Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

I’m only 43 years old right now (Ok, fine – I’m pushing 44!). But this is still prime time to continue on with my career. If I were to keep working, I could build up an even bigger and more secure nest egg.

I’m only 43 years old right now (Ok, fine – I’m pushing 44!). But this is still prime time to continue on with my career. If I were to keep working, I could build up an even bigger and more secure nest egg.

So why don’t you do that? Why did you leave your job and retire early? Are you stupid or just lazy?

Haha, talk about cutting to the chase!

I actually love when others ask me questions about our plans because it gets the conversation going about financial independence.

Personally, I don’t feel like everyone needs to retire early from their jobs. If you enjoy what you do, more power to you. But I do feel that financial independence should be a goal for everyone.

Even if you love your job and don’t plan to ever leave, @#$% happens. Things change and you may decide later that you don’t want to work there any longer. Or maybe you get hurt and can’t do your job any longer. Whatever the reason, it’s important to get your finances in order now versus later.

Generally, the conversations with others about our early retirement go pretty well. Occasionally, the discussion becomes some motivation for others to do the same.

Sometimes, though, I can tell that the questions I get are a little condescending… as if I just did this on a whim without thinking it through. Although no one has outright asked me if I’m stupid or lazy, I can sometimes sense the judgment is there.

So let’s talk about why I decided not to keep working in my career…

Our net worth when I retired…

We should first start off by discussing our net worth. Although I was a little hesitant to share information like this years ago, I realized that it’s important to openly talk about it for a couple of reasons:

1) It can be motivational for others. We tend to treat discussing personal finance as taboo in society and, to be honest, I don’t understand why. The best way to know how to improve our finances is to learn from others – both from ways we should be doing things and ways we shouldn’t.

2) It helps put our financial status into perspective for readers of this site. It took me a good number of years to comprehend a couple of important points about money on this journey. The first is that being a FIRE Millionaire doesn’t mean you’re rich. And the second is that you don’t need to be rich to be financially independent. Understanding both of those points is fundamental in realizing that you don’t need to be Jeff Bezos or Warren Buffet to become free.

When I quit working at my job at the end of 2018, our net worth was $1,098,482.91 as of 1/1/19.

If you’re newer on the journey to FIRE (financial independence / retire early), that might seem like a nice chunk of money. And I’m definitely not implying that it’s not. For regular Joe’s like us to hit millionaire status should help you see that this is possible though.

However, a million bucks ain’t what it used to be. And to support a family of three??? Please.

But, that should be enough to support our current lifestyle over the years. And if it’s not, I’m not worried. If the #$%^ hits the fan and things really go awry, I can always fill the income gap with a part-time job somewhere.

Where we stand today…

As I write this, Empower (formerly Personal Capital) is telling me that our net worth is currently $1,206,217.

It actually went up. We now have more than $100k more in unrealized gains in our portfolio than we had when I stopped working at my job.

That’s not a big surprise considering how well the stock market performed the first quarter of this year.

And that’s with us drawing down on our stash for our expenses. Not only that, but we’ve had to front-load a number of our expenses in preparation for the second half of this year. For example, the place we’re staying at for the first month in Panama has already been paid for along with several other expenses.

Regardless, even though we’ve had a good run in the market, I still find that amazing.

But that’s the whole point of the 4% rule. Our portfolio may sometimes go up and sometimes go down. Decades from now, when all is said and done, there’s actually a good possibility that our portfolio will be bigger than it is now… that’s hard for me to appreciate sometimes.

On the other hand, if we didn’t change or adjust our spending habits along the way as needed, there’s also a small possibility that we run out of money… ouch.

