Disclosure: This post contains affiliate links and we may receive a referral fee (at no extra cost to you) if you sign up or purchase products or services mentioned. As an Amazon Associate, I earn from qualifying purchases.

The guiding principle of the Financial Independence / Retire Early (FIRE) movement is to get to the point in life where you have enough and don’t need more money to cover your expenses.

Once you pull that off, you’re golden. You’re now financially independent and never have to work another day in life again… if you don’t want to.

It sounds great, right?

And for someone that pulled it off at the age of 43 a couple of years ago, I can tell you that I love early retirement (though it does come with its own set of hurdles). Being able to spend so much time with my family is such a blessing in life.

Having enough money in our accounts to cover our regular expenses like a monthly paycheck makes life pretty simple, too. We don’t have to worry about the possibility of layoffs, being fired, traffic in the mornings, or even having to get up at a specific time each day.

It really does remove a lot of the stress out of life.

But after over 2½ years of early retirement, I gotta say it… we don’t need more money, but I want it. I’m glad we pulled the trigger when we did, but now it’s time to start thinking of some ways to bring in some more income.

Today, I’ll tell you why we don’t need more money, why I want more anyway, and how we’ll try to get there.

Why we don’t need more money…

Here’s the deal, if you’re unfamiliar, a lot of the FIRE community follows the idea of the 4% rule. In a nutshell, a study was done years ago that showed that you should be able to pull 4% per year (adjusted for inflation) out of an investment portfolio every year without running out of money over a 30-year time frame.

There are several caveats to this rule of thumb and there are plenty of arguments as to why you should make your withdrawal rate more or less. Regardless, it’s a great starting point in trying to determine how much money you’ll need to be financially free.

As we sought financial independence, I used the 4% rule as one piece of our retirement planning. But, in addition to our market investment portfolio, we also had rental properties in the mix, the last of which we just sold during this crazy hot market.

In general, though, our plan allowed us to have an annual spend of about $55k per year (adjusted annually for inflation). That said, I would prefer not to spend that much if possible. That’s especially true during the first 5-7 years or more, while the sequence of returns risk can be the most lethal.

The first few years of withdrawing from a portfolio can be the most critical. If you’re pulling money out during a bull market, you’re hopefully withdrawing mostly gains and dividends. If you’re pulling money out during a bear market though, you’re going to be withdrawing principal and that’s tough to rebuild when you’re not working.

Our investment drawdown plan considered this with a bucket strategy. Essentially, we have 1 year of cash-on-hand as well as a 5-year ladder of BulletShares fixed income ETFs. This is structured so that we don’t need to sell stock investments during a bear market to fund our lifestyle. Although it can hinder some growth, the peace of mind we gain from protecting our principal is worth it to us.

