Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

It’s time to make some changes to my investment portfolio!

I wrote a post last month called We Have a Lot of Cash in Hand Now… Too Much! that discussed how too much of our portfolio is sitting in cash. Apparently, that’s not uncommon right now as I received a lot of feedback in the comments and replies back from my mailing list (which I recommend you sign up for on the sidebar!).

So I decided to write a post to discuss the changes I’ve decided to make to get things straightened up over here.

Some of this might help you in thinking your way through any extra cash your sitting on. But as always…

Remember that I’m not a financial advisor. Any changes you make to your investment portfolio are at your own risk. Contact a professional to help you make the right decisions for your investments.

My problem… too much cash?

Just to bring you back a little to my post last month, the biggest problem I have in our investment portfolio is too much cash.

That feels weird to even say – is too much money a bad thing? It is when you know that over time it can easily be eroded to nothing by inflation! And with interest rates likely rising over time, long-term bonds don’t feel like the smart bet as a place to shift our extra cash.

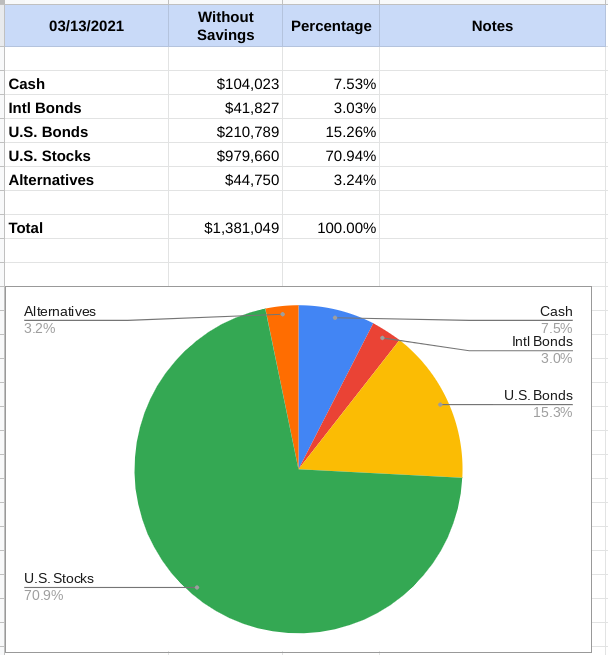

Here’s the chart I shared from Empower (formerly Personal Capital) in that post showing my asset allocation in my investment portfolio…

I love Empower (formerly Personal Capital) and use it religiously to help manage my investments. If you aren’t already using it, you can create a free account for Empower (formerly Personal Capital) here.

But there’s one thing I noticed in the chart that was throwing me off a little. The numbers you see are only from my investment accounts – they don’t include information from my other linked accounts such as my bank accounts. That can skew the information presented if you’re not keeping that in mind. A perfect example of this is the cash we had from selling our duplex a few months ago – when all was said and done, that’s about $86,000 that wasn’t counted at all!

I don’t think it’s a bug because Empower (formerly Personal Capital) is showing you your asset allocation for your investment portfolio, which I would imagine is their primary focus here. It would be nice though if it included all the cash in your bank accounts and possibly subtracted out any short-term debt like credit cards as well. Otherwise, you’re not getting the full picture.

And we need that full picture, so we’ll get to what that looks like in a little bit.

Discussing my investment portfolio with Fritz

Fritz who? What the what?! Fritz is the brains behind The Retirement Manifesto and he’s one smart guy. Lucky for me, we met and became good friends at a FinCon convention in 2017. It’s good to have smart friends!

I reached out to him to see if I could bounce some ideas off him about making some changes to my portfolio. He was nice enough to agree and it was good to talk to him and also get some good feedback on my investments.

And again, bear in mind, Fritz’s opinions are strictly that – his thoughts on my specific investment portfolio. Please don’t take any of this information and try to run with it without understanding the ramifications. Talk to a professional before making any big changes you don’t understand.

