Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

Anytime you can throw the words “million net worth” into a discussion, the words “scraping by” shouldn’t follow. It just doesn’t fit the bill.

Now before I continue, let me say that we’re fine, but we ran into an interesting financial problem that has messed us up this year. And, of course, my job is to share that with you so you can make sure you don’t run into a similar small dilemma.

I’m always very forthcoming regarding our money situation – both on this blog and in “real life.” It’s so weird that talking in-depth about money can be such a taboo subject.

So telling you that we have over a $1.3 million net worth shouldn’t be a surprise. I wrote about when we first hit $1 million in April 2017 and I update my net worth page every month. We’ve also been extremely fortunate to have such a great market return during our first years of retirement.

But even though a $1.3 million net worth is comforting, there are still problems that I don’t hesitate to tell you about. Whether it’s an investment property that wasn’t the best, almost losing the Panama dream, or struggling to find balance in early retirement, you get it all here!

Today, I’m going to tell you how we’re scraping by just trying to make the numbers work until the end of the year…

A smart decision?

As part of our drawdown strategy, I move about one year’s worth of spending from our investment accounts to our online savings account. Right now, that amount is about $50,000/year. That’s more than we normally spend each year so that gives us a little breathing room.

In early March, I decided to take some of this extra “breathing room” money and move it into a CD. Interest rates were starting to drop and I wanted to get a little more return on our cash-on-hand.

In the worst case scenario, I could pull the money from the CD prematurely and pay the penalty, which would mean only losing 60 days of interest. That’s far from the end of the world.

So I moved $15,000 into a high-yield CD at Ally. At the time, calling 2.00% “high-yield” seemed a little silly. But as I type this, that same CD is offering a 0.65% yield and we’re now only getting 0.60% on our online savings so I guess that was a good move.

Of course, making that move meant it would be a little tighter this year, but we had no plans to do anything crazy. It’s not like a pandemic was about to hit, uproot everyone’s lives, and turn everything upside-down, right? Oops.

Becoming a Piloteer was unexpected

First off, who woulda thunk there’d actually be a devoted fan base for Pilot owners called Piloteers… but there sure is!

Anyway, like most everyone, this pandemic threw us off-balance. Once we got back to the U.S. on a humanitarian flight, we soon realized we couldn’t do much anyway. Visiting with friends and family during a pandemic required a little more strategic planning. Additionally, we were being careful so didn’t want to make that too much of a regular thing.

So… what to do?

We bought a car and went on a road trip! It sounded like a great idea and it was but it certainly wasn’t a cheap endeavor. And buying a used car was the bulk of our expense for this trip. Not only did the 2012 Pilot cost $12k but then there comes the other fun of taxes, registration, insurance, gas, etc.

And even though we talked about selling it after our trip, we liked it so much that we didn’t put in too much of an effort of making that happen. Now she’s all ours and resting comfortably at my parents’ house waiting for our return!

A road trip can be costly

We have so many great memories from our 40-day road trip this past summer that I can’t complain. Plus I had all sorts of fun posts that came out of the deal:

- When Life Gives You Lemons… Take a Road Trip!

- Tennessee and Arkansas – Leg 1 of the 2020 Road Trip!

- Three Weeks in Texas – A Big Stop on the Road Trip

- El Paso, Tucson, Viva Las Vegas!! – Road Trip Leg 2

- An Overnight at Cracker Barrel and 5,863 Miles Logged

- Here’s Why I’m Liking… RV Parky

- Free Nights – We’ve Had 5 at Hilton Hotels Recently

That’s a lot of solid material for the blog! Sheesh, the things I do for you guys! 🙂

But alas, that came at a price. It was an expensive amount of fun. Sure we cut corners all over the place to bring the costs down big time. However, our gas costs alone were over $600. Throw in various lodging, entertainment, and food along the way and it becomes some good money gone.

Mint is telling me that we spent $7,821.34 during those 40 days. And we had pre-paid our rent for our place in Panama for a couple of months before we left from there earlier in the summer. So that amount is without even the cost of rent!

To give you an idea of our normal spending while in Panama, I thought $3,468 for a month there was expensive! So yeah, even with a $1.3 million net worth, pushing our spending close to $8k for 40 days is waaaaaay outside of my comfort range.