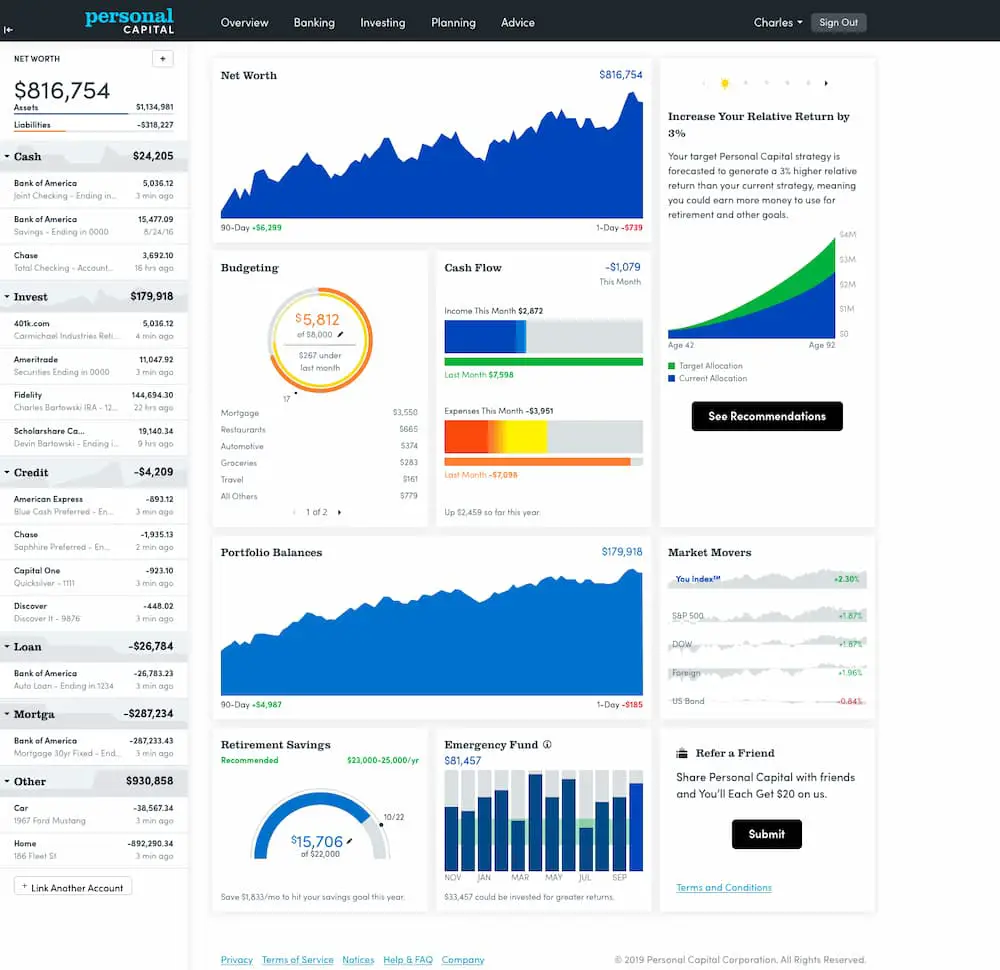

Fortunately, though, I happened to retire during a phenomenal bull run in the stock market. On the day I retired on 12/31/18, our net worth was $1,127,049. As of 08/01/21, it’s now $1,634,608.00… even after completely funding our expenses over the past few years!

You can see our net worth by month throughout the years on my Net Worth page. If you’re not tracking you’re own net worth, I strongly recommend that you do so. It’s the single best way to know how close you are to reaching financial independence.

One of the easiest ways to do this is to use Empower (formerly Personal Capital). It’s free and they beautifully do the heavy lifting for you. You link your accounts and it pulls together all your data for you. It also gives you some insights that would be hard to see otherwise. I saved $50k in fees over 10-years in an instant with the knowledge and tools they provide.

I’ve been using Empower (formerly Personal Capital) to help manage my investments for years now and I think it can be a huge benefit to you as well. Check it out and see what it can do for you!

So far, our plan has worked well. Our needs have been completely met by our investments. We’re living in a beautiful resort in Boquete, Panama. We have fun and can do some traveling as well. Most of the traveling lately has been back and forth to the U.S. a few times a year.

We continue to have new adventures like taking a bus from Costa Rica to Panama after a cruise we enjoyed. And last year, during the pandemic, we bought a Honda Pilot and took an awesome road trip across the U.S.

In other words, we don’t need more money to live a pretty nice lifestyle and have some fun… life is good, my friends!

Why do I want more money…

Sounds pretty good, Jim. Seems like you guys are living the dream… why do you need more money then?

Good question! Here’s the problem: we have enough, but we don’t have a huge surplus. Right now, I still need to keep a close eye on where our money goes and I don’t like that.

I’m not talking about a few dollars here and a few dollars there, but rather when we spend a little more on things. When we go to dinner with my brother and his wife in Texas, we can easily have a $200+ bill for the three of us (they like the fancy stuff more than we care about). That’s still a stab in the heart for me to waste that much on a meal.

