Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

So here’s something unexpected… I just became a 401(k) millionaire last week.

As an early retiree, I had rolled over my 401(k) into a traditional IRA in March 2019. So on a technicality, I’m really a rollover IRA millionaire, but it’s still my 401(k) account sitting there with nothing new added to it since January 2019.

I had even pulled a little over $60,000 out of the account in December 2019. That was part of the Roth IRA conversion ladder I’m doing so we can access our retirement funds early.

Other than that, this account has just continued to grow alongside the market. And with it, I became a 401(k) millionaire last week.

Let’s talk a little bit more about how this happened and why it’s possible for you to do the same.

As a reminder, I’m not a financial advisor so please don’t make adjustments to your investments based on what I discuss. Talk to a professional to ensure you’re making the best decisions for your specific situation.

The path to $1 million and beyond…

Going from $0 to $1 million in a 401(k) isn’t something that happens overnight regardless of where you work. In my case though, I did something that isn’t as common as it used to be… I stayed at the same employer for almost 20 years. My 401(k) was built up solely from working at the same place.

When I first started working at the company in 1999, I was about $30k in consumer debt (credit cards). That doesn’t count the school loans or car loan I had either.

The good thing is that I was still living at home with my parents at the time. I wasn’t very bright financially back then but I still made the right decision to start contributing to the 401(k) plan I was offered. It wasn’t much at the time but I was at least contributing.

Of course, like most people, I had no idea what I was doing and just picked some random “yeah, these look good” funds in the plan. It wasn’t until later that I learned that they were funds with ridiculous fees (expense ratios) hidden in them.

But at least I was doing something.

And over the years, I slowly started increasing my contributions. Between that steady trickle along with the company match offered, the pot at the end of the rainbow started to grow.

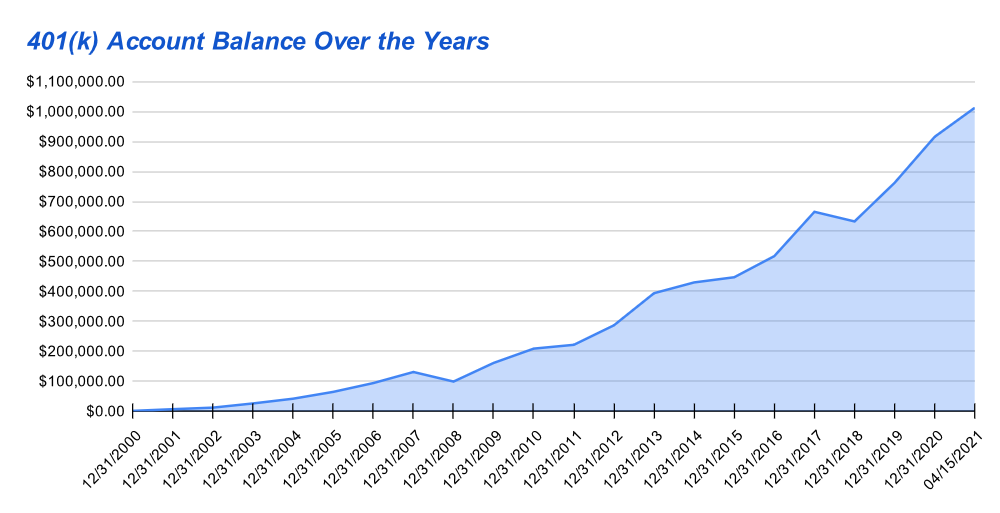

I had to install an old copy of Quicken just to grab some of the old historical data (I’m all in on Empower (formerly Personal Capital) now!), but here’s what it’s looked like over time…

Now, I’m not going to say that I didn’t have a little luck on my side. I began investing shortly after the dot-com bubble burst. In other words, I started buying in at the bottom of the market. That isn’t something anyone knew at the time, but it definitely helped me get where I needed to be.