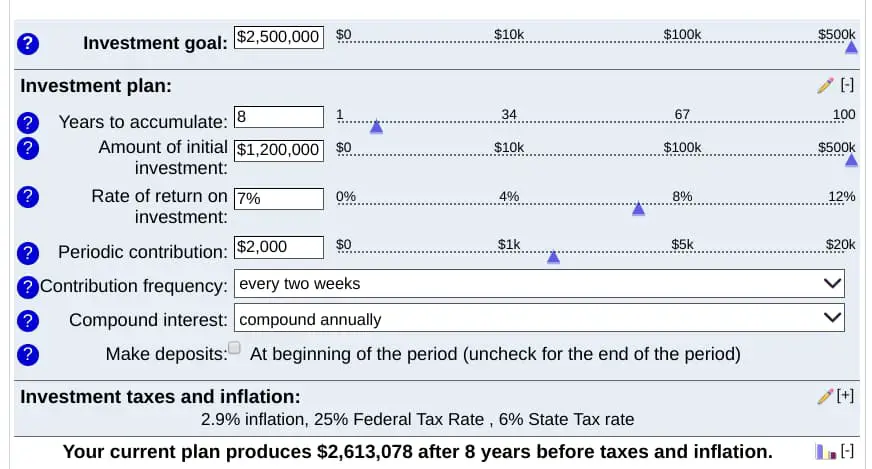

How long would I have to keep working to hit FatFIRE?

If I were to keep working, I could easily pad our stash to ensure that I wouldn’t be forced to pick up a side job… ever. Instead of rolling with the 4 percent rule of thumb, I could build us up to a point where we might be able to only have to take out 3-3.5% of our money annually. That’s much safer.

Or, if I would keep working, I could take us to the next level. We could have gone from FIRE to the even more exciting… FatFIRE!

That would mean our indulgences could go up big time! We could go out to dinner every day and take cruises several times a year (we love our cruises!). We’d be able to give our daughter nothing but the best from start to finish!

That’d be pretty sweet, right?!

The only cost would be that I would just have to keep working a little longer.

We’ve budgeted in to afford expenses of a little more than $50k per year using our different investments (including rental property). However, even with this being a bigger year because of the big move and everything involved, I’m anticipating that we’ll spend significantly less.

But let’s just say that we wanted to be able to afford $100,000/year in expenses. We could live like royalty on that!

According to the 4% rule, we’d need to have a portfolio of $2,500,000. That leaves us with about $1,300,00 shortfall. That sounds crazy far at first.

But using a retirement calculator and a conservative personal savings rate (at least for us), we can ballpark it out. If I were to keep working for another eight years, we’d nail the goal and then some…

Eight years.

So why not keep working?

Funny enough, that last sentence answered it all. Eight years. That might not seem like a lot of time over a lifetime, but it really is. That’s a lot of time sucked away and for what?

Although sometimes it’s hard for a lot of folks to understand, we don’t need more money. We have enough.

In other words, I don’t consider us rich, but we have enough that we can afford all our regular expenses without straining. And that’s with living a comfortable lifestyle, too – enjoying occasional dinners out, wonderful vacations and cruises, and not really wanting for anything.

So are we safe with what we have? Hopefully.

But here’s the thing – it would take a lot for things to go south for us for it not to work:

- The stock market would have to really hit the toilet over the next 5-10 years. That’s generally brought on by some fun called sequence of returns risk. And although that can happen, we’re mitigating that by keeping about 5-6 years of expenses in cash (see our net worth breakdown).

- If things got really bad, that would have to mean that we don’t adjust our spending accordingly. What the @#$%?! Of course, we’d spend less if our money was depleting faster than our portfolio allowed! That would be crazy not to!

- We’d have to never see another dime from ventures we haven’t built into the plan. But, I really can’t imagine that – I’m still a young man (keep your wise-cracks to yourselves, Millenials and Gen Z’ers!) 😉 I already plan to do some fun things along the way that will bring in at least some kind of income like writing a couple of books and continuing to build up this blog.

And if it all still went down the crapper, I’m truly Ok with getting a part-time job. Hell, I may even want to get a job at some point just to get out more. But I think we’re so much in the ballpark with what we have that I don’t anticipate this will ever become a necessity.

So, why not keep working and saving? There’s no need. Enough is the key in my life.

Unless you love what you’re doing, then at some point, you just need to pull the trigger and call it quits or change careers. There’s a lot more to life than being stuck in the rat race every day doing something you don’t enjoy.

We haven’t even started our next adventure of moving to Panama and I’m already loving every day of this newfound freedom. With just the small things in life like enjoying daily workouts, spending so much more unhindered time with my family, and getting a stress-free night of sleep daily, life has been wonderful. And my time writing posts for you guys is less rushed and more meaningful.

Freedom to decide each of your days is incredible.

So for me, the question really isn’t “why not keep working and saving”, but rather “why would I ever want to keep working”?