Then there’s some of the travel we do. We try to find the best deals and use travel rewards as much as possible, but those are drying up while we’re living here in Panama. Flying internationally is not cheap. And lately, we’ve needed to throw in hotel stays along the way as well.

When we visit folks in the U.S., we spend a lot of money in small increments getting together with everyone. Whether it’s seeing friends at bars, restaurants, or even just their houses (bringing beer or food), it costs money. Not enough money that it would normally matter, but we end up doing this probably 20 times during our month-long visits… and that adds up!

I spend a little time then looking at our budget for the month and where we stand. And then I find myself asking Lisa “Ok, but how much will that cost?” way too often.

What I’m trying to say is that we have enough money to support our lifestyle but it has the potential to get cramped relatively quickly. And that’s something I don’t like.

We’re what most folks would constitute as “regular” FIRE since we aren’t cutting back on our lifestyle to live our lives. But adding in a lot of extra spending can muddy the waters somewhat. We have enough money for our normal lifestyle but doing a lot of things out of the norm for us can make me cringe a little.

We have a small cushion built in every year but I don’t like to see that eaten up. I would prefer to not spend as much of it, which would effectively bring down our withdrawal rate. That’s my safety blanket.

Put another way, it’s not that we can’t afford the extras but those extras can make it tight enough to make me a little anxious. Does that make sense?

It’s also a reason I have a hard time with folks on the far end of the spectrum chasing after Lean FIRE. Setting yourself up for a life of cutting back is unlikely to work well for most of us over the long haul. If it works for you, great. But the restrictions you could be placing on yourself can make life almost not worth living.

How we plan to get there…

Ok, right off the rip, it’s important to realize that our expenses aren’t as predictable right now as I’d like them to be.

The travel that we’re required to do as perpetual tourists back and forth out of Panama can swing dramatically. Sometimes it can cost a small amount with our travel rewards. But as we’ve been running out of those, the cost can easily be a couple thousand dollars or more.

Spending day after day out meeting friends and family each time we visit is also a cost that’s not very easily calculable. Those get-togethers can be anywhere from $25-$100 each time. One or two of these aren’t a big deal, but 20 of them on a visit adds up.

The good news is that those big expenses will go to the wayside once we move back to the U.S. next spring. That’s not to say that we won’t still have expenses that creep up, but most of them will be a little more controllable than they are now.

Once we’re back in the U.S., we’ll see some of our living expenses go up and some that will go down. I’ll talk more about this in a later post, but for the most part, we’ll likely see our cost of necessities actually be pretty similar to what they are now. Remember, we’re living a more “lavish” lifestyle than we plan to in the U.S. No more living in a resort once we’re back!

Here’s a photo I took a couple of days ago of the condos where we live right before the heavens opened up and dropped more rain than you could ever imagine!

Walking around in beautiful Valle Escondido where we live…

So that should be a wash, more or less. Funny enough, without all the bouncing back and forth all the time, our expenses may actually go down slightly when all is said and done.

Regardless, I’d still like to see more money in the coffers.

Lisa plans to get a part-time job once we get back and get situated. It won’t be a ton of money coming in but even a hundred bucks here and there can make a big difference.

I hope to continue to grow Route to Retire some more as well. Right now, I’m projecting to close out this year with around $5k in profit from ad revenue and from affiliate income for products and services I enjoy and share with you.

That’s the most I’ll have ever earned in a year since I started this site. If I did the hourly rate on this, it would probably make me cry, but it’s still nice to see something back for all the time I put in on it. Thanks, everyone, for your support!

Over time, I expect that income to continue to grow… slowly but surely. I can’t envision it ever being full-time money. However, while I enjoy doing it, it’s some nice supplemental income.

