Doing a Roth conversion can be the key to a successful FIRE (financial independence, retire early) strategy. That’s definitely the case for us.

By doing some financial planning, this one move is allowing us to access money in our pre-tax retirement accounts with no penalty and the ability to pay little to no tax when it happens.

Today, I’m going to take you through some more details on what a Roth conversion is and why it’s so valuable. I’ll also share with you the steps we took in making it happen.

What is a Roth conversion?

A Roth conversion (more formally known as a Roth IRA conversion) is simply a matter of moving all or part of the money from a traditional IRA to a Roth IRA.

That’s it.

Simple right? You’re moving pre-tax dollars you socked away in one account to an account that holds post-tax dollars.

With a traditional IRA, the money gets put in without having been taxed (sometimes as a tax deduction when you file your annual return). Then you pay taxes when withdrawing your money, which is normally no earlier than age 59½.

A Roth IRA, however, is funded with dollars that have already been taxed (think of it as the money that’s already been taxed through your paycheck). Because of that, the money in a Roth IRA doesn’t get taxed when you withdraw it.

So when you do a Roth conversion, you need to pay the taxman on the money you moved. Uncle Sam wants his share and that can cost a good chunk of change on your tax return.

So why even do a conversion like this?

The Roth IRA is a fantastic account. Knowing that “what you see is what you get” in the account is pretty valuable. When tax rates go up, it won’t matter with the Roth – you’ve already paid your taxes on it. With a traditional IRA, don’t get too excited about the value because the taxman’s going to be standing there waiting like the grim reaper!

A Roth IRA can also be valuable if you expect to be in a higher tax bracket when you’ll be withdrawing the money. At 70½, the law states that you need to take required minimum distributions (RMDs) from a traditional IRA. If you’re still working and in a higher tax bracket than today, those RMDs will be taxed at a higher rate.

A Roth IRA doesn’t have RMDs (unless it’s an inherited IRA). That means you don’t need to worry about if you’re in a higher tax bracket down the road. It also means that the money in a Roth can continue to grow tax-free after 70½ if you don’t need the money at that time.

On top of that, Roth IRAs have more flexibility. Contributions on a Roth IRA can be taken out penalty-free at any time. Notice I said contributions – you can’t take out gains or you’ll be hit with an IRS penalty of 10%. In other words, if you’ve contributed $15,000 to a Roth IRA and it grows to $20,000, you can pull out any amount up to the $15k without penalty, but you’d be dinged if you tried to touch that $5k in growth.

To take advantage of these benefits and several others, it can make a lot of sense to contribute as much as you can to a Roth IRA. And there are some sound financial strategies to get around some of the contribution rules for Roth IRAs as well.

For example, high-income earners aren’t eligible to contribute to a Roth IRA. However, a Backdoor Roth is an option that can be used. My friend, PoF, from Physician on FIRE, discusses how he uses that strategy in his Backdoor Roth IRA post.

Using that approach, you can also get around the contribution limits. For both 2019 and 2020, a Roth IRA only allows contributions of up to $6,000 each year (or $7,000 if over age 50). Doing a Backdoor Roth helps get around those limits.

So yes, you do pay taxes on the conversion, but the money can now grow completely tax-free for as long as it’s in the account. That’s a huge benefit!

But why is a Roth conversion valuable to an early retiree?

For an early retiree like myself, those Roth conversions can be extremely valuable.

The largest part of our portfolio was sitting in the 401(k) I had through my employer. I started to contribute to the plan as soon as I was eligible (around 1999!) and I continued to increase my contributions every year. Eventually, I got to the point where I was putting in the federal max every year.

Because of that and a generous match from my employer (roughly 35 cents on every dollar contributed with no cap), I was able to grow that account significantly. When I left the company and rolled it over to a traditional IRA, it was worth a little more than $690,000… that’s the miracle of compounding!

Although we had other accounts to also use in early retirement, the problem was that this nice nest egg and the $100k+ sitting in Lisa’s old 401(k) were sitting in traditional IRAs. That meant we couldn’t touch the money until age 59½.

That doesn’t work well for us! We need to be able to access the money in our retirement accounts sooner.

Remember how I mentioned that you can take out Roth contributions at any time penalty-free? Yeah, well, that’s what we plan to do.