Go ahead and hit me up and let me know whether or not you agree with my thoughts on stopping at enough or continuing to work for more.

Thanks for reading!!

— Jim

Hello Jim, I really enjoy your posts. I admire your courage to take on your new journey. No one can account for every possible future calamity, but you seem to have thought of pretty much everything, and a plan b and c if need be👍

We are retiring to Cleveland (no snickers please😉) and are considering rental property as an additional investment. Can you suggest what areas you think have upward rental potential (especially regarding taxes) and if you care to share your realtor?

In researching areas near hospital and universities the taxes seem burdensome. Maybe we’re not looking in the right suburb 🤔. I look forward to following your freedom adventures in Panama.

No snickers from me about Cleveland, Kathy! I think it’s a wonderful place to be – beautiful, plenty of things to do, and a low cost-of-living. As a freeze baby though, winter’s our big reason for leaving.

Our duplex is currently in Stow, which is a great area for rentals. Cuyahoga Falls is another nearby area which has some great neighborhoods as well. I like Class B rentals so that’s what I’m most familiar with. If you’re looking to be a little closer to Cleveland, here’s a great post from James Wise on grading the neighborhoods.

The agent I really like to work with is Jacob Coker from Keller Williams Chervenic Realty. He’s always been a straight-shooter and knows his stuff. When we would walk through homes, he would actually point out the negatives and how they could affect our experience with tenants and not just the positives – that was a great way to earn my loyalty! https://jacobcoker.yourkwagent.com/

— Jim

Hi! Love your posts. I really admire what you guys are doing! I left my job at the end of December because I pretty much hated it. We are FI but not Fat FI. I want to do something meaningful and purposeful in my life. I’m currently taking classes at the university just to see what I want to do next and I got a part time job earning next to nothing but I’m really enjoying it. It’s only about 10 hours a week and it makes me feel better that I’m bringing in at least grocery money! I worry about sequence of returns too and of course big medical bills in the future but life is too short to work at a job you hate just to pad the portfolio, just in case! Good luck in Panama!

That’s fantastic and you’re a great example the whole point. Just because you leave your job doesn’t mean you need to sit in a rocking chair doing nothing all day. You found something that’s bringing in some money and you’re enjoying what you’re doing. I think that’s wonderful!

Good luck to you as well!

— Jim

I agree 100%. If you don’t love your job, you should move on once you hit FI. You can find something better to do. Working on something you enjoy adds a huge amount to your life. It’s hard to quantify, but life is a lot better if work aligns with your value.

As for the 4% rule, I don’t trust it all that much. It’s best to be conservative if you’re young. I’m sure you’ll be just fine. 3-3.5% is much safer like you say. You just have to be flexible.

Yeah, I don’t want to put all our faith in the 4% rule, but I really don’t think we’ll need to. I have a good feeling that between us being flexible and the start of other income coming in, we’ll be just fine. Much better than sitting in an office for the rest of my life! 😉

— Jim

I do disagree with you, Jim. 1M is not enough to retire for a possible 50 yr retirement.

1. 4% may not be a SWR for 50 yr retirement.

2. You can not anticipate your lifestyle changes/needs over 50 yrs.

3. Easy to underestimate medical costs. Besides illness or injuries, 70% need some type of long term care.

Addressing the points above

1. Have you review SWR studies for greater than 30 yrs retirement. Depending on asset allocation 3 or 3.25% SWR is recommended.

https://earlyretirementnow.com/2016/12/07/the-ultimate-guide-to-safe-withdrawal-rates-part-1-intro/

2. As you age you/wife need/want better comfort. Will be less and less ABLE to do things and need more help. This will increase expenses. Yes, this WILL happen to you as it does to all of us.

3. Now for the biggie. Medical costs. Unless you are blessed by dropping dead you/wife too will have medical expenses. Short term or long term care. 70% need some type of long term care. Assisted living, memory care, long term skill care. Which can be 10K/mo with 5% yearly INFLATION.