That said, it’s important to note that I also didn’t panic when the 2008 crash happened. I just stayed the course and continued contributing money. I knew one guy who likely had a much larger portfolio than I did. But he panicked and sold everything he had because it freaked him out so much. He sold his entire portfolio at the bottom of the market and has kept everything in cash ever since. So he’s also missed out tremendously on growth over this past decade.

What does a 401(k) millionaire keep in his account?

Great question and the answer is that I keep much better holdings in it now than I did at the start.

When I first started with my 401(k), I was offered several funds to choose from and of course, I had no clue which ones to pick. I randomly chose mutual funds based on what I thought seemed logical. I took it a step further and actually looked at the past performance, but as we all know past performance is not indicative of future results.

If this sounds familiar, that’s because although 401(k) plans in the U.S. are well-intentioned (sort of), the system’s not designed well. Asking people who know nothing about investing to choose their investments is a terrible idea.

Wall Street is out to screw you over and drain you for every penny they can. Between high expense ratios that are generally well-hidden when possible and dropping and creating funds to hide bad past performance, novice investors are almost always positioned to just give away their money to the investment firms.

Just to give you an idea, some of the choices I was invested in funds included:

- MFS International Growth Fund-A

- MFS Corporate Bond A

- MFS Mid Cap Value Fund-A

- MFS New Discovery Fund-A

- MFS Aggressive Growth Alloc-Fd-A

- Dreyfus Basic S&P 500 Index Fd-A

Except for the Dreyfus index fund, I’m not proud of any of these other investments. Hell, I can’t even tell you much about them except I’m sure they enjoyed taking my money while they made random guesses on what would perform well in the market (can you tell I’m slightly bitter?!).

We’re now in a day and age where things have gotten a little better. Mutual fund companies are supposed to disclose their expense ratios more readily and there are more index fund offerings out there. However, we’re far from where we need to be.

Regardless, for the most part, I just left my investments be. It wasn’t until later that I realized that these companies were out to suck your hard-earned money out in the way of hidden fees.

I’ll talk more about that later in this post, but know that once I figured this out, I made a big change to my investments. In 2016, I moved everything in my account ($443,788.55) to be invested in the Vanguard Target Retirement 2055 Fund (VFFVX).

This was one of the only low-cost offerings to us in our plan (0.18% expense ratio at the time and now down to 0.15%). It was also the only target retirement fund we could choose from regardless of the date we planned to retire. Still, it was better than the other options.

A couple of months before I retired at the end of 2018, the company I worked for switched providers to Empower (who coincidentally now owns Empower (formerly Personal Capital)). Our investment choices changed and I moved everything I had in my account ($632,998.75) to American Funds 2055 Target Date Retirement Fund (AAMTX).

Finally, I retired at the end of 2018 and wasn’t a 401(k) millionaire yet… I wasn’t even close. But I was ecstatic to be able to move my money over to a traditional IRA where I could freely choose what to invest in. So that’s exactly what I did.