Here a small recap of some of what we discussed…

Asset allocation

The first suggestion was to update my asset allocation chart to include all cash. As I mentioned, seeing the full picture is critical in making smart decisions. From there, it’s important to determine where I want my investment portfolio to be as far as asset allocation goes. That’s going to be unique for each of us.

Fritz mentioned that he feels that in today’s times, sitting on less than 10% cash is not that big of a deal. Even 15% isn’t necessarily the end of the world. That cash can be fantastic to be able to jump on opportunities when they creep up. A great example is that both Fritz and I made out like bandits when the market took a dive last March. I simply did a rebalancing of my portfolio and brought my desired allocation back to where it needed to be. That worked out excellent for me!

Fritz likes to have about 10% in alternative investments (i.e. real estate, precious metals, P2P lending, etc.). These not only provide a hedge against the stock market, but they can help protect against inflation. He talks about his thoughts on this subject in his post Investment Options To Protect Against Inflation.

Inflation and the Bucket Strategy

Speaking of inflation, that’s a big point of this post. My goal with this cash isn’t necessarily to make a fortune off of it (though that wouldn’t hurt!) but to simply earn at least enough on it to protect against inflation without posing the risk you inherently have when invested in stocks.

I’m comfortable with having 70% invested in stocks. I’m only 45 and need our investment portfolio to carry us for quite a long time. That means we need growth out of our investments. But I don’t feel comfortable going all-in and need a little balance on this ride.

That’s where other concepts come into play such as having a bucket strategy with some cash or other low-risk investments on hand. Fritz discusses the bucket strategy in his post How to Build A Retirement Paycheck From Your Investments and why this can be very helpful in retirement planning. I talk about our strategy here in The Breakdown of Our Net Worth Savings & Investments and The Drawdown on Investments – Our Game Plan.

So the plan and foundation are there – now I just need to re-align to get our investment portfolio back in check.

Some ideas

Fritz and I brainstormed quite a bit – it’s hard to organize and put everything down in this post, but I’ll give you some of the ideas we talked about…

REITs

He liked my thought of putting more money into REITs. With the duplex, I had a nice hedge against the stock market. Now that I sold that, I lose that hedge but REITs can give a lot of that back. They also help build up my alternative investment allocation a little more. We talked about investing anything from the $86k I have from the sale of the duplex up to maybe $120k in REIT funds.

Precious metals

He’s a fan of precious metal ETFs as well. One idea was to take a small amount ($20k or so) and invest it accordingly. This just serves as another asset class to have in our investment portfolio.

Short-term bond funds

I’ve mentioned that I’m not as versed in bonds as I should be. My understanding was that you invest in bonds and if the interest rate climbs, you’re going to be in for a little hurt. After talking to Fritz more though, I now understand that there’s a difference between short-term and long-term bonds.

Because we shouldn’t have much fluctuation in interest rates over the short-term, short-term bond funds can still be a smart move for an investment portfolio. In our case, we’d be looking at Vanguard Short-Term Investment-Grade Fund Investor Shares (VFSTX).

TIPS

If we’re aiming to just keep up with inflation, Treasury Inflation-Protected Securities (TIPS) definitely fit that bill.

Treasury inflation-protected securities (TIPS) are a type of Treasury security issued by the U.S. government. TIPS are indexed to inflation in order to protect investors from a decline in the purchasing power of their money. As inflation rises, TIPS adjust in price to maintain its real value.

Investopedia – https://www.investopedia.com/terms/t/tips.asp

Fritz said that he’s a big fan of TIPS and buys some of these through the U.S. Treasury site every year.

Panamanian CDs

I also mentioned the thought of investing money in a Panamanian CD. The banks here in Boquete are offering around 3% for CDs – that’s a much bigger jump from the banks in the U.S. right now. If I did a one-year CD right now, we’d be able to pull the money out right before we leave next May.

