Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

Everyone likes a secret, but a secret formula? Even better!

Now that we’re only a few months out from me quitting my job, we’re starting to share the news more with friends and family.

A lot of them seem to be a little confused, but then we talk about our planned move to Panama and it takes most folks to a level beyond comprehension.

Eventually, though, we tend to get past that initial shock. And then the “bold” ones out there muster up the courage to ask some questions.

But most importantly, they want to know how we did it…

What’s the secret formula for reaching financial independence?

I think it’s a fair question.

After all, people as a whole tend to struggle financially. A lot of folks in this country will find it painfully difficult to reach traditional retirement.

Some may never retire at all.

It’s a sad state this country is in. Here are some numbers to ponder…

- 21% of Americans don’t have ANY retirement savings… that’s right $0!*

- 33% of Baby Boomers have $25,000 or less in retirement savings*

- 2/3 of Americans aren’t putting anything into their 401(k) plans… a big fat zero!†

- The majority of Americans don’t have enough in their savings to cover even a $1,000 emergency‡

We could go through statistics like this all day, but the point is that the financial direction of many people isn’t leading them into a great future.

And then to hear that someone is retiring at 43? That easily raises some eyebrows and curiosity.

So I thought I’d take the time to explain the secret formula to reaching financial independence. This is such an important post packed with so much material that it even earned its own table of contents!

The Secret Formula to Reach Financial Independence

Get ready to take some notes on this simple, yet secret formula!

Ready for it? Ok, here goes…

There’s really no secret formula!

That’s right – no secret formula at all to reaching FI. Disappointing, right?

So that’s the bad news.

But the good news is that it’s still possible to reach financial independence regardless.

And the even better news is that it really comes down to the things all of us already know. The key is not that you just recognize the path though, but that you actually implement these steps.

So let’s go through what I think the recipe for success is that many of those who reach financial independence follow (including myself!).

The Roadmap to Financial Independence

Notice how we’re calling this a roadmap to financial independence (FI) and not FIRE (financial independence / retire early). The reason is that you don’t have to retire early if you don’t want to.

If you enjoy what you do and want to work forever, go for it. But whether or not you want to work for the rest of your life, you should strive to reach financial independence. This is what gives you the power and control to do what you want in life.

At some point, you’re going to have to retire – like it or not, eventually, your mind or body is going to go downhill. Put yourself in a position that you can decide when you quit working.

With that said, here are what I consider the most solid way to make this happen…

1) Get out of debt

With the possible exception of your mortgage, you need to get this albatross off from around your neck.

Debt kills. That should really be a public service announcement.

Having debt actually hurts you twice…

- It’s painful to get out of debt and costs you a ton of extra money every month.

- But it also prevents you from saving and investing that money each month.

And that second one’s the real killer! You’re missing out on time and compound interest because of your debt.

I’m speaking from experience. I struggled with this mess in my early to mid-twenties with around $30k of credit card debt alone. But once I took control, buckled down, and got rid of it over a few years, it was so freeing… and that’s when my savings and investment accounts really started to grow.

If you can’t get rid of debt (again, with the exception of maybe your mortgage), it will be almost impossible for you to reach financial independence.

Make eliminating consumer debt, student loans, medical debt, etc. your biggest financial priority. There might not be a secret formula, but the sooner you get in the black, the better off you will be.

Your financial future depends on this step more than anything else.

2) Know where you are now and where you need to be

So you’re on the positive side and ready to move forward, right? Time to figure out exactly where you are currently and where you want to be.

Where you are now

The first part of this involves tracking your expenses and knowing your net worth. Find out where your money’s actually going so you know how to move forward.

Notice I’m not talking about budgeting. I don’t budget and never have. If it works for you though, stay with it. That’s one of the best money tools for a lot of folks – it’s just not for me.

What I am talking about though is tracking your expenses. This is what helps you determine which areas you’re spending too much money. And by figuring that out, you can trim some of that fat so you could put that money to better use (i.e. saving and investing!).