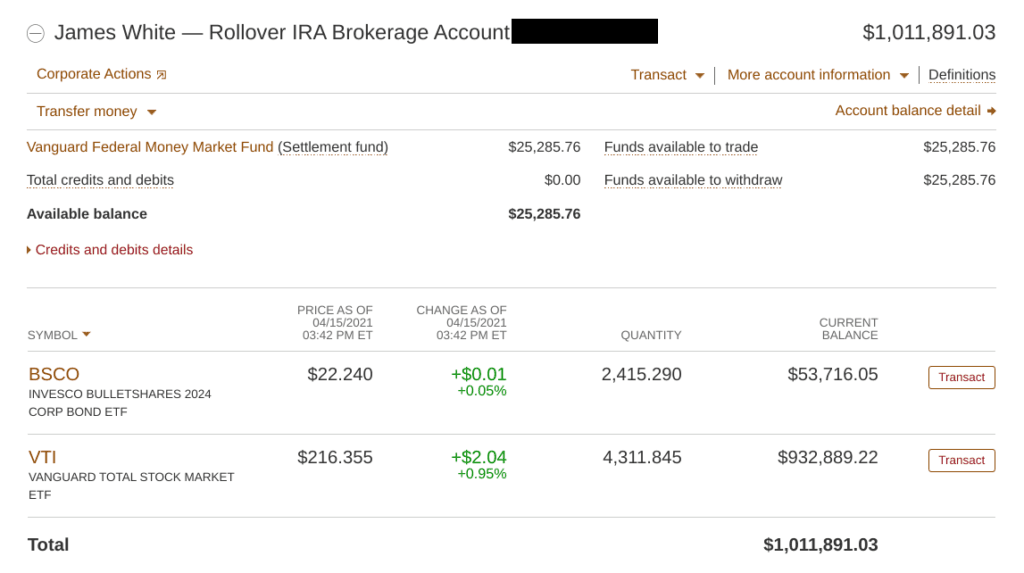

I rolled over $691,298.37 from Empower to Vanguard in February 2019. And here are my holdings as you see them today:

Remember that this is now just a part of our entire financial picture. As such, that’s why you see a year’s worth of our living expenses in BulletShares. The other BulletShares investments we have in our “Bucket 1” are in other investment accounts. I discussed more of this in detail in my post “The Drawdown on Investments – Our Game Plan” a couple of years ago. And the $25k in cash is part of what I’ll be using to buy VGSLX as I talked about in my last post, “Investment Portfolio Changes I’m Making!”

So there you have it. Because the stock market has been on an insane roll for so long, it’s helped the account take off without a doubt. The balance has grown over $375,000 since I retired without me adding another dime into it. That’s almost a 60% increase and doesn’t even account for the $60k I pulled from the account in 2019 as part of the Roth IRA conversion ladder that we’re doing.

How to become a 401(k) millionaire

I can’t guarantee you’ll become a 401(k) millionaire, but I do hope that this has inspired you to at least make that a goal. I’m excited to tell you that it’s possible even if you’re not bringing home doctor or lawyer paychecks.

So what do you need to do?

Save more… and the sooner the better!

Look, this should be the biggest gimme. If you want to become a 401(k) millionaire, you’ll need to sock away more money to make it happen. Putting 1% of each paycheck into the plan isn’t going to cut it.

I’m not saying that you need to max it out to the federal limit right off the rip ($19,500 for 2021), but you’re going to need to start pushing your contributions up.

My suggestion is to start with contributing the most you can afford (until you feel a pinch). But then look for opportunities to push that up even more.

If you get a 3% raise at work, raise your contribution by 2%, and then enjoy that extra 1% raise to spend on yourself… you get the best of both worlds! If you have a nice-sized bonus coming, talk to human resources and see if you can do a one-time contribution of half of it to your 401(k).

Two cool things to keep in mind:

- The earlier you contribute each dollar, the more time it has for compound interest to do its magic. Sure it’s great to think that you’ll contribute more down the line, but consider finding some ways to cut back on some things today so you can contribute a little extra sooner than later. You likely won’t miss it and you’ll appreciate it down the road!

- Be aware that contributions to traditional 401(k) plans are using pre-tax dollars (this doesn’t apply to Roth 401(k) plans). And this is something cool that took me a while to realize. Because taxes are taken out of your check based on the total after your 401(k) contribution, the more you contribute, the less you pay in taxes on that check. Because of that, it’s possible to contribute more and have your take-home pay be close to what it was before you upped your contributions. Try it out using a 401(k) calculator like this one or this one.

A future 401(k) millionaire loves the free $$$$!!!

If your employer offers you some type of match, I forbid you to not take advantage of it. Is that too strong? It shouldn’t be because it’s something you’ll regret later in life if you don’t.

When I was young, I thought it was nice that my employer offered a match on our 401(k) contributions… but I didn’t get just how valuable it truly is.

If we go back a step to the saving more idea, think about how valuable this match can be. Your employer is offering you free leverage to help you boost your 401(k) balance. Remember how compound interest needs time to do its thing? Now think about how much faster you can get there with someone else helping contribute.