The clincher is that when you do a Roth conversion, that money only counts as a contribution to the IRS after it sits and bakes for 5 years. So, we can convert the money at any time, but each conversion will take 5 years until we can withdraw it without being penalized.

And with that, I’ve talked before about how we planned to do a Roth IRA conversion ladder once we retired. That would allow us to move the money from the traditional IRAs slowly (so we don’t get taxed too heavily) and then begin withdrawing it penalty and tax-free in 5 years.

So here we are having been retired for the year.

Why wait until so late in the year?

As I post this, it’s now mid-December. I could have done the conversion at any time throughout the year but I waited until now.

Why?

Because it’s important to see where we stand tax-wise for the year first. That will determine the optimal amount that we can convert without getting bumped up into another tax bracket or needing to pay too much all at once.

With that, it was time to talk to my friend, financial planner, and accountant extraordinaire, David, from Remote Financial Planner. We set up an appointment to discuss my current state of affairs.

I sent him over some numbers on the income and expenses from our rental property and the three small businesses we have. I also had a couple of weeks of a paycheck as carry-over from my employer at the end of 2018.

Then there were some deductions we had throughout the year in donations – that’s what happens when you get rid of everything you own! And finally, we had some dividend and interest income as well.

He took all the numbers and ran through everything just like he normally would when doing our taxes… a rough draft so to speak.

When all was said and done, we looked at a few different options:

| Base | Scenario #1 | Scenario #2 | Scenario #3 | |

|---|---|---|---|---|

| Amount to Convert to Roth IRA: | $0 | $35,000 | $60,000 | $96,000 |

| Refund: | $1,477 | $692 | $0 | $0 |

| Tax Due: | $0 | $0 | $2,308 | $6,821 |

| Tax Rate on Conversion: | 0.00% | 5.00% | 7.80% |

It’s incredible to see what a deal we’re getting on our taxes by doing it this way. The Mad Fientist detailed out this strategy perfectly in his post, Traditional IRA vs. Roth IRA – The Best Choice for Early Retirement and it’s astounding to actually see it in action.

For this year, we decided to go with Scenario #2 and convert $60,000 from my traditional IRA to my Roth IRA. That gets a nice chunk of money moved over without hitting us too high with taxes due for the year.

So by waiting until the end of the year, we were able to determine the amount of the conversion that makes sense for us. We’ll continue to do this year after year until we’ve drained our traditional IRAs completely.

Think about how powerful this approach is. We put tax-free money into our retirement accounts and let it grow tax-free. Now we’re pulling out the money at such a small marginal tax rate that barely a blip in our lives.

That’s why it’s so important to continue to learn what you can about personal finance. The amount of money you don’t realize it’s costing you otherwise can be extraordinary.

The steps we took to do our conversion

Considering I just did our Roth conversion a couple of days before I started this post, you’re getting information hot off the press!

Most of our accounts are at Vanguard so your steps might be different, but the concepts are the same. Contact your brokerage for help if you need it.

Here’s how I did a Roth conversion of $60,000 at Vanguard (click on any image to see it full size)…

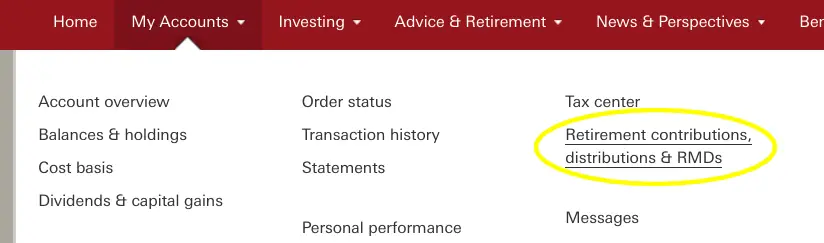

Step 1) Log into your Vanguard account. Hover over the “My Accounts” menu and select “Retirement contributions, distributions & RMDs”:

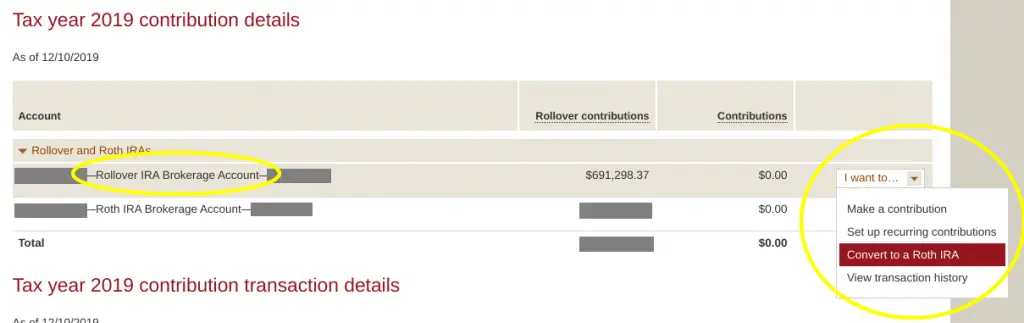

Step 2) Locate your traditional IRA (or your rollover IRA if it was rolled over from another account like a 401(k) plan). In the “I want to…” dropdown to the right of the account, select “Convert to a Roth IRA”:

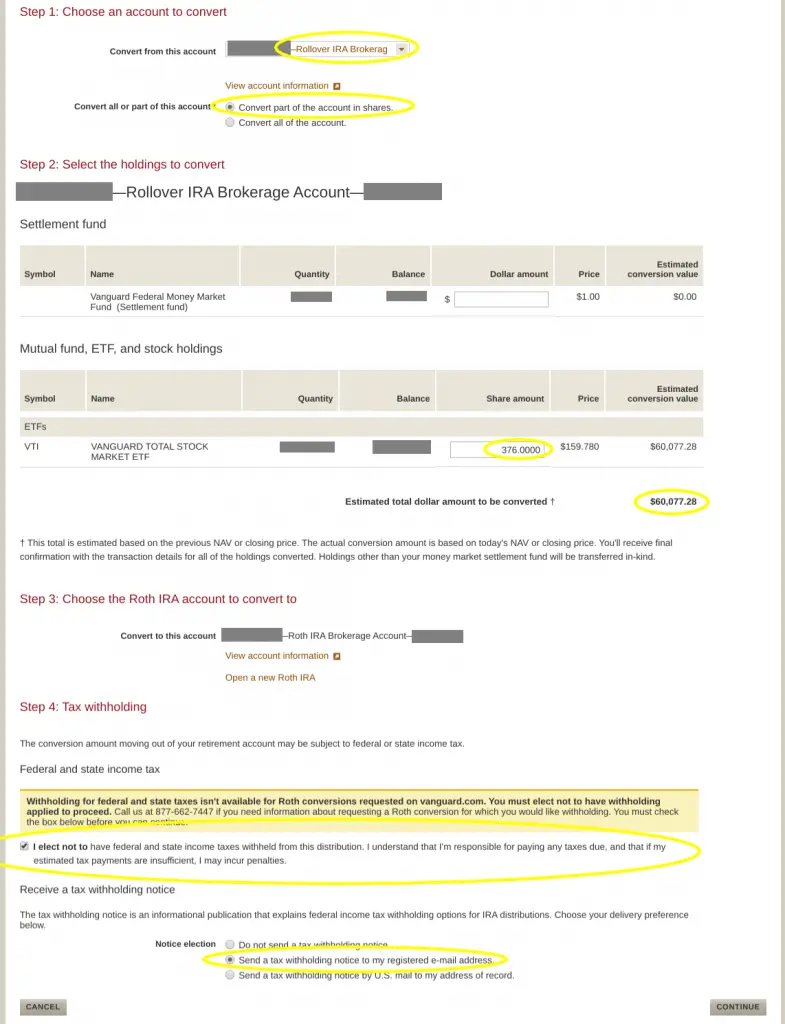

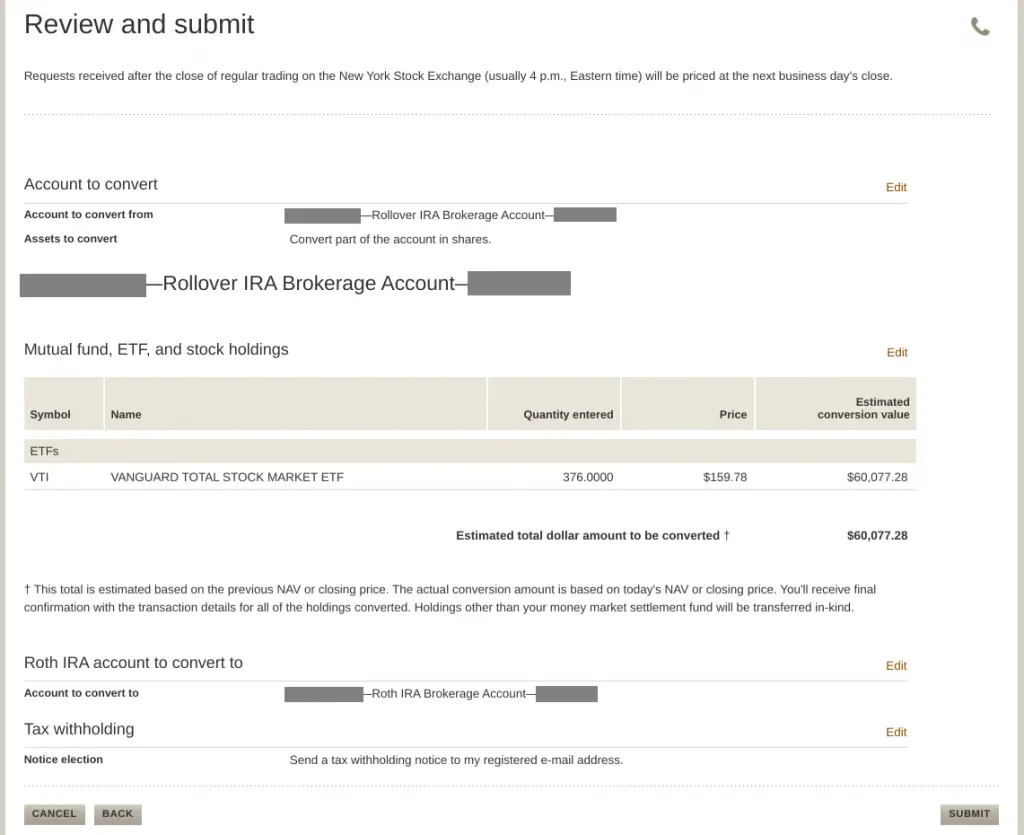

Step 3) This is where you really need to pay attention or you’ll regret it if you mess up!

- Make sure that the “convert from” account is correct. It should be already selected if you chose the right account in the previous step.

- In most cases, you’ll want to convert just part of the account so select the appropriate option there.

- Now you have to do a little math. I wanted to convert about $60,000 worth of my VTI shares to my Roth. So I just took 60,000 and divided by the current price which they conveniently list for you. 60,000 / 159.780 = 375.516334961. I rounded up to 376 and entered that for my share amount. That made the estimate just a little over $60k.

- Review the estimated dollar amount to be converted!

- Ensure that your correct Roth IRA is selected as the “convert to” account. If you don’t have one, they’re nice enough to give you a link to open one up.

- For the tax withholding, I wanted to handle that myself so I checked the box. And they weren’t giving me an option to do otherwise, so that’s all the better! I’ll talk about this a little more shortly.

- I asked for an email on tax withholding – your call on if you want to do the same.

- Click “Continue” when you’re sure everything’s correct.