The other benefit of tracking your expenses is that you’ll learn how much money you’re actually spending per week, month, or year. You need this information so you can determine how much money you’ll need to reach financial independence, which we’ll talk about shortly.

Personally, I use Quicken for managing my finances. I’ve been using it since 1999 so it carries my entire financial history and I’m completely ingrained in it.

Quicken’s been around forever, and it probably packs more capability than most options out there, but you also need to pay for the software (now a subscription). I personally think it’s worth the money because it’s paid for itself many times over for me. It’s the catalyst that helped me get out of debt and it’s been the financial tool I needed to feel in control.

It’s far from the only choice out there though. Here are a few great options that are extremely popular, work well, and are free to use:

- Empower (formerly Personal Capital) – I mention Empower (formerly Personal Capital) first because it also provides some of the best functionality to track your investments (more on this later). The phone app is awesome as well!

- Mint – Intuit sold Quicken so they could concentrate on Mint. It’s probably one of the most popular services for tracking your finances.

- Spreadsheets – Some folks love their spreadsheets and can do some amazing things with them. I don’t like the manual option, but go for it if it works for you!

What’s important is that you figure out where your money is going and what your net worth is. Your net worth is basically the sum of all your assets (the value of all your savings and investment accounts, your house, cars, etc.) minus all your liabilities (your debt).

How much money you make is really irrelevant if you’re spending most or all of it.

Your net worth though is the key. That one number tells you how much money you have stashed away for your future.

Where you need to be

This is the part where you determine your future plans. For some, that might be to have just enough money to cover your current expenses year-after-year. For others, it might be an opportunity to save enough to live out your wildest dreams. Because of that, where you need to be is going to be different for each of us.

However, a great place to start is to look at financial independence in general. And a good first step in figuring out this number is to use the 4% rule as a starting point.

In a nutshell, the 4% rule is based on a historical study that showed that if you have an investment portfolio and withdraw 4% of it each year (adjusted for inflation), you’ll almost always succeed in not running out of money over a 30-year period. In fact, in many cases, you may end up with more money than you started with.

Nevertheless, remember that while 30 years is probably a good number for traditional retirees to consider, early retirees could be living 40, 50, or maybe 60 years after they quit working.

There are other reasons to be careful relying wholeheartedly on this rule, but we’ll save that for another day. However, it’s definitely one of the best places to start when mapping out your financial future. This gives you a chance to put you in the ballpark of how big your portfolio needs to be for retirement.

And a simple way to work this out is to flip the rule on its head. In other words, if you multiply your expenses by 25, that will let you know where to start aiming to get your portfolio to a number that works with the 4% rule.

So if your expenses are $40,000/yr., a portfolio of $1,000,000 would satisfy that requirement ($40,000 x 25 = $1,000,000).

When you’re figuring out what your annual expenses will be, don’t forget that some will go up in retirement (i.e. healthcare) and some will hopefully go down (i.e. mortgage paid off?).

This simple formula can help you get a better projection of where you want to start aiming to reach financial independence.

3) Cut stupid expenses

Yeah, I said stupid expenses.

Look, you don’t have to be the most frugal person to reach FI. If you’re thinking the only way to reach financial independence is to flush your toilets once a day or that you need to live in a one-bedroom house even though you have a spouse and four kids, you’re mistaken.

Not all of the personal finance community is pinching every penny. You need to figure out what works for you so you’re not feeling deprived, but still not wasting money needlessly.

Personally, my wife and I tend to be a little more on the frugal side, but I think we’ve struck a balance we’re happy with. We do a lot of family trips and cruises, but we’re always meticulously hunting for the good deals on the flights and lodging. Additionally, we’re not spending money on a lot of souvenirs or other garbage on the trips. Besides that, we live in a nice house in a good development.

In our day-to-day lives though, we shop at Aldi for our groceries. We’ve been driving the same cars for almost ten years now (and will continue to do so!). We don’t eat out that often and when we do, it’s generally not at some overpriced restaurant.

But that’s just us. That’s what works in our family and we’re very happy with it.