My employer offered a unique match. Some of this was lumped under profit-sharing, but the overall gist was that we received 35 cents on every dollar contributed to our 401(k) plan. There was no limit on that match except for the federal max.

Take a step back and think about this. I was getting $35 of free money on every $100 I invested in my 401(k). That’s a 35% return before any stock market growth!

I’d be a fool to pass that up… and I was for several years. In my post, “How I Got Over $181,000 of Free Money for Retirement”, I talked about how it looks like I started maxing out my 401(k) somewhere between 2006 and 2008. I kept that up until I retired at the end of 2019.

But that’s still 7-9 years of not maxing the plan out. And because my employer was matching up to the federal max, I had too many years where I was missing out on free money.

As a former manager at the company, I can tell you that most of the employees were passing up some or all of that free money being offered… not good.

Becoming a 401(k) millionaire doesn’t mean you need to do it yourself. If your employer is offering you a match, you should be contributing at least everything you can to get every penny available to you. Find out what the max is that you can get a match on and set your sights on that target. Do what you need to do to make that happen.

The fees can eat you alive if you don’t pay attention

For years, I gave up way too much money to these companies due to my naivety of things. The fees they charge come out almost invisibly to you, so as long as your account continues to grow, you don’t think much about it.

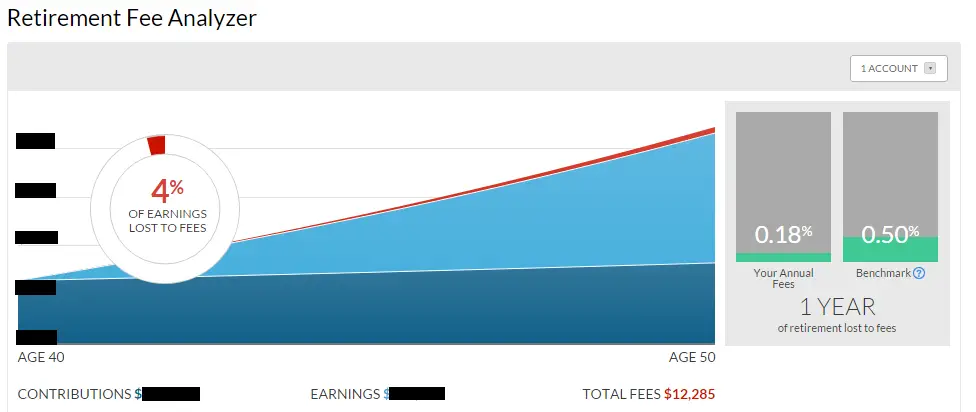

However, I started using Empower (formerly Personal Capital) as some free software several years ago to get a better handle on my investments. It lets you securely link all your accounts (banking, credit cards, investment accounts, etc.) and it’s nice to be able to see everything in one place. This is something I also had with Quicken, but Empower (formerly Personal Capital) has a few other tricks up its sleeve.

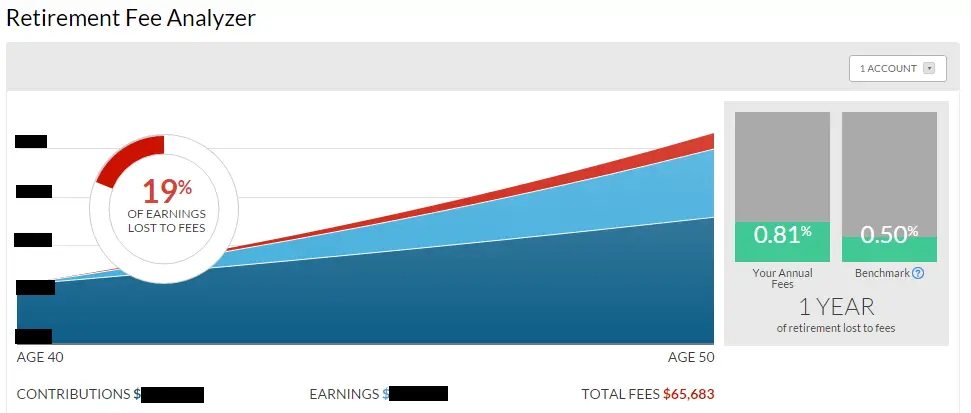

One of those tricks is that it can see what fees you’re paying in your 401(k) account much easier than you can. I learned that the fees I was paying would amount to over $65,000 over just 10 years!