There are some details that we’d want to take into consideration for this though. There is no FDIC insurance here, so if the bank folds, that could be problematic. And, if you put $10k or more in a foreign bank account, it becomes somewhat of a hassle because you need to report it to the IRS. We could do just under $10k, which would put less of our money at risk and we wouldn’t have to report anything.

Dollar-cost averaging

The other point we discussed was dollar-cost averaging. Instead of investing everything all at once, it might make sense to break it down and spread it out over a year or possibly even longer. The research states that you’re generally better off with lump-sum investing over dollar-cost averaging.

However, if the market crashes the day after you put in all your money, you’re not going to be a happy camper. Dollar-cost averaging is a little better for the psychological side of things.

The changes I’ve decided to make in my investment portfolio

I took Fritz’s advice about updating my asset allocation first and including the cash from my bank accounts. I did this using Google Sheets and created “before” and “after” sections in the spreadsheet.

The “before” section matches what I show in Empower (formerly Personal Capital)…

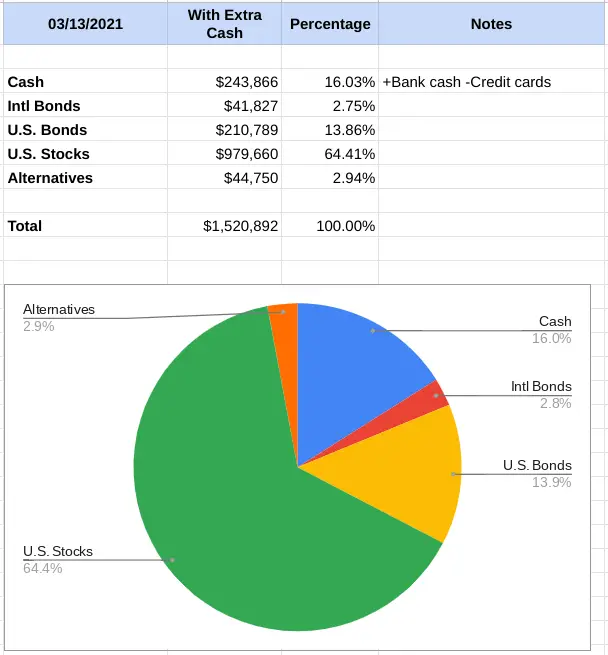

But then I created a new section to include where we stand in total on the cash front. I added in the money from our bank accounts and subtracted out what we currently owe on credit cards (we pay these off in full every month).

If you look at the difference between the two, you’ll see that what I have in cash is actually just over 16% of our net worth. Yikes – that’s a little too high for my liking!

But an interesting change to note is that my asset allocation really only holds 64.41% of stocks. My goal is to keep us at around 70% equities, which is where we were when I wasn’t including our cash in the bank. Wow, that’s @#$%^ a lot of “w’s” in that sentence… alliteration at its best!

Anyway, that means consequentially that I should be buying some more stock (Vanguard Total Stock Market ETF (VTI) in my case). And guess what – that little detail becomes the fundamental piece to everything else that’s about to follow. I’ll talk about that in a second, but first, there’s another important detail…

In my post, We Have a Lot of Cash in Hand Now… Too Much!, I mentioned something important. I talked about how I don’t want to have the REIT investments in my taxable account because it’s a less tax-efficient investment. Instead, I’d prefer to have that in one of our retirement accounts where we don’t have to worry about the taxes associated with the dividend payouts.

The problem is that I’m not working so I can’t put the money into any of our retirement accounts. So the way I planned to handle this was to fund my taxable account with the $86,000 from the sale of our duplex. I’d then buy $86k of VTI in that account with the money. Finally, I’d sell $86k of VTI in a retirement account and buy $86k of the REIT fund Vanguard Real Estate Index Fund Admiral Shares (VGSLX). By doing this, I’d essentially be just shifting where I owned the funds in my investment portfolio… make sense?

So here’s where things get a little funny and eerily simple. Remember how adding in all that cash we’re sitting on threw our asset allocation out of whack from where I want it to be?