I don’t plan to go out and get a part-time job once we move back, but that could change over time, too. Faith will turn 12 right after we move back. The time she’s going to want to spend with dear-old-dad is inevitably going to diminish… such is life.

And Lisa and I have been together for over 20 years. She’s probably been ready for some time away from me for at least the last 18 years!

So I can see my free time growing soon and, well, we’ll see what happens then.

Gaining more free time could also be a good opportunity to spend more time on Route to Retire. Or maybe it could be a chance to write another book (I’ve written two computer books over the years). Writing a personal finance or children’s book (or a personal finance book for kids!) has been on my list to do.

As you can see, we’re not planning on going back to big-time careers anytime soon (read that as never!). But our supplemental income should continue to grow over the next few years. And that’s what I’d like to see – just a little more cushion in our yearly paycheck.

Should I have worked longer to save more? I’m going to have to say no to that. I needed to be done at the time… it was the right time for me mentally. And the supplementary income we’re working on should fill the gaps in nicely.

But if you’re planning to retire from your job and don’t hate what you’re doing, this is something to think about. If you don’t have a big cushion more than your anticipated spending in place, you may want to consider working a little longer to build that up. Don’t get stuck in one more year syndrome but be sure you’re comfortable with what you’re heading into freedom with if you don’t want to ever work again.

For us, it’s not that we need more money. However, having that extra income can help bring down our withdrawal rate a little more. It can also make it easier to plan more fun vacations down the road. Life is good and we want to continue enjoying every moment of it!

Plan well, take action, and live your best life!

Thanks for reading!!

— Jim

Hi Jim,

Great post as always.

We live in the UK and plan to retire at some point in the next 5 years. Just waiting for our kids to finish university, as we are helping them with the costs, such as rent. We have company pensions that we can access from 55, so plan to use them to help fund our retirement. What’s your situation with pensions and what age will they kick in? Are they already factored in to your income and spending in the years ahead?

All the best 🙂

Ian

Unfortunately, pensions are almost mythical creatures here in the U.S. anymore, Ian. With the exception of government jobs, pensions are pretty rare in the working world here. But boy, oh boy, that would be a wonderful addition to have!

That’s fantastic that you’re nearing the finish line in the next 5 years… and with a pension coming! Congrats and best of luck to you guys!

I’m glad almost everyone in the FI community is in such a privileged position and that there are different ways to do it. We’re planning on my husband retiring in 14 more years when he is 55 and the kids are out of college instead of trying to retire earlier. In the meantime, we’re doing some more lavish spending then we did win the kids are young.

Upping your spending with the kids grown up doesn’t surprise me much. It’s a different world once the kids are old enough to start their own lives. Now it becomes a great opportunity to explore your own newfound freedom. Have fun and enjoy!

I’m not sure bringing in some more money will provide the peace of mind you seem to be seeking. We’ve got a couple million more than we need to support our lifestyle and I’d be just as uneasy as you about spending $200 for a meal. I kept earning $100K a year for five years after I retired slightly early because it felt good to live completely on earned income and not the passive income from our index funds and bond funds. I quit earning money a few months ago and we are now doing life like you, but we are withdrawing less than 3% and in a handful of years we’ll start taking Social Security and our withdrawals will be less than 1%. It still feels unnatural to spend lavishly, its hard to change your style after being relatively frugal your entire life. It is nice having a larger cushion I guess but the fact is, it never feels big enough.

That’s really interesting to hear that perspective. It sounds like it’s possibly more of a mental hurdle rather than a money hurdle that knuckleheads like us have to get over. Perhaps I’ll still struggle with the spending, but a bigger cushion probably couldn’t hurt regardless. 🙂

Congrats on getting to the position you’re in financially, too… very impressive!

