement age. Doing the conversions correctly will help us avoid any penalties along the way.

With me no longer at my former employer, I can now take control of my 401(k). We had recently changed 401(k) providers at work and the expense ratios actually went up in some areas, so I’ve been looking forward to getting my money out of there anyway.

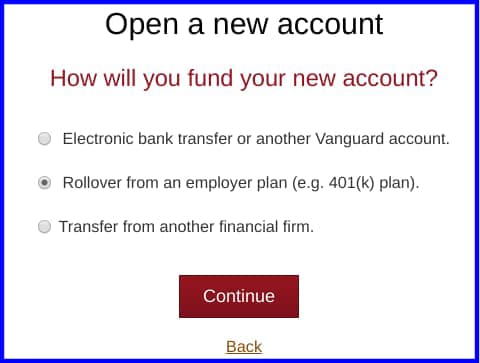

Once my profit sharing posted into my account, I pulled the trigger on the rollover. I opened a new Rollover IRA at Vanguard where we have most of our other accounts.

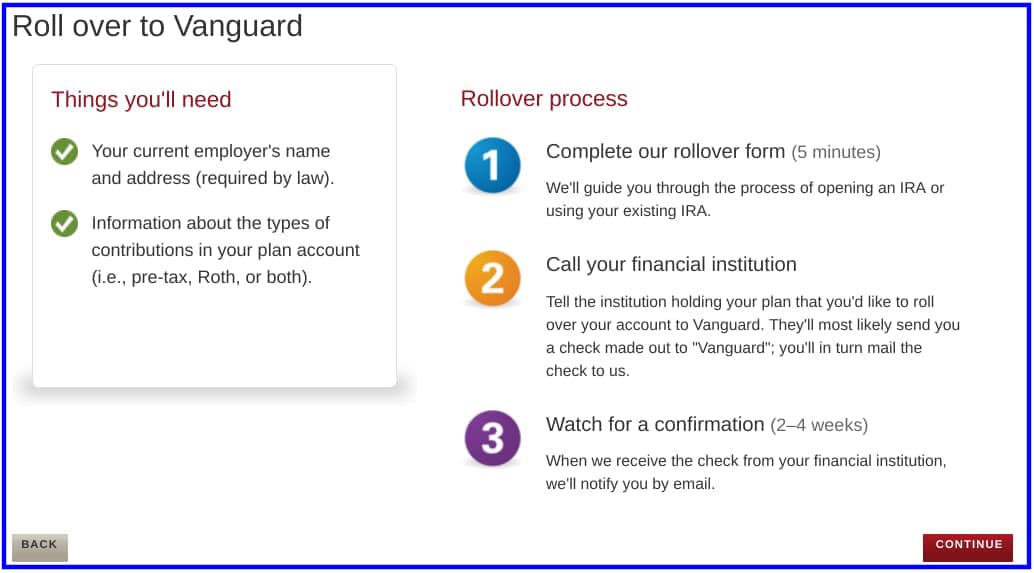

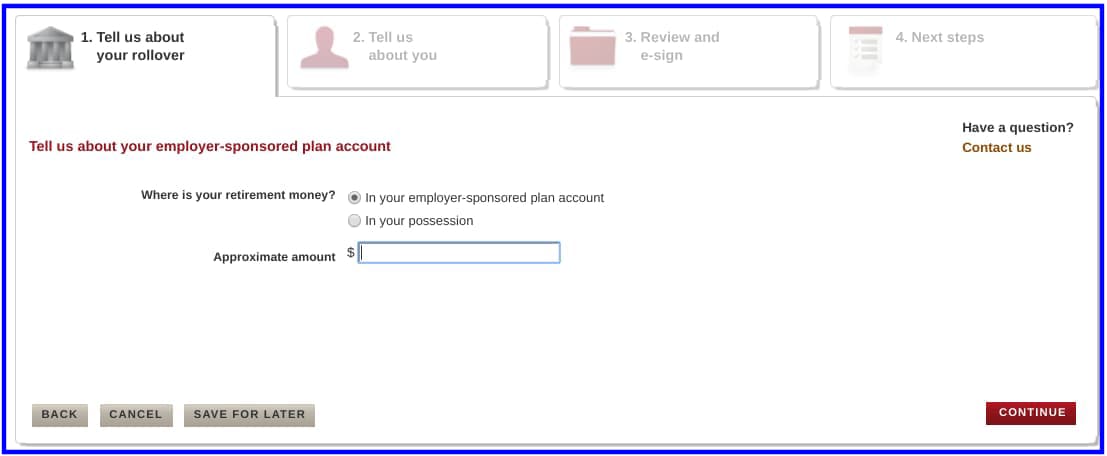

The process is simple enough and one I was familiar with from rolling over Mrs. R2R’s account a couple of years ago. You answer a few questions and – boom – you’re account is ready for the rollover. Here are some screenshots on the process with Vanguard if you’re interested…

After some personal info questions, they’ll give you instructions on how to inform your current institution of the rollover. Once you make that happen, the current institution will “color you up”, so to speak, and sell off everything in your account.

Sometimes this can take a few days. I got lucky that the market was at a pretty good peak on the day they sold, but you really never know because it’s completely out of your control.

Instead of sending the funds to the new company, they’ll likely mail you a check for the full amount of your account (minus any transfer fees… bastards!). The most important piece though is that the check is made out to Vanguard (or whoever you’re rolling it over to) and not to you.

Once you get it, you turn around and mail the check to Vanguard. It’s stupid that you play middle-man on this process, but that’s the way it goes. So then you pace back and forth in worry with the fear that the check got lost in the mail until you actually see the funds show up in your new account.

When Vanguard has everything processed, they shoot you an email to let you know you’re good to go.

The gamble

I sat down in front of my computer and logged into my Vanguard. All my money from the rollover was there ready to trade… $691,298.37.