Based on my total portfolio and the numbers I’ve shown you, I need $84,964.40 more in stock (VTI) to get the percentage back to my desired 70%. And I’m going to be injecting $86k into my taxable account from the sale of the duplex. BOOM, I can buy VTI right there and my stock allocation will be back on track.

So that leaves the REITs. The plan was to sell about $86k of VTI in my retirement accounts to buy the funds in those protected accounts. Would you believe though that I’m currently sitting on $82,094.42 in cash between my rollover IRA, my Roth IRA, and Lisa’s Roth IRA? That’s pretty darn close! If I buy up VGSLX with all that spare cash in the retirement accounts, I’m just about right where I need to be.

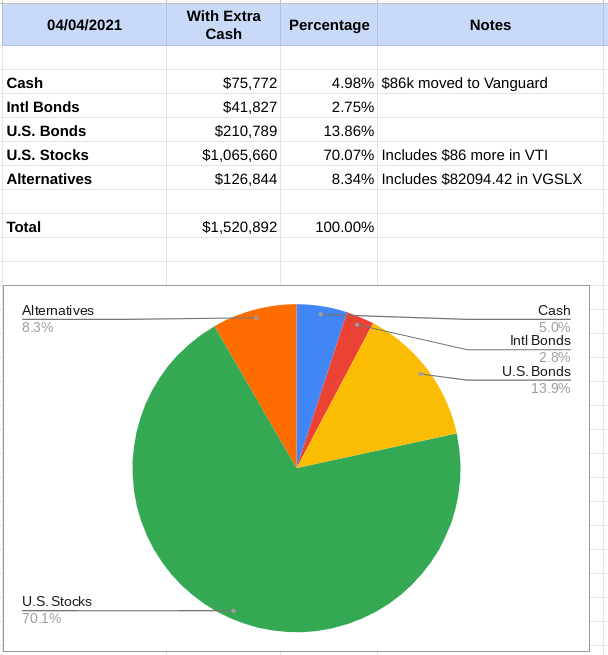

Look at my updated projection after making those few changes…

Our stock allocation will be at 70.07%… perfect! Because of the REIT fund purchase, our alternative investments will be a much more respectable 8.34%.

And finally, our cash on hand moves down to under 5% at a little over $75k. Don’t forget that the cash number includes our living expenses in the bank for this year so that brings down our “extra” cash to a little under $39k. That little bit of cash is good for emergencies, investment opportunities that creep up, etc.

Awesome!

As freaky as this is, everything just fell into place. By simply fixing our asset allocation to include our cash, we essentially only needed to make two strategic changes:

- Re-balance to get our stock allocation where I want it

- Take the proceeds from our duplex sale and buy the REIT fund, VGSLX

I’ll be dollar-cost-averaging these investments as well so it’ll take a while to get everything where it needs to be.

The downside is that a lot of the hour-long conversation Fritz and I had turned out to be irrelevant… for now. Because the numbers simply worked out, I don’t need to start investing in some of the other investments we discussed.

However, things change. For instance, if the market continues to climb and I end up rebalancing again to get my stock percentage back down, I’ll need a place in my investment portfolio for the cash I get from the stock sale. I’ll be referring back to this post myself if/when that happens!

And, on the upshot, Fritz and I got to have a nice video chat – it was great to talk to him again. It was also a good opportunity for me to learn some things and to get some reassurance on what I’m doing right. It’s always nice to get a second set of eyes on something as important as this.

Besides that, I do hope that if you’re in a similar position, this gives you a few ideas as well… team effort, my friends!

One last note – the numbers I based everything on are from 4/4. Things change – that’s how the stock market works. In fact, it’s gone up quite a bit as I wrap this up on 4/9.

So it’s probable that this plan with our investment portfolio isn’t going to work as seamlessly as it looks in this post. However, it should still be relatively close and I’ll make any adjustments as needed along the way.