FatFIRED at 55. During retirement Injuries hit me, serious illness hit my younger brother. My medical costs got to 16k/mo for a yr. Now at 64 about 4k/mo. Had great insurance. Helped brother 10/k mo for 4 mo until he went on Medicaid, then 3k/mo until his death at 61. Your 1M does not EVEN take into consideration these costs. If I had FIRED at 1M would now be ONLY on social security and medicaid with nest egg spent vs 135K/yr, 4% SWR, 65/35 asset allocation with social security available to spend. I thank God over and over and over that I had not FIRED at 1M.

8 years additional working is a bargain! Find a different job if the one you left is toxic. The risk you are taking is TOO high for you and your family. Don’t count on being able to work part time to make up the difference.

My situation is not unique.

LeanFIRE retirees are SERIOUSLY underestimating these costs.

My best wishes for you and your family.

Thanks, Mel – appreciate your thoughts! As a little bit of a retort to your points, I’d like to throw out these thoughts…

1) I actually had the opportunity to meet Karsten (Big Ern) last year. He’s a great guy and he’s written some amazing content, particularly about the SWR. And I don’t disagree with his thoughts in the least.

However, I don’t anticipate that we’ll actually run off the 4% rule. We’ve used that as a basis for our plans, but between the flexibility of our plans and other income that we’re all but guaranteed to bring in through other sources along the way, I would anticipate we’ll actually have a much lower SWR.

2) Funny enough, I’m going to guess that our personal needs will likely decrease in a lot of areas of our lives as we age. We’re planning on doing a lot of adventurous fun things over the next several years that we’ve already accounted for. As we get older, I’d imagine those types of activities will start to subside.

On the flip-side, yes, we’ll probably incur some other costs to accommodate our old age. But we’re far from a needy family. We don’t need to spend a lot of money for comfort. And because we have the time now to get healthier and more fit, I’d also bet we’ll be in much better shape for our future than we would otherwise.

3) Can’t argue on the cost of healthcare. But don’t forget, we’re moving to Panama in the next couple of months. That basically nullifies any healthcare costs. The costs without insurance are next to nothing and the quality is very good to excellent… the way it should be here.

The only piece of the healthcare puzzle that could screw us up would be if we decide to move back to the States sometime down the line. And that’s possible. But know that we wouldn’t just move back on a whim without a plan. If the numbers don’t add up at that time, we’d make a different decision – maybe move to a different country instead.

And then there are the health aspects I mentioned before. The fact that I no longer sit behind a desk all day and get outside every day and walk, work out, and removed a huge area of stress from my life is huge! That will more than likely cut out a number of potential health problems in the future in and of itself.

Also, I don’t consider us part of the LeanFIRE group. That consists of folks who cut their expenses to try to reach FIRE sooner. I actually agree that that has the potential to be dangerous because you’re now trapped with these tight expense restraints after leaving your job. That can only work for a select number of people and to each his or her own.

We’re different than that though. Just because our expenses are lower than what you might think you need to spend, our numbers are the norm for us. We aren’t living in a tiny home or eating Ramen noodles just to keep our expenses down. We live life the way we want and enjoy plenty of vacations and fun times like we always have. We really don’t want for anything. And lucky for us, that still costs us tremendously less than most folks.

Sure, @#$% happens, but I’m Ok re-evaluating our circumstances every year and making changes as needed before things have a chance to become really bad. Life will change every along the way and I’m absolutely aware of that. We’ll adjust accordingly if needed. Like I said, I’m not even opposed to a part-time job down the line – I might even want to be doing that just for something different. 🙂

I think it’s fantastic being FatFIRE put you in a good position to take care of your unexpected needs along the way and I’m also glad to hear you’re Ok.

Best wishes to you as well, Mel!

— Jim

I’m always amazed, given how much people over there worry about the cost of healthcare, that anyone retires early and stays in the U.S. There is a whole world out there with far better value for money, rich cultural experiences and good to great healthcare for close to nothing. Go find somewhere you like!

I’ve noticed here in the U.S. that sometimes there’s a feeling of superiority with things. It’s not really talked about, but a lot of folks who have never explored other countries think that things like the healthcare here are probably much better than you could receive elsewhere. It’s obviously not true, but I think that’s the big stumbling block for people.

— Jim

Love this post. Other than ‘are you stupid, or lazy’, I’ve also gotten assumptions that I was just going to live off my significant other.