My plan was simple… we have things allocated the way I want ’em across our accounts and this account is just going to be all Vanguard Total Stock Market ETF (VTI). As a reminder, I’m not your advisor so don’t just blindly follow what I do… talk to someone a little smarter than the guy telling you about gambling with his money.

So I was just about to pull the trigger on buying all the shares of VTI I could… but then I hesitated.

This is a lot of money – like a lot. This one transaction can have a decent effect on our future.

What if I buy it all and the market tanks tomorrow? I would have just overpaid for the bulk of the wealth in our account.

The logical part of my mind knows that I should just go for it and be done with it. If you’re not familiar with Jim Collins, he wrote a phenomenal series of posts called the Stock Series that can put the entire market into perspective (fantastic read!). He even addressed what I’m talking about right here.

Sure, but… That “but” is usually a bad idea brewing.

There’s the part of me that thinks:

- The market’s been bouncing all over the place lately – this can work to my advantage.

- There’s no rule that says you can’t sit on a pile of cash for a little bit. A week or two – or even a couple months – isn’t likely going to cause you to miss out on a ton of growth.

- Even a small move in the market would make a substantial difference in how many shares I could buy.

I hear you. You’re already thinking, “Jim, quit trying to time the market and just buy now!”

Well, that last bullet point got me thinking. On 3/1/19 (the day I was ready to buy), shares of VTI were a little over $144 per share. Just a couple weeks earlier, shares were at $138 and a couple of months earlier on Christmas Eve, they hit a low of $119.70.

Now, I don’t want to do a lot of gambling with the bulk of our retirement money, but I also don’t want to just shoot the j and buy at the peak.

I ended up doing some quick math and set $140 as a nice even number that was still reasonable. If I could get the shares at $140 each instead of $144, that would be a pretty good deal:

$691,298.37 / $144 = 4800.683125 shares

$691,298.37 / $140 = 4937.8455 shares

In other words, I would be able to get an additional 137.162375 shares by getting it for $4 less per share. At the $144 price, that would end up being worth a $19,751.38 difference… that’s a hefty sum of money!