Thanks for reading!! And muchas gracias for your help, Fritz! You can check out more of Fritz’s geniusness (I made that word up) at The Retirement Manifesto.

Plan well, take action, and live your best life!

— Jim

Thanks for the update Jim. I’ve maintained a similar asset allocation for over a decade using Alexander Green’s book the “Gone Fishin’ Portfolio”. It’s a good read if you get the chance. I did make the mistake of getting some of those alternative accounts in the taxable side but I quit investing in those now and turned off the dividend reinvestments.

On the dollar cost averaging crutch, just picture the market going down right after you make your last investment. You get the same psychological affect. I think the only way to go is lump sum and focus on asset allocation. Glad you are still enjoying Panama.

I’ve heard of that book before but haven’t checked it out. Funny enough, I went to add it to one of my reading lists and noticed that the latest edition just came out today… that seems like a pretty good sign that I should read it! 😉

Thanks for the update! That is a lot of cash actually.

It’s funny, but I am going the exact opposite route! I had about 85% of my net worth invested in risk assets. About 35% of my net worth was in stocks. I am selling stocks now to get it down to closer to 25% if the markets keep going. Just sold so it’s down to 32%.

Over the next 12 months, I plan to re-retire. Therefore, I want to have a more conservative net worth allocation that’s more appropriate for a regular 60+ year old retiree.

Sam

You’re in a great position to be much more conservative, Sam, so I think that makes a lot of sense in your case. With everything I’ve read of yours, you have multiple solid streams of income coming in. That seems to fall right in line with what William Bernstein, MD once said during an interview… “When you’ve won the game, why keep playing it?” Fantastic that you’re in that position where you scale back so much – nice job!

Hi Jim,

I look forward to your blog every week, as well as Brian Preston’s “The Money Guy”. It’s great that both you and Brian mentioned talking with Fritz in recent weeks. I won’t say I retain a lot from either Route to Retire or The Money Guy, but I am very much exposed to investment options and tracking finances. I will have to pay more attention to the details from you both for it to really sink in.

I currently have two houses as rental properties. I receive multiple requests to sell these houses every week , mostly without providing a dollar figure. I am considering selling one or both of these houses and using the money toward purchasing REITs. As a result, I am interested in hearing in the future how the performance of your REIT funds compare to your expected income from renting out your properties.

If you haven’t ever watched The Money Guy on youtube, you might want to check it out. Of course, it’s quite possible I learned about it through your site in a previous post.

Have you definitively decided to leave Panama in May, or are you considering extending your stay? How much, if at all, has Panama eased off on restrictions/requirements due to Covid? I trust we will hear more in future posts. Thanks for keeping your site both interesting and informative.

Thanks, Mike – I’m familiar with The Money Guy Show, but it’s not one of my regulars to listen to… maybe I’ll have to add that into the mix!

I would imagine that if your properties provide a nice cash flow that you’d come out ahead of the REITs, especially with the possible tax advantages. But if you’re not loving the landlord experience anymore, now’s definitely a smart time to consider jumping out. You’ll probably make less of a return but you’ll also have fewer headaches.

I think it’s pretty certain that we’ll be heading back to the States for the long haul next May. As much as I love it here, it seems to be the smart move for Faith (time will tell though!).

We do still have an 11pm-4am curfew, you have to wear masks in public, restaurants are still only open at 25%(?) capacity, and they take your temp and give you hand sanitizer when going into stores/restaurants. Those details are pretty minor to us and other than that, it’s almost completely back to normal here.

“Geniusness”? My spellchecker underlines that word…but I’m honored for the compliment.

It was nice chatting with you, Jim. Great to bounce ideas off each other, sounds like you have a solid (and simple) plan, just the way you like it! As I mentioned, part of our logic for buying our second home in Alabama was the fact that we, too, were carrying too much cash. A common problem, indeed. Tough to find a place to park $ in today’s low-interest (but rising) and highly valued stock market.