That got me going and I did a lot of digging around and I then easily changed my investments to ones with lower fees. After re-running the analyzer, I was now projected to pay just over $12,000 in fees over 10 years.

That’s more than a $50,000 savings just because some free software showed me what was really going on! If you’re not using Empower (formerly Personal Capital) to track your investments, it could be costing you big money!

Don’t ever cash out your 401(k) if/when you leave a job

I became a 401(k) millionaire through almost 20 years of employment through the same employer. However, this wasn’t my first 401(k) plan.

I was introduced to 401(k) plans when I worked at Walmart back in the mid-’90s. I’ll be honest – I didn’t contribute much back then (poor college student!). And then I made the biggest mistake you can do with a 401(k)… I cashed it out when I left.

That’s right – I was so desperate for cash that I withdrew everything I had in it. It sounded like a good idea at the time, but after having to pay taxes and a 10% penalty on it, was it really worth it? Probably not.

Looking back, I’m sure I could have cut back on expenses or borrowed a little money to make things work. But I didn’t realize what a big deal this was – not only did I get crushed from cashing it out, but I also missed out on a valuable opportunity for the magic of compound interest to grow this account at such a young age.

Such is life and obviously, things turned out fine for us financially, but that likely cost us time getting to where we are today. Don’t make the mistake I did – if you leave a job, let those 401(k) accounts continue to grow. Roll them over into an IRA and invest wisely – years from now you’ll be glad you did.

As if that mistake is embarrassing enough, what I’m about to do might even be worse! I’m sharing a regional commercial I did for Walmart back in the day…

You’re welcome.

Will I stay a 401(k) millionaire over the long run? Who knows? The market’s been crazy hot lately… too hot? Time will tell. Maybe this fun point in time will already be over by the time you read this.

In the meantime, I was just excited to reach such a cool milestone… and I’ve got the screenshots to prove it! 🙂

Plan well, take action, and live your best life!

Thanks for reading!!

— Jim

Hi Jimmy,

I forgot about the Walmart commercial. LOL. You did a good job. Did you get paid extra for it?

Between that and our episode on House Hunters International, maybe it’s time for some big acting gigs! 🙂

I’m almost positive I didn’t get paid for the commercial. That was so long ago though, I can’t remember for sure.

Good post, Jim. Fees are definitely worth paying attention to. Especially since the experts do not even beat market average consistently. If I’m going to live on a 4% withdrawal, giving up an extra 1% in fees is a large hit. I’d offer (or emphasize) 2 additional simple ideas for those starting the 401k path. The first is you are young – the money won’t even be accessed for 30 years, and won’t all be used up for another 30 (knock on wood). So be aggressive. Buy stocks – avoid stable value funds. You have time to recover from a 2 or 3 year bad market. By riding out 2008-2009 you got a lot of stuff on sale.

The second is to not fear current taxes – if you can take advantage of Roth 401k early in career, do so. The tax man eventually comes anyway, and you’ll need the deductability of a regular 401k later – to avoid stepping over tax phaseouts or higher marginal rates. For example, income under $150k keeps a couple on the current tax windfall train. Using a regular 401k might keep a couple under that threshold. But the Roth is one and done if you are in the middle of a tax bracket…

I like those ideas, Kev! For younger folks, being aggressive and pushing everything they can into stocks is almost always going to be the smartest move. I agree with the Roth IRA as well. They never had that at my company while I was there, but I would have switched to that if they did. You also get the best of both worlds because the matches go into the tax-deferred pile. The extra bonus with Roth 401(k) money is that what you see is what you got. With a traditional 401(k), you do have to remember that the tax man will cometh at some point and likely take a nice piece of that balance.