Decisions, decisions.

I talked with Mrs. R2R to get her thoughts. We decided it was worth a shot, but only for a short period of time. If after a few weeks, the price didn’t drop, we’d buy regardless – either all of it or incrementally over another few months.

We also knew that this was a gamble. If the price goes up, that $19,751 difference could be a swing in the other direction… and I would cry.

Ah, what the hell – you only live once! I put a limit order in for $140 per share for everything I had as a good ’til canceled (GTC) order.

Come on, lady luck – baby needs a new pair of shoes!!

Can you really call this a retirement money gamble?

Yeah, this is definitely a gamble – any kind of market timing is.

It’s possible that if I had simply purchased the stock and called it a day, the price could just continue to rise. I could be missing out on some big potential gains by this little waiting experiment.

On the other side of the spectrum, I have the potential for a fantastic gain as well.

It really is a toss of the dice. So, yeah, this is a gamble.

But if I didn’t do this, I wouldn’t have this fun post for you guys to read!

And I think this is a kind of a controlled gamble to a point. I’m watching the market closely. If the price starts to take too steady of a climb, I might just call this off, accept my loss and buy in.

This just in…

My retirement gamble ended before I even got to finish this post.

My order got triggered on 3/8/19 – one week after I put the limit order in. I got an email and got the whole lot of my shares at $140.

I watched the market for the rest of the day and the price slowly went up after that. That made me feel good.

You were probably hoping that I lost all our retirement money and had to go back to work. I mean gambling is bad and should end badly, right? Yeah, well, not this time and I’m happy things went well.

However, in all reality – this doesn’t mean much. It’s very possible that the @#$% hits the fan tomorrow and the shares drop to $120 each or $100 each. Will that mean my gamble was a win or a loss?

You could look at this in a few ways:

- Smart move, Jim! You made your portfolio more valuable than it would have been if you hadn’t waited. Well, thank you, thank you very much.

- Thumbs down! You should have waited longer for the price to drop even further. Then you could have made some real retirement money!

- What the what?!! Why would you have even tinkered with your retirement money? You’re an idiot. The best idea would have been to not gamble with your money and sensibly do one of two things:

- Just pull the trigger immediately and buy it for whatever the market price is. If you’re holding for the long run, today’s price isn’t going to matter that much.

- Spread out your risk out over a set amount of time (maybe a year or two) and buy a smaller amount of shares at market price every month… dollar cost averaging.

Don’t do what I do – although things went well enough for me, this could have easily gone the opposite direction. And then this would have been a completely different post filled with some tears and heartache.

Let ‘er rip… why, in your right mind, would you take any chances on your hard-earned retirement money?

Thanks for reading!!

— Jim

Hmm, this whole thought process behind the post is kind of funny and entertaining to me. I guess we all have a sense of what is risky. Some people day trade options and others limit order a total market ETF. I do have a slight bias away from limit orders in that anytime something drops to your price, it is unlikely that it immediately turns around once that price is hit (ie the catching a falling knife problem). Thanks for sharing

Yeah, I’m definitely not a market timer so doing a limit order isn’t something I’ve done too much of. I’m glad it worked to my advantage in this case, but you’re right – the sell might not have trigger right away in some circumstances. That could have made things end a little differently! 🙂

— Jim

Entertaining post! Well done on timing and also communicating what was happening wit your wife.

Ha, yeah, we’re a team and that could have made for an unpleasant matter if we didn’t talk about it first and things didn’t go my way. 🙂

— Jim

I’m guessing there was just a bit of buyers remorse at $140. (“Dang, should have done 1/2 at $138?). Haha. Good move to take the odds with the market’s volatility. In 10 years, it probably won’t make any difference, but it was a fun little gamble that paid off. Well done!

Haha, I’m too much of a sissy gambler, Fritz – I take my “winnings” and don’t look back at what it could have been! 😉

— Jim

I don’t really call that what you did gambling Jim. You simply set the price where you wanted to invest and walked away. If the trade didn’t work out, you were out *nothing*. That’s not gambling Jim!