All that matters is that we now have a place to stay rent-free in Alabama… thanks, Fritz! 😉

I’m going to put $10k into I bonds when the rate changes. There is a fixed rate which will probably be 0% plus the inflation index which should be around 2% for the next 6 months (changes 2x per year). You can only put in so much per person/ per year (Basically $10k electronically). You have to keep the money in for at least a year. After a year you still have to give up 3 months interest but this is way better than current savings accounts. After 10 years there is no interest penalty. Just another safe money option.

I definitely need to spend some time learning more about how bonds work. Great information, Scott! If the stock market keeps growing and I end up having some additional cash from re-balancing, I might be following suit.

Strikingly similar to my cash position. Personal Capital shows it to be 7.1% but if I add in the cash we have in our various savings and checking accounts it is actually 11.4% of our total liquid assets. But I’m OK with that, even more OK since Fritz isn’t aghast, I agree he’s very geniousy. I just look at it as a form of bond that has a fixed and very low rate of decline that you can monitor, inflation. While regular bonds fluctuate with something you can’t predict and might not change slowly, interest rates. I’m also a fossil so I only have 55% of my total liquid investments in stocks. I’m going to sit tight. Last March I moved some of the cash on hand into the market. If I see another such opportunity I might do that again. Otherwise I just will consider the cash to be the bucket to fund me until I hit Social Security which is frighteningly not so far away.

He really is very geniousy, isn’t he?! 🙂

I like your plan to just make that your cash bucket until SS hits (unless an opportunity creeps up again). Great position to be in!

Congrats on the recent scale back to “full retirement”, by the way. Hope you’re loving it!

Most Panama banks now require $10,000 to open a CD. You only have to report to the IRS (form 8938) if you have over $400,000 in all your combined foreign bank accounts. You do have to report & pay USA tax on the interest earned.

You must file FBAR with the Dept of The Treasury if you have over $10,000 in foreign bank accounts. This is no big deal as it’s done electronically.

Before taking out a CD in Panama, be sure to ask what is the fee for transferring it to a USA bank account once it matures. Some say this fee is so high, it’s not worth the 3% interest earned. Panama doesn’t like people transferring money out of the country!

Thanks for the info again, Debbie! I would guess that I’d probably have to open a bank account here in order to take out a CD, so that’s even more of a hassle. I’m happy that things worked out pretty well and I don’t have to even go down that path. 🙂

I think these sound like the right moves for where you are. I am currently 100% in equities, but I haven’t pulled the trigger yet on retirement and probably won’t do so for 5 years (health insurance guaranteed in that time). Then I have to figure out to do a bit more readjusting of my portfolio. Your posts (and Fritz’s) help me plan for that. Love the blog Jim.

Thanks, Jason! I’d wish a down market for you to be buying more stock on sale, but that wouldn’t fare so well for little old me trying to ensure that we don’t get crushed by the sequence of returns risk! 😉

That’s great that you’re only 5 years aways from guaranteed health insurance! It’s ridiculous that in the US that health insurance costs can be the determining factor on when someone can retire in the US, but I guess that the way it goes for the time being. It’s an important factor I have some plans with when we get to the US but I still need to do some more research on it before we make it happen.

I’m pretty darn close to your exact asset allocation except I do have a decent chunk in a REIT index fund and I don’t have the int’l bonds. Besides that we’re similar, though I’m a bit older than you but still consider myself a child maturity-wise 🙂

Haha, I think you and I combined might have the maturity of a ten-year-old! 🙂

I think these changes make sense, especially considering that you’re retired but still want to take full advantage of the market.

Thanks, Bob – trying to squeeze out a little extra return without too much risk is a tough ball game right now. Time will tell if these turn out to be smart moves! 🙂

Changes make 100% sense. I am in the process of doing the same thing by selling VTI in my Retirement accounts and picking up REIT ETF.

I also am carrying quite a bit of cash, but I am using it as a sequence of return risk and that way I don’t have to worry too much about holding any bonds. I also can deploy some extra cash we have into a potential website purchase.