I might be jumping to hasty conclusions here, but this reaction seems inherently biased against women. Why do people naturally think that when a women retires, it’s because they plan to live off their other halves? I know the whole spiel about gender roles, but I am a modern working professional and I have worked a good number of years. Can’t I retire on my own merit?

I love how brave you are with sharing your retirement amount. It’s something I have considered sharing too, but if I do that, it would make me more uncomfortable to share my blog with people I know.

Good luck with the move!

Thanks, Jamie and congrats on reaching FIRE! So far, sharing my numbers hasn’t caused a problem with friends or family, but most have only recently started reading it. Only time will tell on that one! 😉

— Jim

Yes indeed…

It drives me crazy as well to read about all these Fire (and all retirees in general) who retire in the USA to end up broke (or live in permanent anxiety) because of health care

Yes, in other first world countries (like Europe) healthcare is practically free

No, healthcare services in the USA are not good but generally bad/very bad

I don’t know that I would say that the healthcare itself in the US is bad, but the system is definitely broken. Between the costs which continue to rise and the complexity throughout it’s become pretty unsustainable to continue going the direction that it’s headed.

— Jim

I really love your CAN DO attitude, Jim.

But, ya, it is those “unexpected needs” along the way that will decimate your meager nest egg and it MAY be too late to make changes (meager for those circumstances that unfortunately are not a rarity)

Some people ARE lucky and escape such events, but the odds are against us. Seems like better safe than sorry if you can beef up your nest egg to address those circumstances, to do so. Why expose your family to such risks? Who knows you guys may be one of the lucky ones and it seems you are willing to try and beef up while in “retirement” which is a very good sign.

Don’t know how health care in Panama is for major illnesses. Only know people in England and recently three in New Zealand who felt they had great health care until they got cancer (which most of us will get). Do to the costs their health care systems offered limited care (I was surprised how limited it was. We got one US drug manufacture to offer for free a drug extending one friend’s life a year thru compassionate use). Fortunately, one was able to sell everything they owned, plus a gofund me and got life saving treatment in the USA. It was too late for another to raise the funds and the last friend who’s life was extended by the free drug is currently in USA for treatment. They were all told to go on hospice because no further treatment was available in their country. All were in their 40’s or 50’s.

I am assuming that as an American, if needed, you would be able to come back here under some type of insurance that will pay for treatment. Their costs ranged from 400k-1m. It was hard to watch one particular friend go thru this. Please check out before that possibility that there is a solution for your family in case of serious illness. Maybe your insurance broker or family doctor have info on that. It was shocking to me because these were common cancers.

My best wishes to your new adventures in Panama.

Thanks for the comment, Mel! I definitely appreciate it and do understand the concerns. We might have to agree to disagree though. I don’t feel like I’m exposing my family to risks, but more opportunities than anything. The only risk is more calculated as I believe I’ll be able to start bringing in more income through sources like this blog. In fact, hopefully in a couple of years, I can bring in enough that we won’t need to touch any of our other investments for our regular expenses.

I’m sorry to hear about your friends that were affected by cancer. It’s a terrible disease and it’s actually one that I dread regularly. You can be as healthy as an ox, but somehow still get some kind of cancer. If one of us were to be affected by a disease like that though, we do have a few options. If we’re still in Panama, I’m comfortable with the quality and costs of care there. However, we’ll still have our expat insurance in place which gives us the ability to get coverage in the U.S. or elsewhere in the world (up to a couple million dollars). No one can be prepared for that horrendous stumble in life, but I still feel we’d be more prepared than most.

— Jim

Thank you for this. This is something I have struggled with the past few years as we approach our investments being 25X our annual expenses and early retirement creeping upon me. I continue to think about how much more money I could accumulate, and whether or not I will actually be able to pull the trigger.

Reading this really settled my mind in that having enough, is ENOUGH. Stop striving for more, it really is in our human nature .

It’s not for everyone, but there’s got to be a point when you figure out how much enough really is. We all want the most security we can have in life, but if it’s costing you your life now, that can actually be hurting you in your future. If you have the flexibility to be able to adapt as needed, you should be just fine.

Good luck, PPN!

— Jim

I keep working because I still live in CA. Even 2 more years seems like a lifetime…

Being frugal is the key – but frugal is not the same as impoverished.