Having a $1.3 million net worth and scraping for pennies

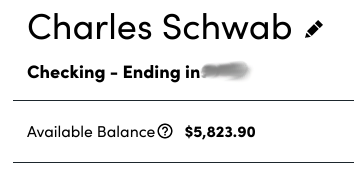

Our automated transfer has already taken place from our savings to checking for November, so here’s a look at our checking account balance:

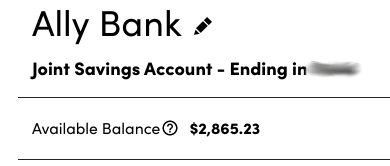

And what’s left in our online savings account for the year:

Finally, here’s the total of our outstanding credit card bills, which are set to auto-pay on their due dates:

Just so you know, I was able to easily grab all this info using Empower (formerly Personal Capital). It makes it easy to see all your balances, transactions, and investments from all your financial institutions in one dashboard. Best of all, it’s free. Because it pulls all your information together, you can also easily use their tools like the Retirement Planner, Retirement Fee Analyzer, and Investment Checkup to ensure you’re on the right track (also free, I might add!).

If you look at the numbers, we should be Ok getting through November, but then we’re going to come up short by about $135 in December. The $3,000 transfer scheduled for December 1 isn’t going to happen. There’s no minimum balance at Ally, but I’d at least have to drop the transfer down to maybe $2,860 at the most.

Don’t forget, we do spend more than $3,000 in months, too. Usually, we have a nice buffer in each account, but it ain’t happening this year. We’re really cutting things close.

And the only reason that we’re still in the right ballpark is that I started moving money from other places to this account. For instance, I moved most of the money from my Route to Retire business checking over to help fill the online savings bucket.

So there you go – we have a nice million net worth but we’re still scraping to make sure we have enough until the end of December (and maybe a week into January). It’s a strange phenomenon but understanding the why hopefully made this a little more clear.

My game plan now is to borrow a little more money from other places. Unfortunately, our duplex has had a rough year (I’ll talk about that in an upcoming post). So that business account is down to basically nothing and has its own problems – ain’t no money coming from that account!

In an effort to ensure we have a little bit of a buffer to cover us, I’ll probably have to scrape from the Route to Retire business checking again. And if that doesn’t cover it, I’ll borrow from Faith’s savings account with Ally. Then I can pay her account back (with some interest) at the start of next year… ssh, don’t tell her!

And as a reminder, if we run into a big emergency over the next couple of months, we could always cash out our $15k CD early. We’d lose a little bit of money but nothing substantial – probably around $60. But to me, there’s a challenge in not touching this account so I probably won’t do that.

We’re good – in fact, we’re better than good with our $1.3 million net worth

Before you start commenting that I left my job too early, we should have saved more, blah, blah, blah… save it. We’re just fine.

We’re actually better than fine. Think about what transpired.

That $15k in the CD is set to mature in March 2021. That means we’ll have our $50k we’ll move over to savings for spending for next year PLUS an additional $15k. We only spend about $35-40k per year so suddenly, we’ll have an extra $25k for the year… not too shabby!

And, as a bonus, we now have a car that we can use when we’re back in the U.S. or can sell if we decide to down the line.

Life is good even if we have to do a little more planning due to some unexpected occurrences. Nothing like a small pandemic to change everything in the blink of an eye!

Has the pandemic messed with your finances this year in either a good or bad way?

Thanks for reading!!

— Jim

I appreciate hearing your method of funding your spending “bucket” each year. I am older than you but just starting this journey of transitioning from a regular paycheck to the reaction of my personal pension. Your experiences are helpful to me. Thank you. Terry

There’s a certain bit of a learning curve to the transition, but after automating a lot of the transfers to create your own paycheck, it becomes much easier. Having a pension will likely make this process even easier so I’m sure that’ll make it a smoother process for you. Best of luck!

As we near retirement in a year or so, we are financially prepared. But I have this nagging concern that dipping into savings, if necessary, will be stressful. We put so much emphasis on saving that I can’t imagine not doing it in retirement. The pandemic has made us more excited though to get out again and explore!

It’s definitely different not actively saving anymore. However, you can start to do more passive saving even in retirement. And by that, I just mean not spending the amount you have to spend each month or each year. The next year you don’t need to pull out as much money since you still have leftover money from the previous year. The less you need to pull out to use, the more time it has to sit and grow.

Although this has been a freak year, we did that process last year and should be good to repeat it again next year. Good luck, Marshall – retirement opens up so many doors in life!

We are in Year 5 of FIRE now & traveling nomads. Before retiring & after reading some early retirees’ “lessons learned” on weathering the 08-09 recession, we decided to keep 2 years living expenses liquid & out of the market. A years’ worth is sitting in I-bonds we have had for years pre-FIRE. We replenish the cash once or twice a year when we think the market is “up”. It definitely helped us during the pandemic drop (& quick recovery, yay!). We decided during the drop that we were cool if it kept dropping to just spend down & not replenish this year, which was the whole point of keeping 2 years expenses out of the market. Gives us alot of peace of mind, so just wanted to share.