Thanks for this update. Any recommendations on Precious Metal ETFs from Fritz?

Hey, AR – seems like we’re on the same page! Check out Fritz’s post Investment Options To Protect Against Inflation where he hits on his thoughts on precious metals. He also links to a more in-depth post there as well.

Perfect thanks. I glossed over that post the first time around. Very useful1

Thanks for sharing. I’m less than a year from retiring early and this is the first time I’ve taken the pains to put all of this data together. My breakdown was 67% stocks, 20.5% bonds, 8.5% cash and 4% REITs/Real Estate Syndication deals when exclusing my home (since it’s not a liquid asset). When including my home, the breakdown comes out to 59.1% stocks, 18.1% bonds, 7.5% cash, 3.7% REITs and 11.7% for our (paid for) home. You really have me thinking about whether this is the right allocations for us…..so I appreciate it…

Here’s an early congrats on getting to your early retirement date… so exciting and liberating to be able to choose how your day will go each and every day! Best of luck with choosing the right allocation for you. Coming up with the right mix between comfort, security, growth, and risk varies from person to person. Even though I felt comfortable with our portfolio before pulling the trigger on leaving work, I talked to a fee-only fiduciary financial advisor and that reassurance (plus the other ideas) was well worth the cost. Not sure if that would be right for you as well, but still worth considering.

Good luck!!

If you move back to the US next May, will you be buying a house? In many parts of the US, home price inflation is outpacing stock market returns. I was wondering if it might be better to purchase a house now as opposed to waiting a year? Where I live in north Austin TX, real estate experts claim that the average home value increased $75,000 to $100,000 from January through March of this year. I’ve enjoyed reading your posts.

For the time being at least, I don’t know if I’ll ever buy a house again. I enjoy the flexibility and “perks” of renting – not dealing with repairs, able to move without having to worry about selling, etc. I know there are downsides just like anything else, but for now, that’s where my mind’s at.

And I definitely hear you on the Austin area. My brother lives out there as well and it’s mind-boggling to hear how much his home value has increased and is projected to continue doing. That’s insane over there! 🙂

Thanks for this post, Jim. You have me thinking about our asset allocation. We’ve been all stocks all the time in our accumulation phase, but now that I’m retiring from corporate life (June 1!), it’s high time to reconsider that.

Also, should this be VGSLX instead of VTI?

“If I buy up VTI with all that spare cash in the retirement accounts, I’m just about right where I need to be.”

Good catch on that, Sarah – you were definitely paying attention! 🙂 I fixed it in the post.

Congrats on getting ready to retire from corporate life… almost there! 34 working days until June 1? I put in the question mark because I’m sure you know that without even looking it up! 🙂 You’re right to think about asset allocation – it’s one of the most important facets of investing. I didn’t realize that until reading the Stock Series from JL Collins – that was like a light bulb moment for me. Enjoy your retirement!

Thank you! I actually didn’t know the number of work days left, but I did create a countdown clock that I like to look at:

https://www.timeanddate.com/countdown/retirement?iso=20210601T17&p0=810&msg=Bye%2C+Corporate+Overlords%21&ud=1&font=cursive&csz=1#

🙂

Love it! Congrats!!

This was great, I like the thinking behind the rebalancing and similarly started to look more into REITs and alternatives. Do you feel that the income from REITs should be compared as an equivalent to running your own property? Isn’t the income you earned at a far higher yield than REIT due to the leverage and taxes being in your hands instead of distributions at REIT? VNQ seems to have a lower yield than what people are quoting for their cash-on-cash returns but maybe Twitter only brags the winners =) Of course personal real estate is active which isn’t something you’re looking for anymore if I read correctly?

I was on a 75% equities, 25% fixed income split, but have now started moving from a pure net worth asset allocation to an income sources allocation model.