Maybe the “secret formula” for you might be completely different. Perhaps you love to eat out (foodies!), but don’t care about vacations… that’s just fine with me!

Here’s the deal though – there are only two ways to accelerate your path to FI… cutting expenses and increasing your income.

I’m also going to guess that unless you’ve really dug into this already, you’re going to find a lot of waste in your spending. Many people struggle to live below their means – don’t be a part of that!

Focus on the big three first – housing, transportation, and food. These items could have the biggest impact on your path to financial independence.

What could you be doing to cut back on these costs? Here are a few ideas:

- Smaller or less-expensive home

- Live closer to work

- Ditch your expensive car payment and buy a used car

- Bike to work

- Eat out a little less

- Shop at a lower-cost grocery store

Feel free to pshaw some or all of these, but I bet you can find a way to easily save thousands of dollars a year with very little change to your lifestyle.

Then it’s time to look at some of the other expenses that might be a little less costly, but could still help bring your expenses down:

- Ditch the cable or cut back on the current package

- Change to a cheaper cell phone plan. I was a Verizon customer, switched to Total Wireless, dropped our bill in half, and saw absolutely no difference!

- Cut back or eliminate magazine subscriptions you don’t use

- Mow your own lawn instead of paying someone else to do it

We could go on forever, but I’m guessing you’ll find something that can help optimize your finances a little more.

4) Increase your income

The flip-side of cutting expenses… increasing your income. Nevertheless, here’s something to consider – you can only cut your expenses so far, but there is no cap on how much money you can make!

There are a ton of great ways to make this happen.

Stay the course

It could be as “simple” as staying at your job and asking for more money. Depending on the job or field you’re in, if you’re valuable enough, a raise might be something you can get without too much effort.

Perhaps it’s time to look at a competitor that pays a little more. Who knows – it’s possible your employer will match or beat the salary you’re being offered just to keep you!

Different is good

Then again – are you in a job that just doesn’t pay that well and never will? Is it time to consider moving into a field that does pay better… even if it means furthering your education to make that happen?

That’s something personal that you would have to decide. Would it pay off to spend the extra money on the education if necessary in order to have a stronger return later? How much longer would that take?

Then there’s the job itself – it can’t always be about the money. Do you love or hate your current job? Would you love or hate the field you’d be digging into? Only you can figure that one out!

A little fun on the side

If you’re content with what you’re currently doing, but still want to work your way toward FI a little faster, maybe it’s time to start looking at a side hustle.

And that’s where the fun begins! Remember when I said that there’s no limit to how much money you can make? Yeah, well, this is where it starts!

You can start a small business or do some moonlighting today. Then hopefully it’ll start to grow over time.

Here’s what’s cool – it’s possible that your side job grows to the point where it can replace your regular W-2 income. At that point, you can quit your job (if you want) and spend more time growing your side hustle into a major cash-flowing business!

Even cooler is that it’s up to you to decide what your side hustle will be. And, there’s nothing stopping you from having more than one.

In fact, I have three side hustles right now…

- ) Our real estate business – After we recently sold our single-family rental, that leaves us with just our duplex right now. However, when we move to Panama and figure out some of the nuances, we may consider picking up another property.

- ) My publishing company – I’ve written and published a couple of technical books over a number of years. I’ve learned a lot with these and think I can grow this out a little more. It’s tough though – it’s a time-consuming process and it can be hard to make a lot of money with this. I do plan to write 2-3 more books (finance, children’s, and humor) once I’m done with the 9-5 and have some more time for this.

- ) This blog! – This venture has been my favorite and most exciting side hustle. I started Route to Retire early with the intent to grow it slowly into something bigger over time. The hope was to build it into something stable by the time I quit my regular job. It’s already been beyond my expectations in every way possible and I’m loving every minute of it.

If that last one intrigued you, be careful. Blogging sounds like an easy job, but it’s really not. You’ve got to love it or you won’t last doing it. Most blogs don’t last a year and that’s because blogging needs to be considered a long-game strategy. It’s very rare for one to just take off and start spitting out tons of money.