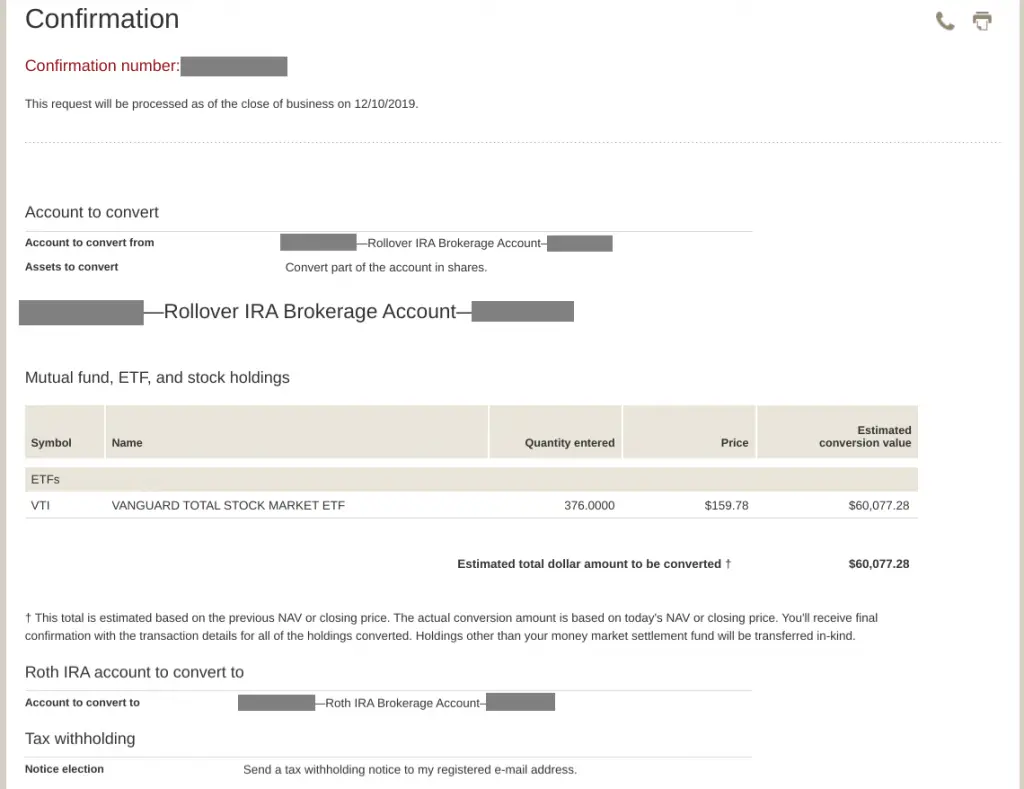

Step 4) Last chance to make sure you didn’t screw this up! Hold your breath and click “Submit”!

Step 5) There is no Step 5… you’re done! Here’s your confirmation to prove it!

As it mentions, it’ll be processed at the close of business. Sure enough, the next morning, I got an email confirmation stating that the Roth conversion was done. Mission accomplished!

Estimated tax payment

One last thing, bucko! If you’re in a similar position that we are, you’re probably not getting a refund. In fact, with the Roth conversion, you’re likely going to owe some money with your tax return in April.

Here’s what’s important – you don’t want to get hit with a penalty and interest from the IRS come April. To avoid that problem, it’s important to do an estimated tax payment if you’re going to owe money.

I recently moved over a sizeable chunk of this year’s spending “allowance” to a 1-year CD earlier this year. With interest rates dropping, I thought this would be a wise move to hang onto a little more of our hard-earned money.

Because of that, I’m running a tight ship until the end of the year. That doesn’t mean we can’t come up with the money if needed, but it would involve a little more effort.

The good news is that the estimated payment isn’t due until mid-January. So when our BulletShares mature in our portfolio and we make our next move to get our 2020 spending money in the first week of January, I’ll make a $2,500 payment to the IRS.

That’s it – a Roth conversion can be an early retiree’s best friend! Being able to legally save thousands of dollars in taxes through financial strategies like this can be huge!

Is the idea of doing a Roth conversion something you’ve considered doing before? Was this information helpful?

Thanks for reading!!

— Jim

Jim – excellent article but I think there is a typo – That meant we couldn’t touch the money until age 70½.

Did you mean to say at age 59.5?

Thanks.

Thanks, Matthew, but you’re actually good to withdraw money from a traditional IRA at 59½. 70½ is when the withdrawals become mandatory (RMDs). Here’s a quick link with a little more info. Hopefully that’s some good news in your retirement planning! 🙂

Really useful and helpful post, Jim. Thanks for writing it up and including annotated illustrations for Vanguard accounts.

Quick question: Converting funds from a Traditional IRA to a Roth would effectively change all of those funds into contributions, including any funds generated as growth while part of the Traditional IRA, right? Meaning, you could pull out all of those converted funds (after 5 years of course) penalty-free even before age 59-1/2, since you paid taxes on them when converting them over.

Thanks again.

That’s correct, John, and exactly what we’re doing. Once you’ve had the money rolled over into a Roth for 5 years, the IRS now recognizes those funds as contributions. Same rules apply at that point where you can withdraw your contributions without penalty (or any more taxes).

I am confused on the tax rates of 5% and 7.8%. I thought the conversions were taxed as ordinary income? For 2019 were do not have 5% and 7.8% tax brackets?