You did really well this year buying a car & you still have that CD, so you spent less than your budget with your trip home and road trip & all! Love reading your blog. Thanks do much for sharing.

Smart move on keeping money liquid like that, Lisa. Our plan is similar but we go a little overboard and have about 5 years in cash and bonds. It is great to be able to take advantage of the market when it does stupid things, isn’t it? 🙂

Congrats on 5 years of FIRE and being traveling nomads!!

Did you pay for the Pilot in cash? Seems like that would set you back quite a bit.

I tend to over-optimize as well. I don’t like to have a lot of cash around because it’s better to be invested. We’ll need to change that mindset before Mrs. RB40 retires.

Would you increase the cash cushion a bit going forward?

We did pay for the car in cash – it seemed to be the best move to make… especially when we thought we’d be selling it a couple of months later.

Makes sense not to have extra cash sitting if it can make more money elsewhere. As far as our cash cushion goes, we’ll end up building up a bigger buffer just because of that extra $15k coming our way. Since we don’t normally spend as much as we did this past year, we should continue to have a good chunk of change “extra” each year. I’ll probably keep an extra $15k just in case, but like you, I’d rather have the extra money working for me elsewhere if possible.

i just ran into a similar cash dilemma and moved some money out of ally when they dropped to 0.60%. full disclosure: we’re right now a 1.5 job household and went from accumulating to neutral the past 2-3 years and just lived off our paychecks. anyhow, i had been building up a cash position and hit around 75k but could not take that low interest rate. i ended up with 30k in high yielding and monthly paying preferred stocks etf’s and 20k in stocks so now we only have 25k cash on hand. i’m thinking of reversing most of this move as i liked having that cash cushion. if we end up changing our minds i’ll only keep 20k invested in preferred stocks to mimic a yield of 2% on 75k while only having 20k at risk instead of 50k.

anyhow, that’s a really interesting post and very enlightening to hear from a real retiree living off investments. it’s much appreciated for those of us about to pull the rip cord soon. cheers.

It is definitely comforting to have a decent cash buffer. I like your idea of splitting it up just so you have enough on-hand that gives you peace of mind. Even if it isn’t earning much, it’s worth it if it helps you sleep better at night.

The trip looked well worth the additional expenses you incurred. We still need to prioritize life experiences, even if they don’t always mesh with our savings goals! And who doesn’t have sleeping in a Cracker Barrell parking lot on their bucket list?!

Personally, I’m thinking of pulling my emergency fund out of my “high-yield” account as the interest rates just aren’t worth it. Just haven’t decided where, or even how much, I feel the need to keep in cash.

Appreciate the candor as always!

Haha, I’m looking forward to hearing when you make your Cracker Barrel parking lot story happen! 😉

It does suck that you can’t get much out of your cash right now, but sometimes we just have to suck it up and take the pennies they give us. If it’s money you might need in the short term, putting it anywhere risky could be a bad move.

Our cash cushion dropped down significantly this year too. Similar to you, this was purposely done. We just wanted more exposure to the market, high yield interest rates aren’t worth it for us. We’ve decided that if an emergency occurs, we’ll use our credit cards to cover while we sell equity to pay the surprise expense.

So cool to see you challenging yourself and staying disciplined. Appreciate the insight. Have you noticed any price increases down in Panama due to Covid? Seems like everyone up here in the Bay Area are inflating prices due to added COVID expenses.

I like that idea of using credit cards to just buy time during an emergency while you get the cash you need. It might not be perfect but it gives you a little more room to keep you money working while still having a plan if a problem comes up.

I haven’t noticed much on increased prices here with the exception of COVID protection items. Disinfectant wipes for instance are higher than normal. However, I think that’s still just due to a lack of supply right now. The good news is that there really hasn’t been any gouging or big shortages here.

Good you reviewed your finances and feel better about where to draw funds.

I’ve found that our passive income is much much higher this year than anticipated. So we are good to go. We also have excess cash, which actually feels great. I don’t think I can do the bucketing strategy. I just spend my passive income as it comes in or not.

What a bull market!

Sam

That’s a great place to be, Sam! Perhaps one day we’ll be pulling in a lot more passive income as well, but for now, we just make do with what we’ve got. And you’re not kidding about this bull market – it’s crazy that we’re still on this ride!

Whoa big spender! Hehe, seems like you had a heck of a good time on the road trip!

It’s probably not a huge deal with $1.3 million however. Car purchases are large irregular purchases that throw things off.