I retired unexpectedly almost 2 years ago (read that as laid off at 58). We relocated and bought a house last year, and have spent quite a bit on landscaping and floors. I keep expecting the monthly credit card bill to drop, but it has been very consistent through travels and home work. I think I have just developed a budget clock in my head and have self regulated spending. I’ve done some part time work but all earnings were used to fund Roth IRA contributions. My desire for more money is just defensive – trying to protect against inflation. Inflation is the only thing that will blow up my withdraw and bucket strategy. Recent headlines are not comforting..

The post-FIRE path is a strange sort of beast for many of us. All the numbers and all the math we can do can only put us speculatively into a comfort zone. Unless we have millions more than we could ever need or have strong pensions or everything in annuities, it’s really just hoping that our historical knowledge will suffice for the future. Will inflation take off and throw all our plans out the window? Possibly. Can the returns in the stock market not be as good as they’ve been historically in all the FIRE calculators? Sure.

And with that, it seems like it will always leave a little bit of uneasiness for wondering if we’re truly where we need to be. We probably are but that desire to have more money seems to be something based on that uncertainty. Maybe that’s a good thing though so we don’t just sit on our laurels just hoping for the best.

Just want to say I always enjoy your blog which I’ve been reading for several years. I’m retired but not an early retiree but somehow your blog is always interesting and enjoyable. Best to you,

Thanks, Howard – very much appreciated!! 🙂

It kind of sounds like you guys are going to transition to BaristaFire or something.

Have you thought of what you’ll do to earn that extra money? More blog posts? Start working full-time again? (Or part time?) Start a new business of some kind?

Some folks pick up part-time “fun” jobs to get rid of that “itch”. Others in that position side-hustle like mad. Which are you considering?

In a way, it might be similar to Barista FIRE in that the extra income would be nice to have. The difference is that I don’t think we really need the extra income. It’s just a way to help me feel a little better about having some cushion and lowering our withdrawal rate a little.

I don’t have any plans to go out and get a job anytime in the near future. I’m not opposed to having a job, it’s just not on my radar anytime soon. That could change down the line though… never say never right?

Lisa, however, plans to get a part-time job once we get back and get settled just because she wants to. It won’t be a lot of money coming in but it’ll be something. If she’s able to get health insurance that would be a real bonus though I don’t think she will based on what she’s planning to do.

In the meantime, I’m going to continue to slowly grow Route to Retire. I don’t want it to become a full-time job right now though so I’ll just keep on pace to grow it organically and market it a little more. While Faith’s doing schooling, that gives me a chance to write more posts as well.

I can understand what you are saying here. We are close to being FI in our late 40s, but we also have a 3 year old and I think a lot about wanting to show them a lot more of the world than I did. I want to ensure that we can do that and if that means I work a little longer to pad our retirement accounts so be it. I also believe that we are in the tail end (probably another 5 years max or so) of a secular bull market and the long-term bull will come to an end and we will go sideways for a long period of time (e.g. 1968-1981, 2000-09). Having some extra income and not having to rely on the drawdown just gives me a bit more piece of mind.

That’s cool, Jason – being able to show your 3 y/o more of the world is an awesome idea. I can say that “just” living in Panama for the past couple of years has helped our daughter to just see that there’s more to the world than just what you read about. It also helps to squash pre-conceived notions of other cultures as well.

And I’m with you on the stock market. That piece of mind is critical. It would be easy for us to just re-calculate our withdrawal rate based on our current net worth and enjoying the extra cash to spend. But I feel more comfortable sticking with what we started with and knowing that the sequence of returns risk is lessening for us every day (for the time being).

jim. you outline very well near the end why i choose to keep working for the time being. i think mrs. smidlap will pull the plug in a month or two from her part time job of the past few years. that’s all well and good but my present gig is pretty easy and does not ruin my life to spend 40 hours. plus, the air conditioning is great at work and we don’t have central air at home! seems like a good way to pad the accounts until something happens that ruins my work life.

you’ll make some money for sure. best of luck.

Haha, A/C wins out again!