Under my income sources allocation model I want to start having equal income come from Shares, Bonds, RE and alternatives. I do a sense check on the numbers that spits out from a net worth perspective for inflation, but it actually works out pretty well. That way I went from a traditional 70% equities, 25% bonds, 5% cash to a new model of 60% equities, 10% bonds, 15% RE (mostly reits), 15% alternatives based on target yields and equal income from each source. It also reduces my stress around the volatility of markets and rather the more stable dividends and income from year-to-year. I also like the idea of not selling equities to fund lifestyle.

I’m not really selling and just using extra cash to move to an income model, since we need the majority of our investment cash to pay for day-to-day expenses. It’s nice to just have a nice goal to work towards =)

Nice post, this is definitely the type of thing that post-FIRE we still need to manage the portfolio!

I likely will make less money from the REITs over the long run than I would if I had kept the rental property. However, I lose the tenant headaches, the property management headaches, and the need to worry about making repairs and improvements. I also gain diversification, liquidity, and I don’t have to deal with the complexities of the business (insurance, taxes, the mortgage, etc.). Since I’m trying to simplify right now, giving up some income isn’t a deal-breaker. For others, owning rental properties might be the smarter move. Like you mentioned, the leverage and tax breaks are nice advantages to have.

I like your goal of building a balance between stability and income. Everyone thinks they know what they’re doing right now since the market just keeps climbing. But when it falls, that can be a real stressful time and people tend to freak out and sell. Reducing your equity holdings should help alleviate that stress somewhat.

I have one question. Why not have some REITs in your taxable account? Would the income push you up the tax bracket or something like that? A little income is good, right?

We have about 80% in equity, 10% bond/cash, and 10% alternative. I think that’s okay at our age. I have 30% in bonds previously, but the performance lagged too much. We don’t plan to withdraw anytime soon so I think having more equity is fine.

You’re absolutely right that I could keep some REITs in my taxable account. We shouldn’t need that though because of our bucket strategy. Since we have bond funds that mature to give us our “yearly allowance”, we can leave the REITs to reinvest and continue to grow tax-free in the retirement accounts.

I like your split and would probably move to something similar if (and when) we have more income coming in like you do. Since we’re withdrawing every year, that would probably be too much on the equity side for us.

Great insights Jim. I too think REITs could be a good investment as the economy opens back up. Also, cash may be a good place to be in right now if the market takes a dip after the run it’s been on since the recession 2008-2009. (Just as you mentioned, I’m not a financial advisor, please consult a professional advisor before any investment decisions.)

It’s crazy how the market just keeps growing (dip from last March aside). We all know that it’s going to go down at some point, but as someone really no longer in the accumulation stage, I’ll take it! 🙂

Every year, I think that 10% – 15% cash is way too risky and have the rest tied to risky assets that have a chance of losing money. And every year, I am consistently proven wrong and that 10 – 15% isn’t risky enough, ha.

Well, you’re already in such a good spot. No matter which way you go, your portfolio will be just fine 🙂

Haha, you never know what’ll happen with those risky investments. Might be good one year and the next year you get crushed. It’s always about finding the right balance.

A good low fee conservative option for you – Vanguard has a good single fund, also add some Foreign diversification which you might want to consider:

https://investor.vanguard.com/mutual-funds/profile/VTINX#tab=2

I’m good with what I have now that it’s been rolled over to Vanguard, but thanks for the suggestion, Robert!

Hi Jim, just discovered your site last night. We do happen to know each other through your cousin, Dave, but that is for another time. I too have recently been rebalancing out of cash. I had/have my emergency fund in 12 12-month CDs with one maturing each month. Due to the terrible interest rates, I started withdrawing them and placing them in a municipal bond fund. Return there is historically much higher. I am about halfway through the process and we shall see how that works out. Keep up the great work!

I know you, Tom! So glad you found my site! That sounds logical to me – the CDs aren’t offering anything right now and municipal bond funds can be a solid alternative to keep your emergency fund. It’s kind of a wacky time we’re in right now with interest rates so low, but actively digging in and finding places to stash your cash to squeeze out some extra money can make a nice difference over the long haul.