However, if you think this is up your alley, here’s a page I wrote on creating your own blog. This site has started to make some money and this year’s looking to be even better. I truly believe I can bring this up to around $25k/yr. in the next 2-3 years, especially when I have time to start posting more next year.

5) Save… a lot

This might arguably be the second most important ingredient in the secret formula for reaching financial independence.

You can earn all the money you want from your regular job, side hustles, etc. But if you don’t save any of it, you’ve failed the mission.

And when you’re looking to reach FI, you need to be saving even more money. That’s right – I said it!

Most financial advisors will encourage you to save 10% of your income. That’s great, but that’s not going to get you to financial independence at an early age.

In fact, according to the Holy Grail post from Mr. Money Mustache titled “The Shockingly Simple Math Behind Early Retirement”, it would take you 51 working years to reach retirement saving 10% of your income! Not age 51, but 51 working years!

That’s not good enough for normal retirees and it’s truly not going to cut it if you want to reach early retirement.

My recommendation is to work your way to at least a 50% savings rate. That could get you to financial independence in 17 years. I think that’s a pretty reasonable amount of time for most folks.

We currently have about a 60% personal savings rate. This will obviously change soon once we retire at the end of this year, but that’s exactly the point. The more you save, the sooner you can call it quits if you want to.

Then there’s the most important piece of advice in the world of saving… in addition to saving a lot, start as early as you can.

They call it “the magic of compound interest” for a reason – it’s like sorcery! The more you can put away when you’re younger, the larger your nest egg will be when you’re ready for it.

The irony is that when you’re fresh out of school and would be best suited to start saving, that’s when you usually need the money the most… or think you do. Because of that, it generally seems harder to save. But make no mistake, if you can automate your savings when you’re young, you won’t look back regretting that decision later.

6) Invest intelligently

If you’re already saving a good amount, you’re doing well. Now it’s time to polish things up a little bit. It’s time to look at where you’re investing your money.

I’m not a financial advisor and I’m not here to tell you the specific funds to invest in. However, I will tell you that if you’re investing in the wrong funds, the fees could be eating away at, not only your potential gains but possibly some of your principal as well.

Keep it simple

The people out there that are smarter than me will tell you to focus on low-cost index funds. Jim Collins is one of those bright guys and wrote a phenomenal series of blog posts called the Stock Series. Read it. Don’t think twice about it. It’s simple to understand, yet truly eye-opening.

Be smart and invest simply. Focus on low-cost index funds to keep your fees low and follow the market. Don’t let the thought of beating the market deter you. Those that try to beat the market not only usually fail, but it generally also costs them an arm and a leg for that kick in the pants.

After that, don’t watch the market going up and down. It can drive you batty. Just leave everything alone and keep investing.

Don’t jump back and forth between selling and buying. You can’t time the market and those who try usually get burned.

Figure out an asset allocation you’re comfortable with and then rebalance your portfolio a couple of times a year. This will help you sell some stocks (or bonds) when they’re doing well and buy when they’re down. Buying low and selling high – the smartest thing you can do in the stock market and you’re basically automating the process!

I have a large portion of our non-401(k) holdings in VTSAX because of the Jim Collins series along with some further reading I did thereafter. That doesn’t mean that you should necessarily just follow suit, but understand that there are stock funds that will perform as well as the stock market with much lower fees than most of the managed funds out there.

Small percentages of fees can be costing you BIG TIME!

Where it gets fun is when you’re dealing with employer retirement plans like the trusty 401(k) plan or similar accounts. You generally only get a selection of funds to choose from in those plans.

If you’re like I was years ago, you just kind of looked them over and picked out the ones that sounded good. And with some of those funds, you could be getting charged some ridiculous fees… oops!

Fortunately, there are tools out there now that can help you decipher some of the stupid hidden fees out there. If you don’t have an account at Empower (formerly Personal Capital), please sign up with them before reading any further. You can thank me later.