No, I think that’s great, Freddy. If you have a job you enjoy (or don’t mind), no reason not to keep at it a little longer to build a bigger stash! And it leaves you in the position to be able to bail if you start hating it for whatever reason.

Of course, you never know… when Mrs. Smidlap stops working and tells you how much she loves it, you might be tempted to join her sooner than you planned! 😉

I’ve loved your blog for a few years and it’s inspirational to me to know FI money really can lead to a different life than the 8-5. Like it was for you at the end of your job, I find I’m grinding it out now. We’re about 5 years to lean FI, saving around 60% of our income. This family of 5 spends closer to $80k/year. We can spend that and still save 60% of our income so we are doing pretty well. With a 12, 10, and 6 year old, the kids have no interest taking a year to travel. I’d like nothing more than to leave my job for a bit, but the golden handcuffs have me locked in now, and when I could finally set sail, the kids won’t be at an age that they want to. So…likely I’ll keep working for another 10 to 11 years then decide I can jump ship. I’m 39 now. 50 is not bad I guess, but this guy hasn’t ever gone more than 2 weeks without work (that sounds like a complaint for the rich I know). My job now allows me to be home every night and run the kids to their various practices. I’m smack in the middle of the American dream I guess, but I’m not sure this dream really hits the nail on the head. I feel like I gotta get this “darn” money-accumulation problem behind me so I can go have fun.

Retiring at 50 is not bad at all, but a tough pill to swallow if you’re not enjoying your job. I was in a position where it would have been tough for me to switch jobs and get the same benefits I was getting at mine… that’s why I sucked it up and stayed until I retired. Are you in a similar position or are you able to find another job you enjoy more for the next 10-11 years? Even if it pays less and it takes a little longer to reach retirement, it might not matter if you find something you really like doing.

Best of luck, Steve… I’ve been there and I know it can be frustrating!

I’m in a similar position. I don’t like spending down at all. At this point in my life, I’d rather earn a bit to achieve parity. I’d be a lot more comfortable spending down when I’m in my 50s. That’s why I do several side hustles.

Maybe you can look for something similar. Uber or something like that so you can have a lot of autonomy. There are all sorts of app-based gigs now. I bet you can find something fun to do and you can write about it. 2 birds!

You’ve been doing outstanding on your side hustles, Joe! I love reading about how you’ve been doing with all of them.

I like some of the interesting things you’ve found like the Lime scooter charging. It’s different, gets you outside, you’re doing it on your schedule, and it actually looks a little fun (like when you get your son involved). I’d love to find something cool like that to do once we move back.

Since that won’t be until next summer, I’ll focus on growing the blog for that little extra in the meantime.

Thanks for the update…I kinda feel like Steve (above) grinding along at age 53. Have 3 sons, two out of the house and working (off my payroll). One still in high school with two more years to go. I must say a lot of bills come do with kids. We (my wife and I) paid for their college (tuition/room and board) and plan to for the last one. Over the years, I’ve had to pay for cars (include some crashes), braces for two outta three, car insurance, blown out knees, food, I recently needed two dental implants. I guess my point is that these life things add up and if I was not working I think I’d be FREAKING OUT. I save hard and have some long-shot investments (oil and a start up company that may go public) which I’m not counting on. I can certainly see where you are coming from with regard to asking the wife this and that about costs. I like the idea of part-time work and that’s my goal when the last kid graduates. I appreciate your honesty and really.

Yeah, life can come with a lot of unexpected costs, particularly with kids involved. Part-time work once your last kid graduates makes a lot of sense. For me, I felt the need to jump ship earlier because I wasn’t enjoying my job anymore in the least and I wanted to spend as much time with my daughter before she grows up (which has been wonderful!). Going back to work part-time later isn’t something I’m opposed to, but it’s not on my radar yet… we’ll see how that plays out over the years and if I’m able to grow this blog more.