Gambling implies you take the risk of losing some or all of that money, but in this case you wouldn’t lose anything as a result of your actions.

At least that’s how I see it. 😉

I like your perspective – for me, something like this gives me that same bit of nervousness like it being possible that I miss “today’s price” and get stuck paying a lot more later because I was playing games. That’s why I considered it a gamble, but the important thing is that I got it at the price I wanted so all’s well that ends well! 🙂

— Jim

What not VTSAX? Is there an advantage of buying the ETF version?

Thanks,

Hi HospitalistDoc – VTI and VTSAX are identical. The only difference is that VTSAX is the mutual fund version and VTI is the EFT. They both have their pros and cons, but I prefer the ETF.

An ETF trades like a stock so you can buy it anytime the market’s open and get it at the going price. A mutual fund takes place after the market closes for the day. Depending on your perspective, either one of these could have the upper hand, but I like that about ETFs.

However, ETF’s you have to buy in full shares – mutual funds you don’t. Being able to buy partial shares with mutual funds can be advantageous for many folks.

ETF’s tend to be more tax-efficient. If you have the funds in a retirement account, this doesn’t matter, but it could be important if it’s just in a taxable account.

I’m not the expert, but I just decided to stick with VTI for my needs. With the exception of some minor differences, though, it’s the same thing. Here’s a good link on those differences that might shed a little more light… “ETF vs Index Mutual Fund: Which One’s Better?”.

— Jim

No advisor would ever tell a client to plunk $700k into the market at once. Especially not after one of the longest bull markets in history. Not just a gamble… A dumb one.

Very true, Jack. It’s worth remembering though that this was money that I had also just pulled out of the market as well. The plan was just to roll it over to the new account and make it pretty much an even trade. I ended up coming out ahead on that deal so I’m satisfied, but you might be right that spreading out the investing could have been even better. On the other hand, it’s also possible (as unlikely as it seems) that this insane bull market could continue even longer. I personally doubt it, but none of us really can predict that one.

— Jim

Ah I know this feeling well. I always use limit orders. The last time I thought Don’t time the market! and just bought on a Friday instead of waiting for Monday, I was happy to get shares of a stock for a certain price. It was a Friday in early February 2018. The order went through because it was the day the market started a freefall. By Monday or Tuesday, it was $10 lower.

It would be over 5 months before the stock climbed back to what I bought it for.

But I shrug. I didn’t lock in a loss and we’re in it for the long haul.

Ugh, that feeling sucks. But you said the magic words – we’re in it for the long haul. Most of us think we’re smarter than the market and we end up tripping over our own feet. Your attitude about just shrugging and realizing that you should come out ahead in the long run is the best way to handle it.

— Jim

I have done this for years but now I have price targets on Vanguard targeted funds. The last time my money went in was December 24th. I have been doing this since 2007. I always have the capital gains and dividends invested into money market fund. Have an entry and exit number on a white board in my office. Very simple, low cost and well diversified and always wins….

That’s awesome, Joe! Having both and entry and exit number that you can live with can make that a good system. This was likely a one time event for me though – I’d rather just keep investing the money as I get it and not think too much about it. 🙂

— Jim

I think it’s okay to time the market especially when you’re trying to be more conservative.

If it didn’t trigger, you still have the cash. It’s not like you lost anything. I’m holding more cash than usual this year too. The market is too volatile for me. I’m being extra conservative.

I’m not a good gambler because I hate losing money.

Haha, I don’t think any of us like losing money! 😉 This market is insane – every time I think, “Yup, this is it, the bear’s finally on its way.”, it climbs right back. I do like your idea of holding more cash than usual right now. I’m a little on edge about the volatility as well.

— Jim

shoulda considered allocating a portion to qqq (nasdaq 100 index). it’s been killing vti over the past 15 years.

I haven’t heard of QQQ, Freddy – I’ll have to dig into it. Thanks for the heads up!

— Jim