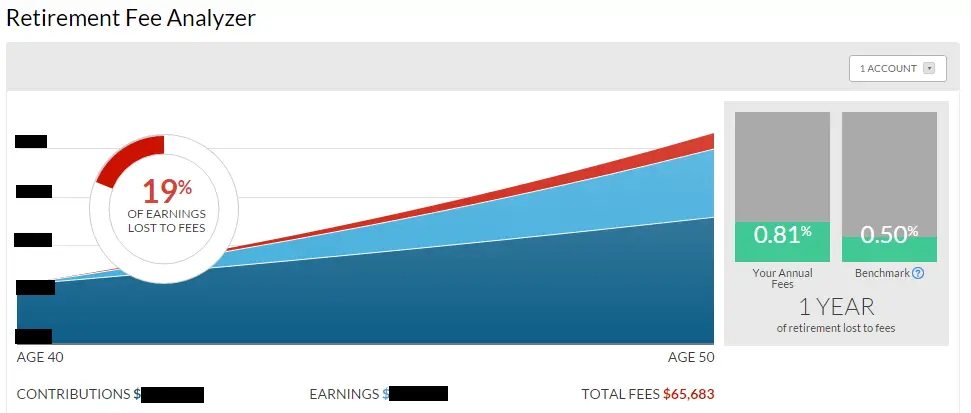

The Retirement Fee Analyzer in Empower (formerly Personal Capital) helped me to see very easily that I was looking at annual fees of 0.81%. That would come out to be $65,683 over a ten-year period!!!

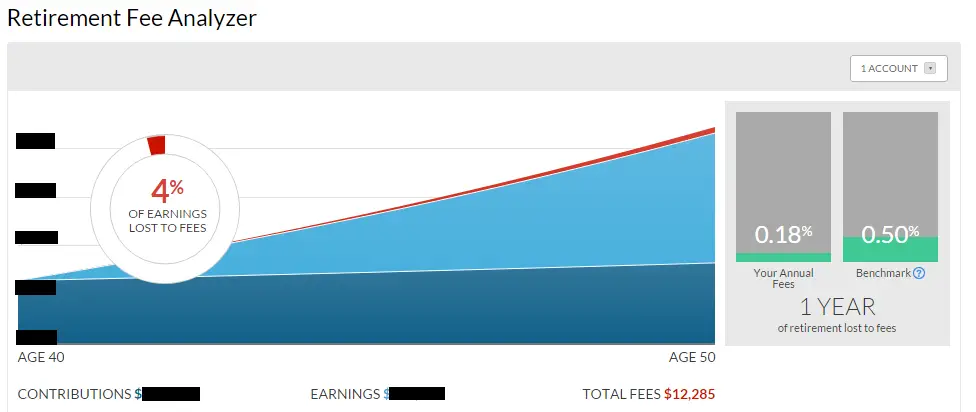

I was then able to log in to my 401(k) provider’s site and change the funds I was invested in. I put everything into the only Vanguard fund we had – a low-cost target-date retirement fund.

I then re-ran the analyzer at Empower (formerly Personal Capital) and this is what I got:

Uh, yeah – I dropped my fees down to 0.18% in my 401(k) and that brought my fees down to $12,285 over a ten-year period.

In other words, I saved over $50,000 in fees by making one simple change. If $50,000 means nothing to you, then you can skip this, but for most of us, this should be reason enough to evaluate your own accounts to see what kind of changes you can make to optimize your account.

Keep your investing simple and dodge the high fees. This is how you invest intelligently.

But wait… there’s more!

Most folks will probably be more comfortable sticking with the stock market, but it would be wrong not to mention some of the other options out there.

I want to be careful taking you down the wrong path, so I’m not going to go too in-depth here, but know that there can be some alternatives to investigate. These other investments can nicely complement or in some places replace a stock portfolio.

Real estate is probably the most well-known with rental property being a good long-term play. Like I mentioned earlier, we’re down to one duplex that is cash-flowing very nicely for us.

However, the first house we bought didn’t end up exactly the way we wanted. It wasn’t all bad, but we definitely got lucky.

The problem is I jumped into this without enough knowledge. I understood the idea well enough but didn’t know all the details. It’s important to understand how to evaluate properties and calculate the numbers before just jumping in.