They call it personal finance for a reason – it’s very personal and different for each of us. I’m happy with where we’re at and it sounds like you’re plan is going to make a lot of sense for your household as well. Best of luck! 🙂

Thanks for sharing!

I’m at $950K NW and thinking about quitting my job in Jan 2022. Wife would continue to work full-time until around 2025. Posts like this very informative and helpful. I find it hard to find the balance of not saving enough vs. wasting too much life, and how needs and wants will change in the future.

Best of luck on the move back to the U.S.!

Thanks, Juan! I try to be as honest as I can about the various aspects of early retirement and not just paint it as all rainbows and unicorns… though it’s mostly rainbows and unicorns! 😉 Finding the right balance can be the toughest hurdle both on the saving aspect and on living life before and after retirement. Needs and wants will constantly change so you just need to make the best-educated decisions you can and adapt as you go.

Best of luck!

As the FED normalizes interest rates to fight inflation, it is likely you will have the opportunity to generate increased income from your portfolio. If you are fortunate enough to get out of the stock market before it goes into the next bear market, your funds have the capacity to generate significant cash flow. SAY: $1.6 million in a federally insured CD ladder at 5% would bring in $80,000 a year. Timing is everything and so far your timing has been excellent. I’m interest to see how you navigate your portfolio in declining market conditions.

Thanks, David – yes, we’ve been very fortunate with our timing thus far. And you’re right that if we got out before the next bear market, we’d be in great shape. However, it’s also possible that the market could continue to grow for years to come and we’d miss out on that growth. The nice thing is that even if the market lost 40-50% right now (God forbid!), we’d still be in very good shape just because of how much growth we’ve had since I left my job.

And then, we have 1 year of living expenses in cash and 5 years in bond funds outside of the volatility. That buys us a number of years in which we could live without needing to sell any investments while the market’s struggling.

That said, that’s all in theory. I’m going to just keep doing asset allocation a couple of times of year (more during crazy, volatile times) and stay the course. If all goes well, great! If not, we’re more than willing to adapt. Even if I have to go out and get a part-time job, that’s not the end of the world… could even be fun to go back to a job versus a stressful career again. 🙂

Sounds like a great plan …. with FI comes so many options to add to the semi-retired mix … part time work, special projects, blogging, vlogging, online tutoring – international school teaching, working in a grocery store, starting an NGO, going back for more study, starting a business (Elon Musk ? 🙂 ) , real estate agent / house flipping, aiding charity groups etc etc ??? many ways to spice things up … I have been semi-retired here in Beijing for a short while now …. we will head back to Canada for my daughter’s schooling on … Lake Huron? then maybe later to Maple Ridge BC or Kelowna or Markham (Toronto ) etc … then maybe back to Beijing, Hong Kong or Germany ? once our daughter is in Uni … love your updates as you navigate your journey – remember a happy wife means a happy life 🙂 Grin! 🙂

You’re so right, Michael – the flexibility is so much greater with FI. I love that you’ve found so many cool things to do… it’s not just sipping piña coladas on the beach all day! Enjoy your travels – so amazing to be able to see and experience so much of the world and other cultures!

Because of the bullish stock market and historically low interest rates many people have a significant net worth, but have difficultly producing adequate cash flow. CD rates are not worth chasing because they generate little income. Some people in this position are buying residential real estate in order to create an income stream, further inflating home values. In fast growing cities around Texas, large companies are buying out entire new home subdivisions before they are offered for sale to the public. The subdivisions are being bought with the intention of holding the valuable underlying land, while generating an income stream from the rental houses over the holding period. Residential rental rates are now soaring with potential renters sometimes making rental offers well above above the asking rental rate. For those that like to manage residential rental properties this could be an option for generating cashflow. I’ve tried being a landlord and found that it is not something I enjoy doing.

I’ve been down the landlording path as well but have sold off both of my properties over the years (my duplex being the last to go earlier this year). I’m glad to be out of it as well. Since then, I took the profits from that and moved them all into REITs. Not as many benefits as owning the properties yourself and possibly a little over-valued, but I’m content with the passivity and the income stream it brings in separate from my other equities.