Cash flows, even with a larger portfolio can be pretty “uneven” at times. Boom or bust as it were.

I just try to keep around *at least* enough cash/short term balance to last through the lean times. The Great Recession was a good example; dividends were cut, rental vacancies rose, and so forth.

This plan has worked out OK so far for our family. Hopefully it will continue. We’ll see if we make it through the pandemic of 2020-2021. 🙂

Yeah, I do like keeping a buffer in place – now I just need to be a little pickier about trying to make every penny of that money work even harder. That’s what really helped put us up this creek for the year.

I also have a good feeling the Tako family will be just fine with your plan throughout this pandemic. 😉

Hi Jim,

I think that you will be well set for life with your net worth. This is regardless of whether you intend to earn some form of active income through this blog or other side hustle. The main gist is to consider reducing the expense further when you see that the cash cushion is diminishing before the year’s budget allocation. This requires the flexibility which will be handy in this aspect.

WTK

That’s what I’m counting on, WTK – fingers crossed! 🙂 I think next year we should be in much better shape to help build up a better buffer to help us over the long haul.

A huge part of what has helped me is setting ‘artificial’ barriers that help me feel like I have less than I actually have. If you never feel strapped for cash, it is easy to let it slip away! This is an important part of the process whether you are accumulating or living on assets, and I appreciate your story.

Great article!

Thanks, Jay – very smart thought. We actually do that as well but this year got a little… messy. 🙂

Part of the problem was that we also had to kick in money to cover our duplex over this year because of a bad tenant. However, as of this morning, I just received almost $5k in my bank account from the county as part of the CARES program for the tenant. That just solved this year’s problem 100%!

Nice to have a cash buffer to avoid sequence of risk problems. While bonds and cash during the next few years will generate very little interest, it’s important to have enough so as not to have to sell stocks into a down market.The trick is determining the correct number of years to hedge against the risk.

So true. We keep more than we probably should outside of stocks – about 5 years’ worth of living expenses. Although that might be excessive, it helps us to sleep better at night so it’s worth the growth we’ll likely miss out on.

$1.3 million is a decent amount for retirement. But of course it has to last and that is probably why you feel that you are just getting by.

That’s true, but that’s not my problem here. The issue is that this year was an oddball because of and in spite of the pandemic… we put aside $15k from this year’s living expenses in a CD, unexpectedly bought a car, went on a monster road trip, and had tenants that didn’t pay rent for about 8 months (that we couldn’t evict because of COVID laws). This was all due to a once-a-century pandemic. Regardless, we’re actually in a great position financially and we’re already looking to be able to put aside a solid chunk of excess money next year.

I retired at 54 last year with 1.4 million and I was originally dead set on doing an approximate 3.5% annual withdrawal out of my IRA via SEPP 72t however I’ve come to embrace the 2 bucket method instead with about 200k in a bank money market. For me that’s at least 5 years because I’m planning on pulling 35k per year. It may surprise some early retiree’s on how much we spend towards job related activity’s including gas, car maintenance, lunches, cloths, etc. Which ever withdrawal rate you use, the younger you are when pulling ER, the lower it should be in my opinion. With record low bond yields and Vanguard’s projected 4-5% growth over the next 10 years in a 60/40, I’m way more comfortable only pulling 2.5% – 3% off my total net. Some say a 5% annual withdrawal is acceptable however I cannot agree.

I hear you on the low growth projections over the upcoming years, Bruce. I’d be extremely nervous about doing a 5% withdrawal as well. Your 2.5-3% seems like it’ll be about as close to bulletproof as you can get – much easier to sleep at night with such a low withdrawal rate. Right now, I don’t think I can go that low, but I’m comfortable with adjusting as needed and hopefully bringing in a little income along the way.

Thanks Jim. I am a fan of Josh Scandlen at Heritage Wealth and his YouTube channel on a lot of his topics except two in particular. This one where he pushes a 5% withdrawal and the other “You don’t need one million or more to retire and can do it on less the $500k”. I get the feeling that his channel was crafted to garner a higher volume of viewers through this message however as he is a CFP, I feel this is inherently dangerous information. Why would you want your clients to ride the edge all the time? That’s why most CFP’s give a higher number to shoot for so retires don have to be ridding the edge all the time. It’s not because they are being mean and want you to suffer through more years of work. He did however make me come around to the 2 bucket retirement over doing straight yearly SEPP 72t withdrawals so he does offer tons of good advise.

I hear ya. I believe there’s got to be balance… make the withdrawal rate too high and you might run out of money. Make it too low and you could be working forever. Sounds like you’re in a good position – best of luck to you!