BiggerPockets is a great resource on real estate to get started learning – the forums, podcasts, and webinars are free and can get you on track.

If real estate is important to your portfolio, but you don’t want to own physical property, real estate investment trusts (REITs) offer a good alternative.

In addition to real estate, buying or building businesses can also be some smart investments. Then there are options like peer-to-peer lending and buying precious metals like gold and silver.

Again, I don’t want to go too deep into these, but it’s important to know that the stock market isn’t your only investment option. Including some of these investments in your portfolio can help to hedge against the ups and downs of the stock market.

7) Continue learning

I get it – not everyone’s excited about personal finance. That’s truly Ok. You don’t need to know everything about personal finance to succeed.

When I got rolling on this journey, I was making a decent income and was able to get rid of my debt. Then I just started saving money and cutting expenses.

I knew where we were financially (thank you, Quicken!), but I didn’t know where we needed to be. I also wasn’t a smart investor and just bought stocks I thought were good and random funds in my 401(k).

However, as my journey continued, I started to learn more. And being a part of this community helped on levels I never dreamed.

Looking back, it’s easy to see that the more you comprehend financially, the further ahead you’ll likely be.

It’s hard not to come out ahead as you continue to learn. Here are just a few examples I’ve had:

- Understanding actively managed funds with high fees versus low-cost index funds investing made a big impact in our portfolio.

- Realizing that small percentages of fee differences have on different mutual funds in my 401(k) helped us save over $50k easy (thanks, Empower (formerly Personal Capital)!).

- Learning how to understand the numbers when investing in rental properties has made all the difference in our duplex versus our first rental house (thanks, Bigger Pockets!).

- The realization that you don’t need to be rich to be financially independent was a huge revelation and what is allowing me to retire at 43 years-old.

- Comprehending the tax implications of the different investment accounts has given us the ability to develop a better strategy in our retirement plans.

- Grasping the relevance of travel rewards hacking is setting us up to be able to travel back and forth from Panama several times for free. It’s also paying for our Global Entry/TSA PreCheck passes!

Could learning alone be the secret formula for financial independence? It truly could be.

I don’t know everything about personal finance (far from it!), but the more I learn, the further ahead we get.

You don’t need to be a personal finance expert to succeed, but you’ll get there faster if you continue to learn what you can about the subject.

Like to read? Check out “The Automatic Millionaire,” “The Millionaire Next Door,” “The Richest Man in Babylon,” “The Simple Path to Wealth,” “The Bogleheads’ Guide to Investing,” and “Rich Dad’s Cashflow Quadrant.”

Prefer to listen to podcasts? You can’t go wrong with Choose FI, Afford Anything, The Mad Fientist, Bigger Pockets, or Radical Personal Finance.

Too much? Start simple – subscribe to a couple of personal finance blogs… like mine of course! And I’d highly recommend signing up for the Rockstar Finance email list – one email a day with links to the best personal finance articles the net has to offer!

8) Don’t forget about today

This sounds like the simplest step, but for me was one of the hardest.

When I started down this path, I was already pretty frugal as a result of the debt I was in decades ago. However, once I found out that FIRE was actually a possibility for most people who have the drive and understanding, things really got rolling.

I worked to increase our income, but I spread things out too much and it started to cut into way too much family time… not good for any family!

I cut every expense I could come up with. I was scraping every penny I could to the point that I was overdrawing my checking account almost every couple of weeks.

The good news is that I was overdrawing it because I was saving and investing too much (how’s that for weird?!). The bad news is that every purchase Mrs. R2R would make me cringe (and she’s almost as cheap as I am!).

Then things changed on a dime. I credit that epiphany to Paula Pant (check out Paula Pant Kicked Me Where It Hurts). She made me understand something that might be the most critical part of this entire post:

You can’t trade today’s happiness for tomorrow’s.

It’s not worth it. What’s the point of saving and investing so much today that you’re not enjoying yourself? It’s entirely possible to be stuck in this cycle and then get hit by a bus right before you retire. Um, that would suck, right?