Yep, in the same boat as you Jim. We’re in that part of the retiree life plan where we start chasing income and yield but hopefully not with more risk. Since bonds pay close to nothing, we’ve all been pushed into equities. Probably better to earn some side income than chase yield too much.

It’s interesting how a high net worth is becoming less important now rather than having cash flow that matches our expenses with extra for some desires like re-investing, travel, health and safety. If you were at 2x expenses in terms of cash flow from investments you’d probably feel super comfortable =) . Folks are ambitious to reach FI, so they also think with a little more active effort/part time hustles/hobbies they can move from a situation of artificial scarcity that a FIRE budget requires to one of abundance.

I read on ERN’s analysis now that although Trinity study is matched to inflation-adjusted expenses growth, we actually want to grow a little faster at inflation plus 1-2% since our peers are adjusting their lifestyle. Most folks don’t want to be 50%+ behind their peers in lifestyle, so it’s a little of lifestyle creep that we desire too.

See section 4 – https://earlyretirementnow.com/2021/08/18/when-to-worry-when-to-wing-it-swr-series-part-47/

Gotta love Big ERN – no one can deep dive like he can! Yeah, it certainly can be a little unnerving to be in our position since there’s simply no way to know for sure what the outcome will be over the long run. I really do think we’ll be ok, but no harm in adding a little extra income in the mix regardless. 🙂

Come to India to explore natural beauty at cheaper costs. I believe you will love it.

If I could be on a plane for that long, I would love to visit India. I’m sure it’s a wonderful place, Yogesh!

After years of focusing on accumulating wealth, the transition to withdrawing from that coveted net worth seems like a daunting one (at this point, I am 5-10 years away from FIRE anyway). Great to see the market has done its job and lifted your savings!

Thanks, IF – it is a little bit strange to suddenly stop the mode of saving and turn to spending. Actively understanding how the numbers work though as many of us in the community strive to understand makes it very logical though. It also makes it much easier when in a bull market like this one for sure! 🙂

I hear you on this:

“What I’m trying to say is that we have enough money to support our lifestyle but it has the potential to get cramped relatively quickly. And that’s something I don’t like.”

Once the lockdowns began, I decided to “go back to work” by making more money online. I had been rejecting almost all business partnerships that came my way for years. I just wasn’t that interested in making more money online.

But I figured, if I’m going to be locked down, I might as well make more! And more I’ve made for the past 18 months. Almost all of it was reinvested to generate at least $25,000 more a year in passive income.

I’m on break now, but will likely keep on grinding until the pandemic is over. Your guest post is out! Will share it around shortly.

Cheers,

Sam

Now that’s some nice extra side income! You’ve got to agree that enjoying what you do is the biggest key to this. You’re no longer working for someone else and I feel like the hustle to see how much more you can make sucks you back in somewhat. Is that fair to say?

Thanks so much for the guest post opportunity – very much appreciated! 🙂

Hi Jim

Very interesting and motivating read! I am currently in the accumulation phase, takes us some years to reach FI and it’s good to think also about the aspects around the withdrawal phase.

Thanks for sharing your insights and experience.

Cheers

To me, it became more of a mental thing than anything. The numbers all add up, but the comfort level of having some income would hopefully help me from staring at the numbers so much. 🙂

Hi. If you retire with 1.1m and calculate your withdrawal based on that amount, but 3 years later you have 1.6m, couldn’t you “restart” fire and calculate a new withdrawal amount with this new net worth? With a 4% rate, this would be 20k extra.

That is one way to do it Jorge and I do know people who do it that way, but there’s a catch to that as well. If it’s a bad year and let’s say your portfolio drops to $800,000, you can only spend $32k for the year. That’s a big downside that definitely wouldn’t work for me! 🙂