You’re doing your best to get yourself on the right track with your finances. You’re working your way out of debt and have turned your eye toward reaching financial independence. But the media wants you to focus on the money you have coming in. I want you to focus on your expenses instead.

You’re doing your best to get yourself on the right track with your finances. You’re working your way out of debt and have turned your eye toward reaching financial independence. But the media wants you to focus on the money you have coming in. I want you to focus on your expenses instead.

First of all, know that your income is important – no doubt about it. In my article The Steps to Wealth, the first thing I talk about is getting a high-paying job. Is that the end-all and be-all in reaching financial independence? Certainly not, but bringing in a higher salary can make the steps of the journey much easier.

However, even if you do have a lot of money coming in, that doesn’t mean you’re going to be successful in reaching financial independence.

Why?

Because if your expenses are too much in comparison to what you make, then it doesn’t matter how much you bring in – you’ll have a hard time getting your financial independence number where it needs to be.

Let’s start off with this…

A lot of retirement articles are full of $%#&

So here’s something that has been getting on my nerves lately… a lot of the retirement articles you’ll find on the Internet are focusing on the wrong side of your money.

So here’s something that has been getting on my nerves lately… a lot of the retirement articles you’ll find on the Internet are focusing on the wrong side of your money.

They seem to float around the idea of basing your retirement off of your income rather than your expenses.

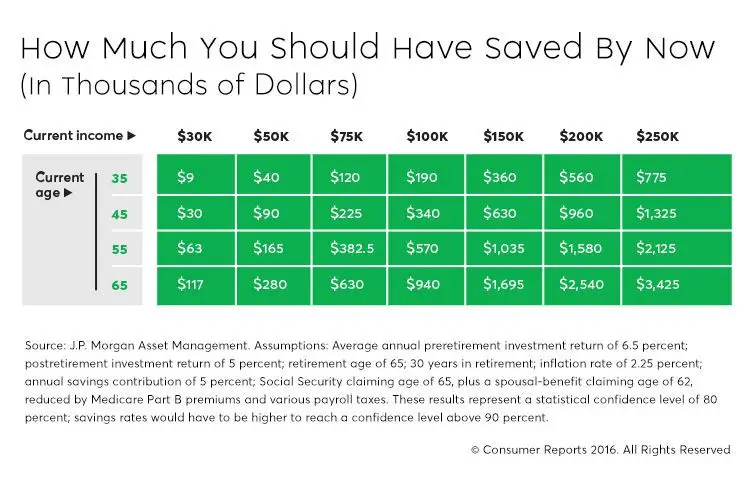

Here’s a perfect example – Are You on the Right Track for Retirement? The article looks at how much you should have saved up right now for retirement based on your age and income.

I get it – it’s a nice easy way to try to help people figure out how much they should have in the bank.

The problem with retirement articles like these is that they want you to think that you need to base your retirement on how much money you’re making right now. Sure, you can absolutely do this and come out ahead in the game.

But take a closer look at the small print on the article… there are a lot of assumptions in it. This one goes off the basis that you’re trying to retire at 65. It also assumes that you’re socking away only 5% of your money.

And by the power of deduction, that means it’s also presuming that you’re spending the other 95% of your money.

That’s insane!!

This problem seems to be more with commercial publications writing these kind of retirement articles. If you hang around the FIRE (Financial Independence, Retire Early) community long enough, you’ll notice that this isn’t the case with most of these bloggers and writers. They understand that putting your sights on your expenses is the smarter path to financial independence.

With you reading this, it’s likely because you’re working to take control of your financial future. That said, hopefully you have higher expectations that those assumptions. Many of you want to be able to quit your job earlier than 65.

So yes, you can plan for retirement by basing everything off your income, but that means you should plan on continuing to make the donuts every day for a long time.

The smarter move is to is to focus on your expenses.

Imagine how much different that table would look if you started to put away more than the stated 5%. You could reach that point of financial independence even sooner. And the best way to do that is to focus on your expenses.

A surprising thing happens as you control your expenses and put more money away. The more money you’re socking away, the less money you’re actually living on. So what happens is that you don’t need to rely on what your income is to survive – you only need to base your number off of your expenses.

Get the point?

Living off less money will allow you to save more and reach a goal of becoming financially independent sooner. In other words, It’s Not How Much You Make, It’s How Much You Keep.

What expenses you can control to get you there sooner depend on your situation – everyone’s scenario is different. But some of the things that you should start with are the areas that could have the biggest impact on your expenses.