You’ve got to find a balance between paving a solid path for your future without forgetting about today.

What really helped me to get it was David Bach’s book, “The Automatic Millionaire.” We had already automated our savings and investing years ago, but this gave me a realization of this fact.

So, with everything in place already, why was I watching every nickel? We’re paying ourselves first already and not touching that money, so whatever’s leftover in our checking accounts should be for two things: our bills and having fun.

I’m definitely not perfect on this, but I’ve loosened up the reins and I’m comfortable with it. I want to enjoy the time with my family and do fun things with them and that’s exactly what we’re doing!

Enjoy today while you work your way to tomorrow!

So there you have it. It’s not a secret formula, but hopefully, you’re already on the track to implement everything in it.

I firmly believe that anyone can reach financial independence by wanting it bad enough and understanding the plan I’ve laid out.

Where are you on the path to financial independence? Would you agree that following this roadmap can get you there?

Thanks for reading!!

— Jim

Great job on this post. Maybe you can convert it to a mini ebook or something to give away with an email sign up. This is pretty much everything you need to know about FI.

The secret is to save and invest consistently. It’s all in the execution phase.

The concept isn’t that hard. Nice job!

Thanks, Joe – that’s a fantastic idea! I’ve actually been looking at coming up with ideas for an email sign up – that’s genius!

— Jim

I second Joe’s comment. I like what you wrote, but also that you included the holy grail links to the best FI article, books, podcasts, and investing strategy. If you do put this together as a book I would repeat all those links at the end and create one concise resource list.

Oh, absolutely – having a list of some resources to dig into further is one of the best ways to really get rolling toward FI. 🙂

— Jim

Awesome post! You really hit the nail on the head here. I think this would be a great introductory read for someone who is new to financial independence. Keep up the good work.

Thanks, Keli – much appreciated!

— Jim

This is just an excellent rundown of the path to FI. It is a well thought out framework for anyone getting started down this road. I think your last point is one some people forget about too. The goal is not to live a life of complete deprivation until you reach your goal but to optimize your life in such a way that you can enjoy your whole life to the fullest.

Thanks so much! And, yeah, that last one is something I didn’t have for a few years and it definitely made my path to FI more of a struggle.

— Jim

This statement is untrue (sounds like from a blog selling cards i.e. MMS): “Grasping the relevance of travel rewards hacking is setting us up to be able to travel back and forth from Panama several times for free”

We’re still newer to travel rewards, so I’ll bite – what’s your viewpoint on why this wouldn’t be correct? We just started down this road at the beginning of the year and we’re on track to have around 400k miles accrued by the end of the year. That alone will translate into more than a dozen round-trip flights between the U.S. and Panama. With the three of us, that’s four trips we’ll be able to make as a family for the cost of nothing except being methodical in how we use our credit cards.

I’m not sure if you’re new to this idea or not, but if so, dig into the Travel Rewards section of the ChooseFI. That’s what opened up my eyes to understanding how easy this is and helped point me in the right direction.

— Jim

What a great post and one that I can point FIRE newbies to. Bravo Jim, bravo!

Thanks you very much, Mrs. WoW – much appreciated!

— Jim

Informative article for every FIRE beginners or newbies. Great formula. Thanks for sharing such an valuable article.

Appreciate it – thanks, Lukas!

— Jim

Great post. Going to link to it on my blog as a great starting point!

Thanks, Mr. 39 months! Very much appreciated!!

— Jim

Great roadmap. My wife and I are FI, and I have recently taken up blogging as well. Just hope everyone pursuing this realizes that we also need to give back to others and donate also, whether that be time or money. Don’t want to lose sight of that.

Wife and I also considering eventually moving abroad, but not Central America. We’re more likely considering somewhere in Asia.

Thanks for the great post!

I agree with the giving back part, Matt. Coincidentally, I have a post in my drafts that I’ve been working on to talk about exactly that!

That’s cool on the possible move to Asia – do you have any thoughts on where in the continent yet?

PS Good luck on the blog!!!