I use NewRetirement.com for planning. I get a kick out of the optimistic and pessimistic calculations for living to 94. We’ll be somewhere between $600k in debt or be worth $11+ Mil. Seems like there will be opportunities to make adjustments to our living plan within that range of outcomes.

Haha, those calculators can be really funny. I actually like the NewRetirement calculator, too! Unfortunately, none of them can predict how life will go for you. And that’s the whole point – if you’re willing to adapt along the way, you’ll have a much more likely chance of ending with that $11 mill instead of the debt! 🙂

— Jim

You retired early because you have a plan and you COULD!

I have seen numerous people retire and honestly, six months later most of those folks are a distant memory in the workplace. Don’t hang around for a legacy – make your own by retiring and enjoying life with your family!

PS – Offer still stands if you are hanging around the upper Texas Gulf Coast!

Thanks, Mr. r2e! And, believe me, if we’re planning to be near that area, I’ll definitely hit you up!

— Jim

Well I’m only a few years older than you so yes, I must be stupid. Or semi-stupid in my case since I’m only semi-FIRE’d.

So it’s settled. I’m semi-stupid 🙂

Haha, smart move going only semi-FIRE, Dave, or you’d be full stupid like me! 😛

— Jim

I recently read on a FIRE forum that the problem with working One More Year is that statistically, you’ll probably not live long enough to spend the extra money you earn beyond the 4% rule. As an engineer who hates waste, that really hit home for me. We are moving next month to retire early in Wyoming and the only reason I would continue freelancing is for extra fun money. Maybe an extra girls weekend with my best friend, maybe an RV upgrade down the line, maybe I’ll want to color my hair in a salon, who knows. I do know that all those extra wants don’t add up to needing to work full time ever again!

I love it – sounds like a great plan!!

— Jim

We’re in a similar boat of thought I reckon. And I am soon visiting Panama for the first time to check it out as a potential part time retirement place. Your thinking is spot on.

After 2.5 years of not working I am slowly being drawn back to my old corporate life. I actually miss the fun with the teams and the impact my work had sometimes. At age 37 now, I decided to go back to do some more corporate work and solidify my financial position even further more in line with your thinking to push for FatFIRE. It will give me and my family a little more peace I reckon, plus I do love to see the asset portfolio value and bank account going up rather than stagnate.

Also, I don’t really believe inflation numbers published by our governments these days. The real inflation value which i track for myself is higher. With sharemarkets expected to perform lower over the next decade and inflation being higher than portrayed the 4% guide needs to be adjusted for accordingly. That’s easily done though, any part time job is gonna handle that as you mentioned. I trialled this last year as a dive instructor and called it beer money job (and loved it).

All the best in Panama, looking forward to reading more about your new life!

Thanks, Financial Gladiator – it’s not work if you love what you’re doing! Good luck and maybe we’ll meet up in Panama one day!

— Jim

that’s right! why keep working? i think this is especially true given that you have a young daughter to watch develop and grow. we’re a kid-free household in our 50’s and found the goldilocks sweet spot for jobs. mine is pretty stress free with 5+ weeks off each year and mrs. me just landed a 20 hour a week gig that allows her to take off when i’m off for travel. we’re in about your budget area around 50k/year and we live in buffalo where that money goes plenty far. i see you’re in cleveland for now so i’ll bet it’s similar. winter might be the thing that gets us out of here eventually as we don’t have extended family here.

i enjoyed reading your investment breakdown too. i put my whole portfolio out there for public shaming/mockery but nobody takes the bait. we have a similar cash/fixed income proportion too. i’m glad you’re taking the plunge. enjoy panama…i’ll be following along.

Thanks, Freddy – if you enjoy what you do, it makes sense to keep at it, right?

Haha, I was a little anxious putting my portfolio out in the public eye, too, but I didn’t get beat up either. Maybe we’re actually doing things better than we thought we were! 😉

— Jim

You hit the nail on the head that you might not be *able* to work to full retirement age. Or at least might get hurt for a little while and need the money that being financially independent brings with it.

Unfortunately, I’m getting a late start so I won’t be hitting FI. Too many bills and too much spending thanks to my ex-husband. But I can strive to sock away as much as possible to forestall as many “What if?” scenarios running through my brain. Like, competition is heating up in my industry, so what if our small company were to go under or be sold? Well, I’ve done the math and as long as I keep the guest house rented, a part-time job (I have a disability, so a full-time job outside the house just isn’t realistic) should suffice. It’d be tight, but it’s nice to know that it’s doable. That may be as close as I get to FI, but it’s something.