“And electronics!”.

OMG, that Walmart ad is HILARIOUS! You can afford to laugh now, you’re a 401(k) millionaire!!

Fritz, if you need an autograph, you’ve earned it with the help you’ve given me on my portfolio… just let me know who to make it out to! 😉

I’ll take one of those autographs!!!! lol….

Best thing I’ve seen all year 🙂

When I was younger, I used to have a t-shirt that said “No autographs, please!” I need to get one of those again because this celebrity status is becoming too tough to manage! 😂

Well Jim, if the bust ever knocks you off your millionaire pedestal, at least you’ve got your acting chops to fall back on!

Thanks for the tip about the fee analyzer, wasn’t aware of it and will check it out for myself today.

Congrats on hitting this milestone!

TFT

It’s tough being a celebrity, TFT, but I do what I can! 😉

Yes, you definitely should check out the Fee Analyzer on Personal Capital. Being able to see what’s really going on can make all the difference.

Congrats! As I was reviewing my asset allocation and reducing risk in equities, I realized I could’ve been a 401(k) Millionaire as well. Sadly, I am not and my solo 401(k) balance is only about $240,000.

Although I do have a decent rollover IRA, it is not technically the same as a 401(k)! Therefore, I may have to delay the retirement life after all.

Got to keep grinding!

Sam

Thanks, Sam – I had my post all outlined and was working on it and then I saw yours (Could Have Been A 401K Millionaire By 40 Had I Kept My Job)! You beat me to the punch, but we had some different angles for sure. Regardless, we both came to the same conclusion that it’s absolutely possible for folks to become a 401(k) millionaire if they make it a priority.

Good stuff – congrats on achieving 401K millionaire status! I was interested in your thoughts on Invesco BulletShares bond ETFs – how have they performed for you? How accurate is the Invesco BulletShares net acquisition yield calculator relative to reality? In this low interest rate environment, I have been thinking that the BulletShares may be a viable option for some yield if hold to maturity. I was thinking about the high yield corporate BulletShares while keeping duration short (2023 and 2024). Any thoughts / recommendations would be welcome!

Scott, this might surprise you but I actually don’t closely track my portfolio performance I just invest according to my game plan and stay the course (though I’ll periodically adjust as needed). In the case of the BulletShares, these fit the bill as a safer haven for my upcoming living expenses than the volatility of equities could provide so that’s why I keep a 4-5 year ladder of them. You’ll probably want to check out the prospectus and performance on the Invesco website to see if they’ll work for your situation as well.

LOL!

Love the commercial!

I did a TV interview for one of the local TV stations back when I worked for Builder’s Square.

Thank God it only aired twice!

😀

I’m far too ignorant of the ins and outs of the market to risk it. So far, the investment in the rentals has been treating me well. (knock on wood).

Oh boy, I need to get my hands on that interview, Rich – did you have the same “sass” then as you do today? 😂

You’ve done awesome on the rentals over the years for sure, Rich! With your empire, no need to worry about getting into nuances of something like REITs when you’ve already perfected a system.

I’m totally getting your autograph next time we meet! Are you in the screen actors guild?

Haha, that’s true – I need to get a SAG card!

Congratulations! Nice job.

You started later than I did and became a 401k earlier.

I made some mistakes early on. It took me a while to figure out how to invest.

Hopefully, I’ll catch up to you soon.

Well, you definitely have my portfolio beat as a whole… I’ll accept this one win graciously! 😉

Those fund choices from your 401k early days remind me of some of my early 401k investments. I remember picking things (seemingly) at random but I must have thought I had a brilliant strategy back then. My employer eventually switched 401k providers and we got better fund options to choose from which was good. The important thing is that you started saving early, which is probably even more important than what you invested in. Congratulations on the millionaire status!