In process of doing this very thing this week so your article was very helpful. For those of you with Charles Schwab, I called yesterday and they were extremely helpful and said they could either walk me through it online or they could move the money. One more call today with tax accountant and I should know exactly how much I want to convert.

Awesome to hear, Connie – hope the process goes smooth for you!

As far as the rates go, I’m not an accountant by any means (that’s why I have a good one!), but my understanding is that it’s taxed as ordinary income. However, because that is basically our only income for the year for the most part, after the standard deduction and other deductions, those smaller numbers are what the tax rate becomes on the conversion. Not too shabby, right? If we did the conversions while we were still working, that’s when it becomes much more expensive.

You mention a “ladder” for the Roth. Each conversion does not require a 5 year hold. So the clock starts with the first year of a Roth IRA. There is no 5 year clock for each conversion.

BTW When you roll a Roth 401k to a Roth IRA the Roth 401k clock is ignored and a new 5 year clock is started.

Jim, please follow up on this. Is Tom correct?

My impression is each conversion requires a 5 year hold. It doesn’t make sense if withdrawal is contingent on just the first conversion. Then, you can convert $100 on the first year. Then convert $60,000 on the 5th year.

I don’t think Tom is correct here.

I’m 99.9% sure that is not correct. I’ll verify to ensure that there’s no misinformation, but right not I’m in Grand Cayman as part of our cruise and I have a limited signal. I’ll follow-up here when we get back from the trip.

Ok, I’m finally back from our cruise (woe is me, I know!). We’re actually at the airport right now, but I wanted to dig into this and ensure that the correct info was out there for everyone.

According to Publication 590-B (2018), Distributions from Individual Retirement Arrangements (IRAs) from the IRS:

Distributions of conversion and certain rollover contributions within 5-year period. If, within the 5-year period starting with the first day of your tax year in which you convert an amount from a traditional IRA or rollover an amount from a qualified retirement plan to a Roth IRA, you take a distribution from a Roth IRA, you may have to pay the 10% additional tax on early distributions. You generally must pay the 10% additional tax on any amount attributable to the part of the amount converted or rolled over (the conversion or rollover contribution) that you had to include in income (recapture amount). A separate 5-year period applies to each conversion and rollover. See Ordering Rules for Distributions, later, to determine the recapture amount, if any.

To be clear, the important sentence in this is: A separate 5-year period applies to each conversion and rollover.

So yes, there is a 5-year clock for each conversion that is done and that’s the key to constructing a Roth IRA Conversion Ladder.

Hope that helps clear things up! 🙂

Jim, this is a super helpful post. Your step by step example answered a lot of questions I have, and it was interesting to learn your timing and considerations to make. Very interesting about the estimated tax payment in January too, was not aware of how important that is!

Thanks also for sharing your financial planner link. I have a feeling my wife and I will want his help walking through this as we get closer!

Mike

No problem, Mike – glad it was helpful!

This is a really helpful post. We aren’t to that stage yet, but it’s like we’ll need to do the conversion ladder for a few years if we do decide to retire early. The step by step approach here (with screenshots!) is really useful. Thanks for sharing you’re specific example, it’s helpful to see how you considered everything up to and through the decision.

Thanks, Ed – funny enough, it’s nice to have it documented for myself as well! Next year, I can just look up this post to see how to do it again! 😉

Thank you SO MUCH for posting screenshots. I bookmarked this for our own conversions in 2020 (starting our ladder next year). Very valuable information!

Thanks, Kim – it was much easier than anticipated as long as you don’t rush through it. 🙂

Just be careful if there are ACA subsidies involved, which is the case for many early retirees. A large enough Roth conversion can cause one to go over the “ACA Cliff” and pay back ALL premium tax credits received. That could be many thousands of dollars.

That’s an excellent point, Charlie! With us living in Panama and having expat insurance (just in case), this doesn’t apply to us. But for a lot of folks, that could be a big deal. Thanks for bringing it up! 🙂

Why do you have to make an estimated $2500 tax payment in January? I thought you said this conversion isn’t resulting in any tax due?

I did this same conversion last summer on a small traditional IRA I had but my husband arranged for additional withholding from his paycheck to cover the tax that would be due. I’m glad I did it as you pointed out the IRS would penalize us for it which I didn’t know. Thanx for all the valuable info.