That actually great, Abigail! Honestly, most folks aren’t going to hit FI and there’s nothing wrong with that. What you’re doing is awesome though – you’re getting to a position of building yourself an FU money pile (pardon the phrase!) for whatever comes along. Continuing to move forward with saving and having that buffer is incredible. Keep heading down that path!

— Jim

Freedom to define each of your days says it all! I absolutely loved what I did for my “Career” but I scarified a lot in 25 years. It was good and it got my to FI, but now I’d never turn away! I can now “do what ever I want, whenever I want”. Not many folks can say that. And I’m making good on it too!

I hear you on that! For those who love what they do, nothing wrong with reaching FI and continuing their careers. But for some of us, the freedom to decide what you want to do each day is so important. Glad to hear you’re making good on it – I hope to as well!

— Jim

Care to share how the 7% PA is achieved?

Hi Jag – the stock market has historically averaged a return of about 10% annually. Take out a conservative 3% for inflation and that leaves you with about a 7% return. https://www.nerdwallet.com/blog/investing/average-stock-market-return/

Obviously, this is debatable, but the point was to just keep it simple for illustrative purposes.

Hope that helps! Have a good weekend!

— Jim

Thanks for the article. I enjoyed reading. I am struggling this week to get a better understanding of how much is enough after being denied a promotion yet again. I’ll be honest, I’m having a tough time today remembering why I am still working.

Do you ever think of preparing a response for when people ask you what you do? I think that when I retire, I might tell people that I am a beekeeper or a private client wealth manager – even though I have only one beehive and my only client is myself.

I am looking forward to hearing about how things turn out in Panama

Sorry to hear about being denied the promotion, PMM – that’s a bummer for sure.

Haha, I like the private client wealth manager – sounds very professional! At first, I struggled with the “what do you do” question. But, I’ve noticed that people don’t seem to judge like I thought they would when I tell them I’m retired. In fact, it seems to open up some great conversations.

— Jim

Personally, I think the stupid people are the ones that keep working when they don’t need to. The sedentary lifestyle of sitting at a desk all day will kill you pretty quick… as well as stress.

Sure, anyone can pile up more money… but what are you going to do with it? Once you’re FI and can live a really good life with plenty of good food, travel, friends, and decent healthcare… um what more is there?

A bigger TV? A nicer car? Minor niceties. You can’t take any of it with you.

That said, I do think some of the LeanFIRE folks are cutting things a bit too lean for my tastes. We personally called ourselves financially independence once we hit a 3% withdrawal rate. Even then, I’m still pretty conservative with our spending because of the kids.

Like you, I definitely get the idea of “enough”, but I feel like it’s a bit of a struggle for a lot of people. Being able to pull the trigger and quit their jobs is generally not an easy decision for a number of people. I’m not one of those folks 🙂 but I do empathize.

Wait, a minute – you can’t take your TV with you when you go? What am I going to watch when I’m gone?! 😉

— Jim

I enjoyed reading this post, as well as all the comments.

I had a similar thought process. How much is enough? Why am I still getting up in the dark and going to work every day?

I’ve just made the decision to go part-time next year, rather than pull the pin altogether.

I have enough money saved in cash that I could live off until I reach the age to access my superannuation (retirement account), but I’m single and I like the thought of keeping some money coming in just in case unexpected things happen further down the line. I have no one but myself to rely on.

Luckily, I enjoy (most aspects of) teaching, so I’m hoping that having the extra 2 days a week for what I want to do will give me the “sweet spot” that Freddy Smidlap talked about in his comment.

That’s a great position to be in Frogdancer! Going part-time at a job you enjoy for the most part is definitely a win. You get to ease into the retirement side of things and still keep some additional money coming in in the meantime. I think that’s fantastic!

I didn’t really have that option – there wasn’t really a way to do my job part-time and I wasn’t enjoying it anymore. That made pulling the band-aid off a little rougher, but I still feel like we’re in a good position and can adapt as needed.

Congrats to you on the decision and good luck!!

— Jim