It’s silly how they used to have such bad choices. I’m going with “used to” because I’m hoping that’s not common anymore. But you’re right – saving early was the key regardless! 🙂

Congratulations on making the $1 million mark. Nice post too.

Thanks, DP – much appreciated!

Not quite as impressive as the Dogecoin millionaires, but still a great milestone (with the added benefit that you are still a 401k millionaire unlike the Doge fortunes that have been lost already!). And I gotta say, the only thing embarrassing about that Walmart commercial is that it didn’t lead to bigger roles. That was pretty good!

Haha, great points on both counts! I’ll stick with my million dollar’s worth of index funds over crypto any day. I might miss out on some speculative wins but I’d rather wait until it becomes (if it becomes) a solid investment tied to something other than just other investors speculating as well.

Now for the next step, converting the 401K from $1m to something that can slowly be spent now, rollover time!

But well done, that’s impressive to get to the $1m mark! and that 35% match is amazing! I wonder if the company would’ve reduced it if anyone actually took it up?

Already working on the Roth IRA conversion ladder but with the exception of the $60k I pulled from this account so far, everything’s been from Lisa’s rolled over 401(k) thus far. Slowly but surely to minimize the taxes!

There were a handful of people I’m aware of that actually maxed out their 401(k) plans there year after year (myself included). My employer was very generous in offering that for a company of only about 40 people. Would he have set a cap if more people did it? Possibly, but unfortunately, I don’t think that’s something that would become a norm anytime soon.

Congrats Jim! That’s an impressive sum!

Thanks, Mr. Tako… slow and steady wins the race over time it seems.

How come your About page doesn’t have the fact that you were a celebrity from Walmart?!! Just kidding.

It’s amazing how easy it is to become a 401k millionaire. Max it out every year, put it in the S&P 500, and BOOM! 401k millionaire. No tricks of any kind, just plain old buy and hold.

The number of posts talking about 401k millionaires is making me really question whether I shouldn’t look into early retirement.. It’s quite difficult to give up a 7 figure balance, no matter how bad my job is at times..

Very true, David – but who knows when the market’s going to shift. That pile of money could be worth a lot less in a short amount of time.

I hear you about pulling the trigger – giving up a nice income is a tough thing to do!

This may be a little off the subject, but can you track some of this information in Mint? When doing taxes, how do you run a category report, such as how much you spent on dining out?

I found you one day on a Firefox link, by the way. I have been reading faithfully every week. I love what you write.

Thank you, Jim!

Thanks, Tim – glad to have you as a regular reader! I actually now use a combination of both Mint and Personal Capital. I would probably be using only Personal Capital but tracking manual cash transactions is something that Mint is much better at and that’s become a fair amount of our spending here in Panama. So now when I look at our category spending (which I don’t do heavily), I refer to Mint. Once we move back to the U.S. next May though, the cash spending will probably be pretty negligible and I might go back to trying to use Personal Capital by itself again.

Congrats on reaching that milestone! Sadly my 401(k) is no where near $1 million! That said, like you, in the past I made mistakes by either not contributing, or taking advantage of matching, etc. There was also one job I had where the employer matched in company stock, with a heavy vesting schedule, and then went bankrupt. I suppose that also left a bad taste in my mouth. Luckily that was back in 2007-2008, and I have learned a few lessons since then! 😉 These days my current employer offers 8% and I have been taking full advantage since day 1 which is definitely contributing to the path to FI! I also like your point about bonuses – Not only will some employers allow you to contribute some of your bonus toward your 401(k) but it may also be the case that they apply the matching percentage to it as well. It always pays to ask, as I find things like that aren’t always advertised..

No doubt we’ve all made some mistakes with our finances and investing. The key is realizing it was a mistake and then taking the actions to change it. Looks like you’ve done exactly that with your 401(k) with your current employer. Nice work and hopefully you’ll be writing a similar post about your million-dollar account one day! 🙂