Your home

Your home

For instance, if you own a house, moving to a smaller or less extravagant home can make a dramatic difference in your life. A lower mortgage payment would greatly reduce your expenses and put more money in your pocket to put toward your future.

In addition, a less expensive house generally means a lower cost on property taxes and insurance. Plus, the area of maintenance and home repairs can be lessened as well.

I’ve personally started looking at the possibility of moving to a less expensive home. We’ve tabled the idea for the time being until we determine if we are going to move to Panama, but if we don’t then we’re going to seriously consider this option.

Your cars

Your cars

A lot of you probably just glanced over the idea of moving to a new house and that’s Ok. It’s definitely something to at least think about, but if you can’t make that leap, then you need to start looking at other big expenses.

And that should take us right to the idea of cars. If you’re in New York City or another big metro area where might not even consider owning a car, this might not apply to you.

But for many of you, you might own one or more of these tin cans chock full of expenses. And many of you need those cars to get to work. And that’s Ok as well.

But do you really need a gas-guzzling SUV or a brand-new luxury car? Probably not. If you’re serious about reaching financial independence and your expenses are too heavy, this is a great area to cut back on.

Another tricky area is the lease trap. Although the payment is usually cheaper than buying a new car, many people get stuck with the temptation to lease forever. If you’ve ever paid off a car before, you know that there’s nothing like that feeling of not having that payment every month. If you get stuck in the lease trap, you’ll continue to waste money month after month.

I own a 2009 Chevy Malibu and she has a 2011 Ford Escape (both that we did buy new) and we’re going to run them both into the ground. Mrs. R2R and I have both decided that we won’t be buying new cars anymore. And if we do end up making the move to Panama, we’ll probably end up just going down to one car since neither of us would be working anymore.

Other expenses

Other expenses

Every household is different, so you’ll need to figure out some of the other expenses that can be cut. Maybe that’s cutting the cord to cable or maybe it’s just to stop buying the latest cell phone or computer.

Or do you take a lot of vacations? Maybe it’s not a matter of cutting out the vacations, but figuring out ways to spend less on the trip.

Do you go out to lunch at work every day or dine out for dinner all the time? Do you spend way too many mornings buying a Caramel Locko Mocko Whobee Doobie Spicey Picey Latte at Starbucks?

I don’t know what you need to cut out or cut back on to reduce your expenses, but you should open your eyes and pay attention to figure out what those irrelevant areas are in your life.

Remember, it’s all about the expenses…

I make a nice salary – nothing too far-fetched, but a good salary. Mrs. R2R, on the other hand, does not. She works part-time at a non-profit and if she didn’t enjoy what she does, her pay would make most people cry.

However, between our modest living and even raising a daughter, we are still putting away around 35% of our income. It’s definitely possible and many people are able to put a much greater percentage away.

Income doesn’t matter if you’re making a million a year but spending it all. Figure out your expenses and then you can figure out what you need to live off of. Take the remainder of the money and start saving and/or investing it.

Come up with a solid plan and financial freedom will be here before you know it!

Do you feel focusing on your expenses is a good way to get reach financial independence? What are you doing to make that dream more of a reality?

Thanks for reading!!

— Jim

Great post, Jim! Expenses make the world of difference and I wish more folks understood that. We live a pretty frugal life but there are areas we could cut back more on ourselves. We could get by in a smaller house, but we bought big as we knew we’d be starting a family and didn’t want to end up being to crammed for space five years later. We also own two cars but mostly only drive one.

But we do pretty good and combine that with two decent incomes and we’re able to save a lot each year! That’s the benefit of low expenses!

That’s definitely the benefit of low expenses! 🙂 Sounds like your family is in a pretty similar situation to us and that’s a good thing – living a pretty frugal life and saving a lot. Let’s hit our FI numbers and call it a day!

— Jim

Excellent analysis and conclusion. This is exactly the line of thought that I’ve been having the last couple of months. Now that we’re free of everything except the mortgage, FI has become more of a possibility. However, there’s no way we could make it last with our current expense level. Next year we’ll be working to save more and spend less.

Thanks, Chuck – appreciate the kind words! That’s exciting that you’re moving on the right track for FI. You’re definitely right that cutting expenses is the right way to go about it! 🙂

— Jim

This is definitely one of the biggest things I learned once I started getting into personal finance – that it’s expenses that matter, not income. The big publications base their retirement calculations on income because it’s just an easier number to see. Not a lot of us know our expenses. Plus, those publications are aiming for the lowest common denominator, so they just need to dumb it down to the simplest way possible.