Hi Debbie, it’s not that I don’t have any tax, it’s that I have a small amount of tax due. I could have converted over less so I’d pay nothing in taxes, but this is a great deal and fits into our plan of moving over a good chunk every year to keep things moving.

Smart move on the withholding to cover the tax due on the conversion so you didn’t get any surprises later. Hope your holidays are great, Debbie!

I know that this is several years late – but…

According to my CPA, even though I am doing my ROTH conversion in December this year, because I did NOT make estimated tax payments throughout the year, I am going to be hit with penalities because the IRS automatically annualizes your income(Roth Conversion). This means that it is assuming that you should have been “receiving” the income over the entire year and thus should have been paying taxes throughout the year. Thus, even though I have no idea ahead of time how much I can convert until December which is when I do the Roth conversion, it doesn’t matter. I am penalized for not splitting the taxes due over the entire year.

And by the way, my state also does the same thing.

Did you run into this same issue when you did your taxes for the year you did the Roth Conversion?

Interesting… I’m not an accountant, but my understanding was that that’s not the case. I was told by my accountant that it needs to be done during the quarter you receive the “income.” I mean, what would happen if you suddenly won the lottery in December or some other windfalls? Would you be penalized for the unexpected income? That doesn’t add up.

I didn’t dig around on it too much but I do see that Investopedia states:

“Estimated tax is a quarterly payment of taxes for the year based on the filer’s reported income for the period.”

Obviously, that’s not the IRS documentation but it does line up with the way I understood it.

To answer your question though, no, I’ve had no problems. Maybe the key is that I pay the estimated tax payment to cover the Roth conversion a few weeks after before the deadline. I do make an estimated payment, but only in the quarter that the conversion was done (4th quarter income payments need to be made by January 15th of the following year).

Again, I’m not a CPA (or even close!) but those are my thoughts. Hope that helps! 🙂

We are in our 50s and have way too much in tIRA, but have made a decision to convert only $50-65K a year for the next 20 years, which unfortunately (or fortunately, really) only barely covers the gain in the IRA, assuming average 8% annual. That said, since the RMDs are only starting at 75, we figure that if we still have the same 7 figures in our portfolio, given inflation and that tax brackets are indexed to inflation, we will be fine with the RMDs. Better to have too much money at 75 then less money in our 50s and 60s. It may be good to even have income in your RMD years to max up to your standard deduction or your schedule A amount if you itemize.

Point is, it’s personal to everyone’s situation, and if you’re in a position to not pay too much every year and whittle your IRA to zero, then that’s a great goal. However, if you have a high balance in IRA, it may not make sense to pay a lot of tax upfront, and increase your MAGI to kill off all subsidies (i.e. APTC, medicare, etc), or if you anticipate any liquidity events, cap gains, etc, etc.

I sort of wish we could convert 100% but unfortunately it’s not realistic for us unless we want to convert at a high marginal tax bracket.

Good point on this. That’s a good problem to have, even though it’s still not ideal. Even though it’s a little early in the game, I’m seeing that our IRA is outgrowing the money we pull out for conversions as well (so far). I’m sure there will be years where that’s not the case, but it is what it is. We’ll keep trucking along and we’ll just likely need to do RMDs as well when the time comes. Not ideal, but still a good problem to have.

First world problems, for sure. My spouse’s tIRA accounts alone YTD are up $186K, and we’re not even out of Q1. Of course, Q2 and the rest of the year could be terrible, but there’s no way to convert enough to get the balance to zero ever…unless you want to go straight up the tax brackets. We first thought about it when we first retired 3 years ago, should we bite the bullet to make a huge dent in the tIRAs and pay through 22% or 24% brackets and lose all ACA subsidies? We still think about it.

Then there’s the timing of the market — converting during market corrections so you at least convert at lower prices. We did a little in the beginning of 2023 when market was still low, but as we got into Q4 and could project more clearly our income for 2023, we pulled the trigged during that Oct 2023 correction, which was helpful. But had we done it all early in the year, say Jan or Feb 2023 before the market started its upward trajectory, we would have made out better.

C’est la vie…just can’t optimize everything nor time the market. You win some and you lose some, but as stated earlier, these are serious first world problems.

Sounds like you guys are in good shape too…congrats!