Housing and cars are definitely the two big expenses that most people underestimate. If you can keep that in check, you’re really in great shape.

The media does seem to dumb everything down and, unfortunately, that sometimes gives people the wrong idea of what they need to do to get their finances on the right track. The good news is that the FIRE community is there to get people who really care and want to come out ahead on the right track.

— Jim

While raising your income is helpful in the equation, your right it’s all about the expenses ultimately. Put another way many people have highly variable pay. If my pay goes up or down in a given year do I require more or less to live on? The answer obviously is your income has no relation to your expenditures unless you let it. So why would you use it to measure your ability to live off that income in the long run?

Thanks, FTF – that’s a great point on your expenses staying the same regardless of if your pay goes up or down. There are a ton of workers in sales for instance that have dramatic swings in their pay and their focus should definitely be on their expenses versus income.

— Jim

Nice one Jim! I think you nailed it. Controlling your expenses has everything to do with how soon you (or if) you can retire.

I totally agree — it’s not what you make…it’s what you keep!

Thanks, Mr. Tako! 🙂

— Jim

I also dislike those articles that try to generalize how much you should have saved up at a certain age or income level. Because they’re written for a “general” audience they end up being written in a way that’s not useful to anyone. Particularly lawyers and doctors can’t fit themselves into those neat little boxes because many of them are just getting started in their career at age 30 and with several hundred thousand dollars of debt.

Haha, I’m with you on that – those articles suck as well! 🙂

You know it’s funny because a lot of people like myself that aren’t in those high-paying professions like lawyers and doctors always think about how much income you guys bring in but forget that you also go into it with ridiculous amounts of debt as well.

— Jim

Is that right? It’s hard to forget about the debt when it’s generating $1500 in interest alone. That’s not a made up number. Thanks to the government fixing interest rates, I graduated law school in 2009 with loans ranging from 6.8% to 8.5% with no opportunity to refinance them (places like SoFi, Earnest, etc. didn’t exist). So I had to clear a $1500 payment each month BEFORE I even started to ding the principal.

But I was one of the lucky ones. The real tragedy is the doctors and lawyers (but mainly lawyers) that end up with all the debt but without the high salary, which is made worse in that it’s not a reflection on their abilities but instead is a problem with oversaturation of the legal market.

That’s an insane amount of interest!! I have read some of the stories of people leaving law school and then not making a good salary – that’s like the mark of financial death.

Hopefully, I didn’t offend you – I definitely get it – I just meant that to guys or gals that haven’t gone through all that schooling for those professions like you did initially forget the cost you had of getting to where you are. I make a really nice salary, but I still look at guys in your position and think “wow, that kind of money would be great” because my first thought isn’t the loans (or the time invested for that matter!). Definite props to you for sure! 🙂

— Jim

Haha, no – definitely not offended. I was trying to make a joke about how it’s hard to forget you’ve taken on this fire breathing monster of a debt when it’s literally trying to kill you every month.

-Josh

Good – last thing I want to do is get on the bad side of a lawyer! 🙂

— Jim

Great post, and you’re absolutely right.

One of the biggest hurdles to figuring retirement off your expenses is that it requires figuring out how much you spend. A lot if people are unwilling to acknowledge their expenses because 1. they don’t want to put the time/effort into the tracking, and 2. they fear that they might have to cut back in their spending.

Too bad though, because those figuring off income might be in for a surprise.

I think you nailed it with why they don’t want to figure out their expenses. Unfortunately, that’s not going to end up being a good surprise for most people!

— Jim

Great analysis. Out of the wealth generating equation (income – expenses) it is often easier to cut unnecessary expenses than it is simply to generate more income.

I guess that’s why we see so many company do layoffs in downturns than actually try to generate more sales.

Thanks, Andrew – I didn’t about it being easier to cut expenses. I would agree with that being the smart move for most people, although some people do seem to have the knack for creating more income like it’s nobody’s business. 🙂

— Jim

So many people tell me, I can’t save money because I have so many expenses and there is just nothing left after paying for them.

The next time someone tells me this, I am going to point them to this article. Thanks for writing it!

Thanks T – appreciate the kind words! It’s interesting to step back and see people who complain about money but don’t want to cut back on any unnecessary expenses.

— Jim